Chapter 2

Allegations regarding the performance and management of Energex

2.1

An impetus for this inquiry was the allegation that a Queensland

distribution network business, Energex, manipulated its weighted average cost

of capital (WACC). As explained in the first interim report, the Australian

Energy Regulator (AER) determines, on a periodic basis, the maximum amount of

revenue a distribution or transmission network business can recover from its

customers. The WACC is one of the inputs to the calculation of a network

business's maximum allowed revenue. The AER is required to set a WACC that

would provide the business with a rate of return commensurate with the

efficient financing costs of a benchmark efficient entity with a similar degree

of risk, in respect to regulated services.[1]

As part of the determination process, network businesses submit to the AER the

WACC they consider is required to meet this objective.

2.2

In addition, the committee also received evidence alleging that the same

state government-owned network business:

-

is not being managed in an efficient and prudent manner, with

unnecessary costs that result being passed on to consumers in the form of

higher electricity bills; and

-

had misled the AER, and others, about the necessity of certain

infrastructure.

2.3

This chapter outlines these allegations and Energex's response to them.

This chapter also considers the powers available to the AER for obtaining

the information necessary for it to perform its regulatory functions, as well

as the penalties for providing the AER with false or misleading information.

Finally, the chapter considers the proposal outlined in the terms of reference for

the creation of a new agency to consider these types of allegations in the future.

Allegations about data manipulation at Energex

2.4

Claims of data manipulation regarding Energex's cost of debt were made

by Ms Cally Wilson, a former Energex employee turned whistleblower. Ms Wilson

was a treasury analyst at Energex between June 2012 and September 2014.[2]

When she resigned from Energex, Ms Wilson took her concerns about various

practices to the Courier Mail, which published her allegations in a

series of articles. Ms Wilson subsequently wrote to the AER regarding her

concerns and appeared as a witness during this inquiry.

2.5

An incident at Energex that greatly concerned Ms Wilson was when she was

asked to find a cost of debt rate that would result in a higher WACC. The

following description of the task was provided:

What I was asked to do was to find a cost of debt rate that

would support management's target WACC of 8.23%. This is called reverse

engineering. I found a rate on Bloomberg that gave management the targeted

number they were after, however, it was an outlier from a US bank. At the time

I did think it was extremely odd that an outlier rate was used as normally

they are discarded.[3]

2.6

Ms Wilson explained that she did not, at the time, realise the

implications of identifying a rate that would substantiate a higher WACC, as

'normally a company tries to reduce their WACC'. However, Ms Wilson claimed the

reasons for diverging from regular corporate finance theory become clearer when

it is understood that regulated electricity network companies are not 'reimbursed

on their actual cost of funding, but rather what the AER determined their cost

of funding to be'. Ms Wilson noted that as interest rates had fallen

dramatically, compared to the start of the regulatory period in 2010, this had

resulted in 'a big profit (and probably unexpected profit) for Energex'.

According to Ms Wilson, Energex management was concerned that the fall in

interest rates to historic lows would mean the next WACC approved by the AER

would be substantially lower than the 9.72 per cent that was in place for the

2010–15 regulatory control period.[4]

To put it another way:

What they wanted to try to find was a WACC that was not going

to, as they called it, 'jump off a cliff'—so it was not too low and it was not

too high. I know they spent a lot of time actually figuring out what would

be a politically sensitive WACC to put in place.[5]

Energex's response

2.7

Energex strongly rejected the allegations levelled against it by Ms

Wilson. In particular, Energex highlighted the various obligations imposed

on it that seek to ensure the information provided to the AER as part of a

regulatory proposal is fair and reasonable. In its submission, Energex stated:

Energex's Regulatory Proposal is required to identify the key

assumptions that underlie the capital and operating expenditure forecasts which

are included in it, and the directors of Energex must certify the

reasonableness of these assumptions. In order to enable the directors to make

this certification, Energex has established comprehensive governance arrangements

that require Energex management to certify the accuracy and reasonableness of

the information on which those forecasts are based. Energex, through its Board

and management, takes its regulatory obligations very seriously and has at all

times complied with all applicable regulatory requirements, including the

requirement for director certifications.[6]

2.8

Both Energex and Ms Cally Wilson were in agreement that Ms Wilson was

not working on Energex's regulatory proposal. Energex's chief executive

officer, Mr Terence Effeney, stated that Ms Wilson was working on

Energex's corporate plan. Mr Effeney explained that Energex was examining

various scenarios for its corporate plan because 'the WACC has varied

enormously over the last period'. He stated:

