Chapter 3

Overview of the regulatory framework and revenue determination process

3.1

The electricity system comprises four components: generation,

transmission, distribution and retail activities. Retailers purchase

electricity from the generators, the transmission networks connect generators

to the distribution networks, which in turn connect most end users. Retailers sell

bundled electricity and network services to residential, commercial and

industrial energy consumers.[1]

3.2

This inquiry focuses on two components of electricity supply: the

transmission and distribution networks. This chapter provides an overview of

electricity networks and why they are regulated. This chapter also outlines the

key regulatory and policy bodies that have a role in electricity regulation in

the National Electricity Market (NEM). The committee has generally limited the

scope of this report to the network businesses that operate in the NEM as

concern about network costs has largely been evident in NEM states and the

majority of the evidence received related to the NEM's regulatory framework.

The specific business referred to in the terms of reference for this inquiry

also operates in the NEM.

Networks in the National Electricity Market

3.3

Prior to May 1996, state and territory government-owned utilities

provided all four components of electricity supply. Every state and territory,

except Western Australia (WA) and the Northern Territory (NT), are now

connected to neighbouring states by interconnectors and participate in the NEM.[2]

The NEM is the wholesale electricity market that allows for electricity

generated in one state to be transmitted and sold in another state. The NEM

spot market is run by the Australian Energy Market Operator (AEMO).

3.4

Electricity networks facilitate the transmission of electricity from

generators to customers, often over long distances. To minimise transmission

losses, transformers convert power to a high voltage when it enters the

transmission network. After the high voltage electricity is transported by the

transmission lines, substations convert the electricity to a lower voltage for

transport along a distribution network. Substations within the distribution

network lower the voltage further, making the electricity suitable for use by

consumers (although some power is provided to end users at a high voltage).[3]

3.5

Within the NEM, there are five transmission networks and 13 major

electricity distribution networks. The total asset value of the transmission

and distribution networks in the NEM is over $70 billion.[4]

The Productivity Commission (PC) has noted that the NEM is 'one of the most

geographically dispersed electricity networks in the world', with more than 40,000

kilometres of transmission lines and 777,000 kilometres of distribution

networks. In comparison, the United Kingdom's population, which is more than

three times that of the NEM's, is served by approximately 25,000 kilometres

of transmission lines and 800,000 kilometres of distribution lines.[5]

3.6

Key background information about the networks in the NEM is provided at Table

3.1 and Table 3.2.

Table

3.1: Electricity transmission networks in the NEM

|

Network

|

Location

|

Line length (circuit km)

|

Electricity transmitted (GWh),

2012–13

|

Maximum demand (MW), 2012–13

|

Asset base* ($ million)

|

Owner

|

|

Powerlink

|

Queensland

|

14 310

|

49 334

|

10 956

|

6 035

|

Queensland Government

|

|

TransGrid

|

NSW

|

12 893

|

65 200

|

17 100

|

5 289

|

NSW Government

|

|

AusNet Services

|

Victoria

|

6 573

|

49 056

|

9 342

|

2 414

|

Listed company (Singapore Power International 31%, State Grid

Corporation 20%)

|

|

ElectraNet

|

South Australia

|

5 527

|

14 284

|

4 136

|

1 786

|

State Grid Corporation 46.5%, YTL Power Investments 33.5%, Hastings

Utilities Trust 20%

|

|

TasNetworks

|

Tasmania

|

3 503

|

12 866

|

2 483

|

1 236

|

Tasmanian Government

|

|

NEM totals

|

|

42 806

|

190 740

|

|

16 760

|

|

Source: AER, State

of the energy market 2014, p. 66.