Of course we are modelling, as a prudent organisation, a

whole range of scenarios about what the WACC outcomes might be, what the debt

parameters might be, what the equity outcomes would be. Of course we would

model all those things. A prudent business would do that. But that does not

mean that we are manipulating the regulatory outcome.[7]

2.9

In her evidence to the committee, Ms Wilson readily acknowledged that

she was not working on the regulatory proposal. However, Ms Wilson suggested

that the executive in charge of her team who was interested in the WACC

'probably would have been talking to the strategy and regulation team as well';

that is, the team that prepares the AER submissions.[8]

In any case, Ms Wilson observed that the corporate plan and statement of

corporate intent are for the Queensland government and reflect 'what Energex

believe at that point in time they can reasonably achieve'.

To put it another way, the corporate plan represents the key

performance indicators that Energex is signing up to.[9]

Ms Wilson stated that she believed the corporate plan figure 'ended up being

8.13, so it was fairly similar to the rate that we were currently looking at'.[10]

2.10

Energex explained that, each year, it provides its shareholding

ministers with a statement of corporate intent and corporate plan. Among other

things, the documents forecast future financial outcomes for the business. When

these documents were prepared in early 2013, it 'was necessary for Energex to

try and predict the WACC that would be determined by the AER for the next

regulatory period'.[11]

Energex noted that market conditions have changed substantially since 2009,

when the AER last determined Energex's WACC:

In 2009, the global financial crisis was still creating

uncertainty and significantly impacting debt and equity markets. In contrast,

at the moment, the current market condition reflect a stable, low interest rate

environment and lower debt and equity market expectations. This positive change

in sentiment was almost certain to lead to a lower WACC for the

2015–20 regulatory period.[12]

2.11

Energex maintained that the results of the modelling exercise did not

form part of the regulatory submission. That is, the work undertaken by Ms

Wilson did not affect the WACC determined by the AER, prices paid by consumers

or profits for Energex's shareholders.[13]

Energex also emphasised that the AER ultimately determines the WACC, not the

regulated entity. Mr Effeney concluded that the suggestion:

...that we can somehow or other manipulate the outcomes from

the AER: there is no substance to that; there is no fact. And it has been

clearly set out in the submissions by the people who set the rules and

administer the rules that that is not something that can be done.[14]

2.12

However, Ms Wilson noted that both Energex and Ergon Energy, the other

Queensland distributor, departed from the AER guidelines in their regulatory

submissions to justify their proposed WACC. Despite the statements by Energex

that the AER sets the revenue, Ms Wilson claimed the divergence from the

AER guidelines demonstrates that the network businesses seek to apply pressure

for a higher WACC.[15]

Claims of inefficiencies and other concerning practices at Energex

2.13

Ms Cally Wilson's evidence also criticised the culture and certain

practices at Energex that she claimed directly result in customers paying more

for electricity. Ms Wilson also raised these concerns in a submission to

the AER on Energex's most recent regulatory proposal.[16]

2.14

In Ms Wilson's evidence to the committee, three broad areas of concern

can be identified. The first concern is the level of staffing at Energex

and the expertise of Energex management. Ms Wilson described the staffing level

at Energex as 'excessive for its actual needs'. To provide some insight into

this, Ms Wilson recounted her observations of staff at Energex:

Walking around the building saw row upon row of employees

spending large amounts of their day engrossed in personal activities while the

inefficient dissemination of information means employees often spend large

parts of their days in unproductive meetings.

Employees are hired to do roles that became redundant in

commercial organisations a decade prior and any attempts to modernise,

streamline the workforce seem to be a very touchy subject due to labour

constraints. Treasury departments often look at work-place efficiencies but all

attempts by me to discuss cost-less technological changes that would affect a

personnel and cost reduction were quashed so Treasury wouldn't upset other

departments.[17]

2.15

Ms Wilson further noted that Energex employees can only be made

voluntarily redundant,[18]

meaning that Energex 'cannot get rid of people that probably need to be gotten

rid of, unfortunately'.[19]

Ms Wilson concluded that the 'sheer wastage of people's time' as a result of

over-staffing at Energex is 'mind-boggling'.[20]

Further, Energex's staff costs are, in Ms Wilson's view, 'astronomical'.

According to Ms Wilson, Energex staff received 'exceedingly generous

income and benefits compared to commercial standards for the same roles'. As an

example, Ms Wilson referred to a treasury officer at Energex employed on a

salary of $85,000 per annum despite not having a university degree or any

previous training.[21]

2.16

Ms Wilson also questioned the qualifications and competence of certain

executives. As an example, Ms Wilson remarked that during her time at Energex,

an individual who acted as the chief financial officer did not have

accounting qualifications.[22]

On the expertise of Energex executives more generally, Ms Wilson stated:

There are a lot of very nice people there, but I do not think

they are fully qualified to run a company of this size. There are no real risk

managers. There should be a lot more commercial expertise and people with real‑world

experience in this company, not just government experience. They have come up

through the ranks—they like the job and they have been sitting there for 15

years—but they have no training or educational qualifications in it.[23]

2.17

The second area that Ms Wilson suggested required attention was the

treatment of capital and operating expenditure. Ms Wilson told the committee

that 'Energex had a culture where it was always better to overspend on your

capital expenditure'.[24]

Ms Wilson outlined several rumours that she had heard while employed at Energex

'of things that probably were operating expenditure were rolled up into capital

expenditure'.[25]

2.18

The third area where Ms Wilson considered inadequate procedures at

Energex were contributing to higher electricity bills for consumers relates to

the business's financial practices, particularly with respect to risk

management. Ms Wilson noted that appropriate risk management techniques and

skilled treasury and procurement teams can often provide savings that amount to

many millions of dollars. Ms Wilson stated that, although Energex's hedging

methodology would work well with a skilled team, she considered it was an area

of concern due to the mismanagement she witnessed while employed there.

The following example was provided of how the risk associated with capital

expenditure could be treated:

At Energex, the concept that they should be able to quantify

the values of commodities and foreign exchange used was disregarded with the

viewpoint that it wasn't feasible as they didn't know what contracts would be

taken up. This is in direct contradiction with other multi-nationals and large

corporations that undertake a detailed and quantified understanding of their

capital expenditure exposures in order to better mitigate the risk of price

fluctuations.[26]

2.19

Another example involved an occasion where Ms Wilson 'spent many hours

trying to explain to senior people within the procurement and finance

departments at Energex that just because a country is within Europe, does not

mean it uses the euro'. She explained:

On one multi-million dollar contract, Energex took a position

against the euro which it had no currency exposure to while not hedging against

its currency exposure to the Norwegian krone.[27]

2.20

Ms Wilson also expressed concern that Energex employees faced potential

risks as a result of endorsements they supposedly had given for particular

transactions. Ms Wilson explained that, on at least one occasion,

financial analysis and commentary she had prepared for Energex's board that

argued a contract was not commercially beneficial to Energex was 'substituted

for wording that agreed with the financial viability of the procurement

contract'.[28]

Further, Ms Wilson stated that she found 'at least 50' documents with

her name on them that she had not approved. Ms Wilson reported that

management's response to her concerns about this was to 'agree that it was not

a very good thing to have happened and that they would try to ensure that it

did not happen again, but they could not guarantee it'.[29]

2.21

Ms Wilson also suggested there were significant weaknesses in the

auditing arrangements for the treasury section at Energex. Ms Wilson explained:

Normally when you are in a treasury department you get

audited very, very regularly because the moneys are flowing through you,

because you are the one inputting stuff into the bank account. When I was at

Energex, when I went through all the books, there had only been one

internal audit done—and they did not understand what questions to ask—and there

wasn't even any external auditing done. When I was in previous companies, at

one company I remember being audited quarterly but most of the time we were

audited half-yearly. While I was at Energex, we never had one of the big four

audit the treasury section; they audited other sections but never the treasury

section, which I thought was very unusual.[30]

2.22

Finally, Ms Wilson expressed concern about the Energex board's ability

to assess the proposals put to it. Although she agreed that the board has a

fiduciary duty, Ms Wilson observed it would be difficult to fulfil this

duty if the board is being 'lied to'. Ms Wilson stated that she

'definitely saw evidence of people covering up things, so they did not go to

the board'. Ms Wilson considered the board was unlikely to know of any problems

with data or other concerning practices within the business, as Energex

management is very good at what Ms Wilson termed 'marketing'. Ms Wilson

stated:

If you do not understand the intricacies, it would be very,

very easy to be taken in, because it sounds right. It is only when you look at

it that it is not right.[31]

2.23

Ms Wilson concluded that the problems at Energex were caused by 'a

culture that in effect has no accountability or transparency'. Ms Wilson called

on the AER to cut Energex's operating expenditure; Ms Wilson reasoned that by

doing so, Energex's management would be provided with an incentive 'to stop

sloppy, expensive habits that would not be tolerated in a commercial

environment'.[32]

Energex's response

2.24

Energex responded in detail to the issues about its operations that Ms

Wilson outlined. The following paragraphs outline Energex's response.

Energex's staffing

2.25

In response to the claim that Energex is over-staffed, Energex asserted

that, in the role Ms Wilson was employed in, it 'would be difficult for

any person to reasonably assess the Energex human resource requirements to

maintain a safe and reliable electricity network that meets our customers'

expectations'.[33]

More specifically, Energex advised that a strategy was initiated in 2012 that

has resulted in Energex's workforce being reduced by 'more than 20 per cent'.

This strategy was implemented in response to reduced electricity demand and

capital works. Energex added that its 'staffing levels and expenditure are

also regularly externally benchmarked and assessed'.[34]

2.26

Energex also refuted the claim that its management did not have the

necessary expertise to run the business. The following statement was provided:

Energex strongly rejects any allegation that its staff

members are not appropriately qualified or lack commerciality. Energex has

expert employees in a wide range of fields. Many have experience within

government and government owned corporations but many others have private

sector backgrounds.

Energex is very proud of the Energex staff and their

commitment to the community of South East Queensland. Energex will continue to

drive efficiency and seek to deliver quality and cost effective outcomes for

our customers.[35]

2.27

The evidence given about the qualifications of the acting chief

financial officer was specifically addressed. In its response to Ms Wilson's

evidence on this matter, Energex wrote that it 'rejects the allegation that

there was an acting chief financial officer with no accounting qualifications'.

Energex explained:

Following the departure of Energex's Chief Financial Officer

in 2013, Energex undertook a temporary restructure and the finance department

reported to an incumbent executive general manager with extensive experience in

the electricity industry.[36]

At no stage did the individual hold the title Chief Financial

Officer and at all times Energex had an appropriate level of skill, expertise

and qualifications in its finance department with appropriate controls and

oversight.[37]

2.28

Energex added that it 'is not unusual that temporary restructures such

as this take place during recruitment processes'. Following an open recruitment

process, a chief financial officer, with accounting qualifications, was

appointed in 2014 on an ongoing basis.[38]

Treatment of expenditure and

auditing arrangements

2.29

In addressing the whistleblower's concerns about the treatment of

capital and operating expenditure within Energex, the response from Energex

first questioned whether a treasury analyst in the financial accounting area of

the business could 'reasonably assess whether Energex has appropriately

allocated its expenditure between capital and operating expenses'.[39]

Nevertheless, Energex also addressed the claims by outlining its policies.

Energex provided the following statement about the classification of its

capital expenditure:

Energex capitalises expenditure in compliance with its

Finance Policy Manual which complies with Australian Accounting Standards and

cost attribution principles as outlined by the AER. Energex's statutory and

regulatory accounts are subject to external audit each year. No evidence of

incorrect costings to capital has been found as part of these audits.

Energex performs periodic reviews of the outcome of the

application of its internal business rules to verify ongoing compliance with

its Finance Policy Manual, Australian Accounting Standards and cost allocation

principles approved by the AER. Most recently in 2014, Energex also engaged a

large accounting firm to perform an independent review of material items being

capitalised to ensure ongoing compliance with Australian Accounting Standards.

An explanation of Energex's capitalisation process and rules

and a copy of the capitalisation policy are furnished to the AER on an annual

basis under Energex's regulatory reporting obligations.[40]

2.30

The evidence given about the auditing arrangements for Energex's

treasury section was specifically addressed. Energex contended that the

evidence received by the committee about this was inaccurate. Energex advised

that external audits of 'the key activities of Energex's treasury team to

the extent that they impacted the financial outcomes of Energex' were conducted

in 2012, 2013 and 2014. Energex also noted the internal audit Ms Wilson

referred to, which Energex described as 'comprehensive'.[41]

2.31

Another issue that Energex responded to was the evidence about its board

processes. Energex prefaced its comments on this matter by emphasising that the

Energex board 'takes its fiduciary and legal duties very seriously and complies

with its obligation to oversee and question management'. Further, Energex

stated that the board 'processes and sub‑committee structure are

extremely robust'.[42]

2.32

Energex questioned the level of involvement that Ms Wilson had with

board processes and decision-making. Energex stated that the treasury analyst

is 'responsible for providing advice to the procurement department on risk

mitigation of treasury risks arising from foreign currency and commodity

prices'. The treasury analyst does not have a role in approving a transaction.