Table 3.2: Electricity distribution networks in the

NEM

|

Network

|

Customer numbers

|

Line length (circuit km)

|

Electricity delivered (GWh),

2012–13

|

Maximum demand (MW), 2012–13

|

Asset base* ($ million)

|

Owner

|

|

Queensland

|

|

Energex

|

1 359 712

|

51 781

|

21 055

|

5 029

|

10 197

|

Queensland Government

|

|

Ergon Energy

|

710 431

|

160 110

|

13 496

|

3 420

|

8 837

|

Queensland Government

|

|

New South Wales and Australian Capital Territory

|

|

AusGrid

|

1 635 053

|

40 964

|

26 338

|

5 570

|

13 613

|

NSW Government

|

|

Endeavour Energy

|

919 385

|

35 029

|

16 001

|

4 156

|

5 344

|

NSW Government

|

|

Essential Energy

|

844 244

|

191 107

|

12 291

|

2 294

|

6 518

|

NSW Government

|

|

ActewAGL

|

177 255

|

5 088

|

2 903

|

698

|

790

|

ACTEW Corporation (ACT Government): 50%; Jemena (State Grid

Corporation 60%, Singapore Power International 40%): 50%

|

|

Victoria

|

|

Powercor

|

753 913

|

73 889

|

10 556

|

2 396

|

2 869

|

Cheung Kong Infrastructure / Power Assets 51%; Spark Infrastructure

49%

|

|

AusNet Services

|

681 299

|

43 822

|

7 501

|

1 877

|

2 809

|

Listed company (Singapore Power International 31%, State Grid Corporation

20%)

|

|

United Energy

|

656 516

|

12 837

|

7 856

|

2 077

|

1 789

|

DUET Group 66%; Jemena (State Grid Corporation 60%, Singapore Power

International 40%) 34%

|

|

CitiPower

|

322 736

|

4 318

|

5 981

|

1 493

|

1 601

|

Cheung Kong Infrastructure / Power Assets 51%; Spark Infrastructure

49%

|

|

Jemena

|

318 830

|

6 135

|

4 254

|

986

|

1 031

|

Jemena (State Grid Corporation 60%, Singapore Power International

40%)

|

|

South Australia

|

|

SA Power Networks

|

847 766

|

87 883

|

11 008

|

2 915

|

3 469

|

Cheung Kong Infrastructure / Power Assets 51%; Spark Infrastructure

49%

|

|

Tasmania

|

|

TasNetworks

|

279 868

|

22 336

|

4 248

|

239

|

1 455

|

Tasmanian Government

|

|

NEM totals

|

9 507 007

|

735 298

|

143 488

|

|

60 322

|

|

*Asset bases are at

June 2013 (December 2013 for Victorian businesses).

Source: AER, State of the energy market 2014,

p. 67.

Regulation of electricity networks in the National Electricity Market

Rationale

3.7

Electricity network businesses in Australia are subject to economic

regulation, as is the case in many other countries. Generally, this regulation

is based on an understanding that electricity transmission and distribution

networks are capital intensive operations where increased output results in

declining average costs. As a result of the evident economies of scale, it is

generally accepted that networks are a natural monopoly. That is, the most

efficient outcome is for a single supplier to provide network services in a

particular geographic area.[6]

3.8

Economic regulation of a natural monopoly is required to prevent

monopoly pricing, where inefficient outcomes result from monopoly firms

charging customers more than what it costs to supply them.[7]

Efficient levels of investment and costs are encouraged by providing the

monopoly firm with incentives similar to those faced by firms in competitive

markets. Economic regulation is also supplemented by other regulatory

requirements seen as desirable, such as reliability and quality of supply

standards.[8]

Legislative framework

3.9

The creation of the NEM followed the National Electricity Market

Legislation Agreement (NEMLA) entered into by New South Wales, Victoria,

Queensland, South Australia and the Australian Capital Territory in 1996. The

agreement provided for the National Electricity Law (NEL), a single national

law for electricity regulation.[9]

The NEMLA was replaced by the Australian Energy Market Agreement (AEMA)

entered into by the Council of Australian Governments (COAG) in June 2004.