Energex commented:

Accountability for the correctness and accuracy of the

relevant procurement board papers lay with the executive in charge of

procurement and the CEO, not Ms Wilson or the treasury department.[43]

2.33

Regarding the claim that Energex's procurement department changed

sections of board documentation Ms Wilson had written, Energex advised that after

'an extensive investigation, no supporting evidence could be found for Ms

Wilson's claims'.[44]

Further, Energex stated that the claims of mismanagement and fraud have been

'extensively investigated' by Energex, with both internal and external

investigators used. Energex reported that following these investigations, 'none

of the allegations were substantiated'.[45]

Concern about the need for infrastructure investment

2.34

Another set of allegations made in evidence taken during this inquiry is

that network businesses have misled the AER in relation to the necessity for

proposed infrastructure. The Agriculture Industries Electricity Taskforce

provided the following projects it considered were examples of unnecessary expenditure:

-

Transgrid's proposal for a transmission line in the Manning

Valley in 2011;

-

AusNet Services' proposed terminal station augmentations at

Brunswick, Melbourne in 2012; and

-

power lines proposed by Energex in the Logan River valley.[46]

2.35

The Logan River proposal involves the construction of a second 110

kilovolt sub-transmission power line from Loganlea to Jimboomba. The committee

received evidence from the Veto Energex Towers Organisation (VETO), a community

organisation formed in 2008 by Logan residents in response to Energex's

proposal. VETO advised that it, and Logan City Council, opposed the proposal

because:

...it will turn the already fragile Logan River valley into a

power line easement, clear Logan koala habitat, directly impact 90 rural

residential landowners and destroy the amenity of the historic township of

Logan village.[47]

2.36

VETO outlined at length the history of this project, including that its

cost has increased to $64.2 million from an initial amount of $26 million.[48]

VETO argued that alternative proposals the community considered were more

acceptable were not adequately contemplated by Energex. According to VETO,

documents released under freedom of information reveal that Energex employees

were 'deliberately jacking up land acquisition costs' to weaken an alternative

proposal developed by the Logan City Council.[49]

VETO concluded that Energex does not 'genuinely respect the needs of the

communities in which they expect to operate'.[50]

2.37

Finally, VETO noted that the AER had expressed concerns about Energex's

compliance with the National Electricity Rules. Following complaints lodged by

the Logan City Council and VETO, the AER conducted a review of the regulatory

test used by Energex. The AER's review identified 'several compliance

issues', including that the Energex regulatory test consultation report 'did

not adequately contain details of the two alternative options proposed by

Energex'.[51]

The AER reported that it would monitor future regulatory test processes

undertaken by Energex. However, VETO considered the AER's actions were

'inadequate'. In particular, VETO was disappointed that Energex was not

required to substantiate its proposal 'or assess any alternatives that could

have delivered lower cost outcomes for consumers and our community'.[52]

Energex's response

2.38

Energex responded to the allegations made by VETO. In a letter to the

committee, Mr Effeney stated that Energex appreciates the proposed power line

project 'has been a long running and controversial development which has

brought about diverse views within the community'.[53]

Mr Effeney also acknowledged there had 'been shortcomings in the public

consultation process surrounding the initiation of this project in 2008'. In

relation to the areas for improvement found by the AER, Mr Effeney wrote:

Energex has taken these recommendations seriously and fully

implemented each of them. We continue to strive for improvements in the way we

talk to, and work with, the community we service.[54]

2.39

However, Mr Effeney advised that Energex rejects 'the assertion that it

has in any way manipulated cost estimates'. The following statement was

provided:

The cost forecasts, including land cost, and other

assumptions which underpin this project have been subject to extensive public

consultations. Commencing with a Corridor Selection Report, followed by an

Initial Assessment Report, a Supplementary Initial Assessment Report and a

Final Initial Assessment Report issued in 2010.[55]

2.40

The response noted that these reports are publicly available on a

website, as is a consultant's report that was commissioned by the Queensland

government. Energex claimed that its internal processes in this matter 'have

been extensively scrutinised and reviewed'.[56]

Responses to the allegations from the AER and other interested parties

2.41

Ultimately, when a regulator is presented with information, it needs to

carefully assess that information and identify and act on any data

manipulation, claims of inefficient expenditure or evidence indicating a

contravention of the laws it administers.

2.42

The potential for regulated entities to attempt to mislead the regulator

is not a problem that is unique to the AER; the Economic Regulation Authority

(ERA), which performs tasks in Western Australia similar to the AER,

recognised the risk of data anomalies and manipulation. The ERA informed the

committee that, when exercising its regulatory functions:

...the ERA always undertakes its own research and analysis to

arrive at its determination of the efficient WACC. In undertaking this

research, the ERA is able to identify any anomalies in data presented by the

service provider and thereby to form its own view as to its credibility.

The ERA is aware of the potential for data manipulation. To

minimise the risk of this occurring, the ERA pays particular attention to

verifying original data sources and to replicating analysis. The ERA also forms

its own independent views on issues, rather than relying on the assertions of

service providers and their consultants.[57]

2.43

It is also instructive to consider another statement made by the ERA on

this matter. The ERA noted that profit-maximising entities should be expected

to 'seek to legitimately present the best possible case for them' and warned

that this 'should be distinguished from deliberately misleading the regulator'.[58]

2.44

The Energy Networks Association (ENA) told the committee it is 'not

aware of any evidence that any network has provided misleading information to

the AER in relation to any cost of capital or regulatory valuation issue'. The

ENA added that it would expect to be aware of any issue that had arisen given

its regular engagement with the AER.[59]

2.45

The AER advised that it has raised Ms Wilson's claims with Energex.

The information received by the AER as a result of its discussions with

Energex

'will be taken into account, and reflected in', the AER's preliminary revenue

determination (which is discussed at paragraphs 2.54–2.55).[60]

The AER added:

More generally, our analysis in examining the proposals is

aimed at ensuring that data is robust and resulting costs are efficient such

that consumers are paying no more than necessary for safe and reliable

electricity services.[61]

2.46

The AER also responded to questions from the committee about Energex's

operating expenditure. The AER noted that there is 'considerable difference' in

operating expenditure across distribution businesses in the National

Electricity Market (NEM).[62]

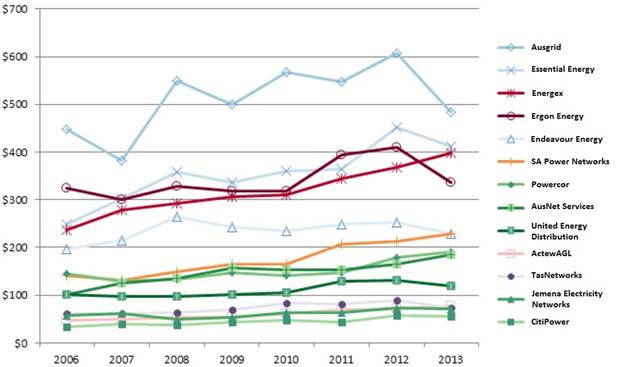

In 2013, Energex had the third highest operating expenditure (Figure 2.1),

which compares favourably to Energex's customer numbers.[63]

On the other hand, as Figure 2.1 shows, Energex's operating costs have

increased significantly, rising from approximately $300 million in 2009 to

around $400 million in 2013.

Figure 2.1:

Operating expenditure by distributor ($ millions, 2013)

Source:

AER, Answer to questions on notice 8, received 10 April 2015, p. 6

(chart edited to replace abbreviated names of network businesses with

unabbreviated names).

The AER's information gathering powers and penalties for providing false or

misleading information

2.47

In light of the various allegations regarding the information provided

to the AER, it is necessary to consider the regulator's powers to gain

information and the penalties for providing false or misleading information to

the regulator. This section examines the current powers and sanctions. The

evidence received about the need for a new Commonwealth agency to investigate

misconduct is also discussed.