Tasmania entered the NEM in May 2005.[10]

3.10

The NEL provides the foundation for the regulatory framework governing

electricity networks in the NEM. Underpinning this framework is the National

Electricity Objective (NEO), which is contained in section 7 of the NEL.

The NEO is as follows:

The objective of this Law is to promote efficient investment

in, and efficient operation and use of, electricity services for the long term

interests of consumers of electricity with respect to:

- price, quality, safety, reliability and security of

supply of electricity; and

- the reliability, safety and security of the national

electricity system.[11]

3.11

The National Electricity Rules (NER) are made under the NEL. The NER provide

the detailed arrangements that govern the operation of the NEM. Matters covered

by the NER include:

-

the procedures that govern the operation of the market for the

wholesale trading of electricity;

-

the economic regulation of distribution and transmission services;

-

retail markets; and

-

metering.[12]

3.12

The NEL and NER provide the basis for the revenue determination process,

which is discussed later in this chapter and in subsequent chapters.

Institutional regulatory

arrangements in the NEM

3.13

There are several bodies established under the NEL and Commonwealth

legislation that have a role in electricity policy or the regulation of the

networks. These bodies either determine the overall policy that is applied to

the NEM or administer functions under the NEL and NER. Of most relevance are

the:

-

COAG Energy Council;

-

Australian Energy Market Commission (AEMC);

-

Australian Energy Market Operator (AEMO); and

-

Australian Energy Regulator (AER).

3.14

The functions and responsibilities of these bodies are outlined below.

COAG Energy Council

3.15

Reflecting the multi-jurisdictional nature of the NEM, the COAG Energy

Council (formerly the Standing Council on Energy and Resources, or SCER) has

responsibility for priority issues of national significance and key reforms in

the energy and resources sectors. The COAG Energy Council is comprised of

energy and resources ministers from the states, territories and New Zealand.

Australian Energy Market Commission

3.16

The AEMC makes rules under the NER, as well as the national gas and

energy retail rules. The AEMC also conducts reviews of aspects of the energy

markets at the request of the COAG Energy Council. The AEMC is responsible to

the COAG Energy Council and is funded by state and territory governments.[13]

3.17

In making rule changes, the AEMC must follow an open and consultative

process to ensure that decisions take account of the views of stakeholders.

Proposed rule changes are assessed against the relevant statutory objective;

for the regulation of electricity networks, this is the NEO.

Australian Energy Market Operator

3.18

AEMO was established in 2009, superseding the National Electricity

Market Management Company (NEMMCO) and the state energy market management and

planning entities. AEMO's electricity responsibilities include managing the wholesale

electricity market and playing a coordinating role in ensuring system security

when demand exceeds supply. Other functions performed by AEMO include the

provision of long‑term planning reports and regional demand forecasts and

the planning for the Victorian electricity transmission system (in other

jurisdictions, the state government or the transmission service provider

undertakes these functions).[14]

3.19

AEMO's ownership structure is divided between government (60 per cent)

and industry (40 per cent). Industry members include generators, transmission

companies, distribution businesses, retailers, and resource companies across

the eastern and south-eastern states of Australia. AEMO operates on a cost

recovery basis as a company limited by guarantee under the Corporations Act

2001.[15]

Australian Energy Regulator

3.20

Economic regulation in the NEM is provided by the AER, an independent

statutory authority located within the Australian Competition and Consumer

Commission (ACCC).[16]

The AER regulates network providers in accordance with the NEL and the NER. Its

main role is the determination of network revenue, although it also has

compliance and information reporting functions.[17]

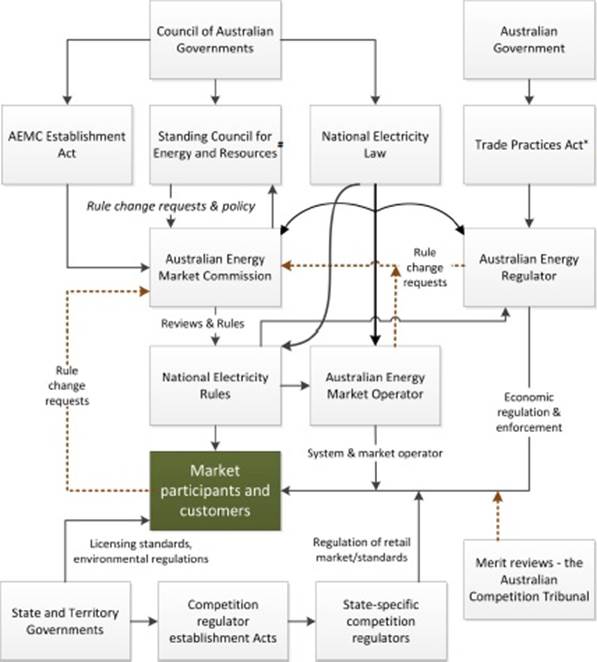

Figure 3.1: Institutional arrangements in

the NEM

# Now the COAG Energy Council.

* Now the Competition and Consumer Act 2010.

Source: PC, Electricity

networks regulatory frameworks, vo1. 1, April 2013, p. 85; modified to

indicate recent changes.

Introduction to the revenue determination process

3.21

The economic regulation applied to network businesses involves a

regulator determining the amount of revenue the business can recover from its

customers. For businesses operating within the NEM, this regulator is the

AER.

Key statutory requirements and

principles

3.22

The determination process and the roles of the AER are set out in the

NEL and NER. The AER is required to exercise its economic regulatory powers and

functions in a manner that will, or is likely to, contribute to the achievement

of the NEO (section 7 of the NEL).[18]

As is evident from the wording of the NEO (see paragraph 3.10), and as the

AER noted in its submission, the objective is 'not only concerned with cost

outcomes for electricity consumers', but also the safety, reliability and

security of energy supplies.[19]

3.23

Section 7A of the NEL contains revenue and pricing principles that must

be applied to determinations. The principles provide:

-

that a network business should be provided with a reasonable

opportunity to recover efficient costs;

-

for incentives to promote efficiencies; and

-

that prices should reflect returns commensurate with the risks

involved in providing network services.

3.24

In addition to the objectives and principles set out in the NEL, the NER

provide the framework the AER must apply in undertaking its revenue

determination role. The rules for the economic regulation of distribution and

transmission networks are contained in chapters 6 and 6A of the NER

respectively.

Benchmarking

3.25

Incentive-based regulation is enshrined in the NEL and NER, with the

benchmarking requirements providing a clear example. When determining the

amount of revenue that a network business can recover from its customers, the

AER must set an allowed rate of return that reflects the efficient financing

costs of a benchmark efficient entity. This involves the AER considering the

revenue that would be required by a benchmark efficient business to cover its

efficient costs and to provide a commercial return on capital. The AEMC

explained that the benchmark entity used by the AER 'must be subject to a

similar degree of risk in providing regulated services as the network

business'. The AEMC noted that the framework maintains 'incentives for

investment because investors can reasonably expect to recover efficient costs'.

The AEMC argued that this approach provides incentives for 'network

businesses to raise capital as cheaply as possible and make efficient

expenditure decisions':

Put simply, if the business spends less than the estimated

efficient cost it will earn a higher return because it will still be allowed to

recover the total revenue for the remainder of the regulatory period.

Conversely, if its spending exceeds the estimated efficient costs, it will earn

a lower return or potentially make a loss because it will not be allowed to

recover the additional spending. The essential point is that the revenue of a

particular network business is based on estimates of the efficient costs of a

prudent operator and not on their actual costs.[20]

3.26

The AEMC explained that the alternative to an incentive-based approach

is a cost of service regulatory framework, where the revenue allowance 'is

based on the costs that the individual business requires to provide services'.