Overview of information gathering

powers and penalties

2.48

In its submission, Energex highlighted the information gathering powers

that the AER has to conduct its regulatory functions. Under these statutory

powers,[64]

the AER 'requires network businesses to collect and maintain information

in a manner approved by the AER and to submit it annually or as part of the

regulatory reset process'. Energex explained that the accuracy and the quality

of the information supplied to the AER is typically certified by its board

and/or the chief executive officer. Energex noted that section 28R of the

National Electricity Law (NEL) prohibits the provision of false or misleading

information to the AER in purported compliance with a requirement to provide

information to the AER.[65]

It is a criminal offence to contravene this provision, punishable by a maximum

penalty of $2000 for an individual and $10,000 for a body corporate.[66]

2.49

Energex suggested that another protection against false or misleading

information being supplied to the AER is the public nature of the determination

process. Although network businesses such as Energex can seek confidentiality

over parts of documents, in Energex's view, the AER strictly applies the

confidentiality rules 'with the intention of providing the community and market

participants with the maximum possible information'. Energex acknowledged that

the 'greater scrutiny that can be applied where information is publicly

available also increases the weight that the AER is able to ascribe to such

information'.[67]

2.50

The Department of Industry added that the Commonwealth Criminal Code

contains offences for providing false or misleading information or documents

that have general application to all Commonwealth entities. Specifically:

Section 137.1 of the Criminal Code makes it an offence to

give information to Commonwealth entities knowing it to be false or misleading

or omitting any matter or thing without which the information is misleading.

The penalty for contravention of this section by a person is imprisonment

for 12 months. By virtue of the operation of section 4B(3) of the Crimes

Act 1914 (Cth), a court may impose on a body corporate a penalty not

exceeding $51,000.[68]

2.51

Finally, the AER may revoke a determination that is in place if it

considers the determination is affected by certain types of material errors or deficiencies.

One category of deficiencies that the AER may rely on for revoking a

determination is if the AER was provided with false or materially misleading

information.[69]

The need for a new Commonwealth

agency to investigate misconduct

2.52

The terms of reference for this inquiry asked the committee to consider

whether an independent Commonwealth authority should be established to

investigate anomalies identified in relation to price structuring or

allegations of price rorting by electricity companies.

2.53

There was little support for this proposal. The Electrical Trades Union

stated it would support 'the principle' that allegations of price rorting

should be investigated by an independent Commonwealth body with the required

powers and reach to investigate and prosecute.[70]

However, other stakeholders that commented on this aspect of the inquiry's

terms of reference—including electricity businesses (both network and

retail), the Department of Industry and agricultural industry bodies—did not

support the creation of a new agency.[71]

The AER's preliminary decision on Energex's revenue for 2015–2020

2.54

On 30 April 2015, the AER released its preliminary decision on Energex's

revenue for the 2015–16 to 2019–20 regulatory control period. The AER accepted

Energex's forecasted operating expenditure for this period, which results in an

average operating expenditure of around $347 million a year.[72]

However, the AER decided on a significantly lower rate of return than that

proposed by Energex. In its October 2014 regulatory proposal, Energex

submitted that a rate of return of 7.75 per cent was required. The

AER agreed to a rate of return of only 5.85 per cent for 2015–16, to be updated

annually until the end of the regulatory control period in 2020.[73]

2.55

Overall, the AER's preliminary decision is that Energex can recover

around $6.5 billion from consumers over the 2015–20 regulatory control

period.[74]

This is significantly lower than the over $8.3 billion sought by Energex in its

regulatory proposal.[75]

Committee view

2.56

The committee has noted with concern the various allegations levelled

against Energex, a distribution network service provider that operates in

Queensland. The wide-ranging allegations went to the modelling of

Energex's cost of debt, various internal financial practices, Energex's

staffing levels, and unnecessary network investment undertaken by the business to

the detriment of electricity customers generally and local affected residents.

2.57

The majority of these allegations were put to the committee by a former

Energex employee. The committee appreciates that a whistleblower was

prepared to come forward and recount their experiences. There are many examples

in the public and private sectors where serious wrongdoing, malpractice or

other troubling practices only come to light because of whistleblowers.

2.58

The first allegation the committee will address is the evidence

regarding the modelling of the cost of debt. The committee's first interim

report discussed the perverse incentives currently enshrined in the process by

which the maximum allowable revenue for a network business is determined,

including how network businesses appear to 'game' the regulator.[76]

2.59

The committee notes that, since the current framework was introduced, the

AER has never agreed to a WACC that network businesses have initially proposed.[77]

Despite this, stakeholders are concerned that the network businesses benefit

from the current method for considering revenue proposals, as businesses can

'frame the discussion' by submitting detailed regulatory proposals containing

proposed revenues that are higher than what the regulator can accept.[78]

The AER must effectively disprove the business's original proposal by

determining an alternative WACC based on a hypothetical benchmark of an

efficient business. The regulator must do this while being inundated with

information and documents during the revenue determination process.[79]

2.60

The evidence regarding the modelling of the cost of debt at Energex provides

a case study of some of these issues. The committee notes Energex's position

that the modelling exercise was not directly used in the regulatory proposal

lodged with the AER in October 2014. In any case, it is clear that the AER has

not accepted Energex's proposal. Energex's October 2014 regulatory proposal to

the AER used a figure of 7.75 per cent for its rate of return. The AER's April

2015 decision provides Energex with a significantly lower rate of return of 5.85

per cent for 2015–16, to be updated annually.[80]

2.61

However, the Energex case study provides further evidence of the

apparent mindset of network business executives that the WACC must be as high

as possible, regardless of the circumstances. The use of an outlier to

establish a WACC for a corporate document, or for any other purpose, does not

appear to be a reasonable action. More significantly, the AER's preliminary

determination for Energex's rate of return was 190 basis points lower than

Energex's proposal. In light of this, it is difficult to see how Energex's

initial estimate was reasonable.

2.62

The evidence regarding various internal matters in Energex also concerned

the committee. The committee notes the evidence that Energex provided about the

reduction in its staffing levels since 2012. However, the committee is

concerned that one of the reasons put forward by Energex to dismiss the

whistleblower's concerns about over-staffing is that the whistleblower was

employed as a treasury analyst and had no involvement in the human resources

aspects of the business. While that is the case, employees, particularly

employees who have previously worked in other organisations, do not need

management or human resources responsibilities to observe, and be concerned

about, inefficiencies. Energex's evidence does not indicate it supports a

culture where employees are encouraged to identify and speak up about

inefficiencies and waste.

2.63

Similarly, the committee notes that Energex highlighted the

whistleblower's job description to suggest that an individual working in that

role would have a limited insight into other parts of the business, such as

regulatory issues. The committee was cognizant of the scope of the treasury

analyst's responsibilities when considering the evidence put forward. However,

the committee does not accept that an employee working in one area of the

business will not gain a detailed awareness of practices in other areas. Within

any organisation, information is shared with other employees and quickly spreads.

Of course, it is necessary to separate unfounded gossip from those claims that have

merit, but concerns should not be dismissed out of hand.

2.64

The committee has considered each claim on its merits, taking into

account Energex's response. However, the role of this committee is not to make

findings against particular individuals or organisations; rather, the committee

gathers and tests information for the purpose of formulating recommendations

for changes in policy, legislation or administration. Based on the evidence

before it, the committee considers there are lingering questions about various

practices within Energex. Accordingly, there is a case for a thorough external

audit of the performance of Energex's financial risk management practices, with

a focus on Energex's treasury section. A well‑resourced external

performance audit, as distinct from a financial audit, would enable the

operations of the business to be closely inspected and a wider range of Energex

employees interviewed. As Energex is a Queensland government-owned business, this

is a matter for the Queensland government to consider.

2.65

Finally, the terms of reference for this inquiry asked the committee to

consider whether a new Commonwealth body should be established to investigate

allegations of misconduct by electricity businesses. The committee does not

consider there is sufficient evidence to support this proposal. Clearly, the

regulator that determines the maximum revenue of network businesses—the AER—must

be provided with accurate and relevant information to ensure that optimal

decisions are made. However, it was not demonstrated that there were problems

with the existing arrangements that prohibit the provision of false and

misleading information to the AER. In the committee's opinion, the crux of the

matter is that the regulator needs to ensure it employs adequate scepticism

when assessing the information provided to it. Further, as discussed in the first

interim report, the regulator must also be resourced appropriately. The

committee emphasises the recommendations it made in the first interim report

regarding these matters.

Recommendation 1

2.66

The committee recommends that the Queensland Government request the

Queensland Auditor-General to conduct a performance audit of financial risk

management practices at Energex.

Senator Anne Urquhart

Chair

Navigation: Previous Page | Contents | Next Page