The AEMC argued that such frameworks do not 'provide strong incentives for

regulated firms to operate efficiently and minimise costs'.[21]

Method for recovering revenue

3.27

A key consideration in revenue regulation is how the revenue will be

recovered. Conceptually, the allowed revenue that a network business can

recover from its customers can be recovered in two ways, either by a revenue

cap or a price cap. Under a revenue cap approach, the AER determines the

allowed revenue a network business can recover from its customers over the

regulatory period. A price cap sets an average price level that a network

business can charge over the regulatory period.

3.28

The AEMC provided the following information about these approaches:

Prices are based on estimates of future demand under both

approaches. Under the revenue cap approach, average prices are adjusted each

year for errors in forecast demand that result in revenue recovery above or below

the allowed revenue. Put simply, network businesses under a revenue cap are

guaranteed to recover the allowed revenue over the regulatory period. Under a

price cap approach, prices are not adjusted for errors in forecast demand which

result in revenue recovery above or below the allowed revenue. Variations in

the allocation of risk should be reflected in how the AER determines the

allowed rate of return.[22]

3.29

The AEMC went on to note that the AER determines whether a revenue cap

or price cap is 'most appropriate for the network business in order to maximise

benefits for end-users'. The AEMC observed that recent network revenue

determinations made by the AER have used a revenue cap approach. The AEMC

suggested that by shifting the burden of demand risk onto consumers, the

revenue cap approach could possibly result in lower prices:

Network businesses are

required to meet their jurisdictional requirements for reliability such that

they are obliged to maintain and develop the network to meet expected demand.

In return, consumers experience the benefits of this reliability standard.

There may be considerable risk to network businesses who are required to meet

both a state-mandated reliability standard (that requires investment) and

declining demand (a smaller amount of demand over which to recover the

costs of that investment). By consumers bearing the demand risk through a

revenue cap approach the risks of the network business are lower and there

could then be an opportunity for the benefits to be passed on to consumers in

the form of a lower allowed rate of return to the network.[23]

Steps in regulating network revenue

3.30

The process for determining the amount of revenue that network

businesses can recover from customers is ex-ante—businesses apply to the AER

for an assessment of their revenue requirements in advance of a new regulatory

period. Chapters 6 and 6A of the NER set out a detailed process that the AER

must follow in regulating distribution and transmission network revenues. This

process is as follows:

-

The AER is required to publish a 'framework and approach' paper

23 months before the end of the network business's current regulatory control

period (RCP). The paper must set out the AER's proposed approach to the

business's next regulatory determination.

-

The network business must submit a detailed regulatory proposal

to the AER at least 17 months prior to the end of its current RCP. The

regulatory proposal must set out the business's proposed regulated revenues for

the following RCP.

-

The AER must publish:

-

the network business's regulatory proposal and related documents;

-

an issues paper the AER has prepared seeking written submissions

from stakeholders; and

-

an invitation to stakeholders to attend a public forum on the

issues paper, well before stakeholder submissions are due to be submitted.

-

The AER must then publish, nine months before the RCP ends:

-

a draft determination setting out where it refuses to approve any

aspect of the network business's regulatory proposal;

-

notice of a pre-determination conference; and

-

an invitation for stakeholders to make written submissions.

-

The AER must ultimately publish, at least two months before the

RCP ends, a final determination setting out:

-

where it has not accepted elements of a network business's

regulatory proposal;

-

reasons why it has not accepted those elements of the proposal;

and

-

its decision in substitution of those elements of the regulatory

proposal it has not accepted.[24]

3.31

Following a final determination by the AER, affected parties can apply

to the Australian Competition Tribunal for a review of the merits of the

determination. Determinations are also subject to judicial review.

3.32

Table 3.3 outlines the next RCPs and key dates for AER decisions.

Table 3.3: Timetable for upcoming revenue

determinations

|

State/ Territory

|

Service provider

|

Regulatory control period

|

Draft decision

|

Final decision

|

|

Electricity

transmission

|

|

NSW/Tas

|

TransGrid, TasNetworks

|

1 Jul 2015 – 30 Jun 2019

|

27

Nov 2014

|

30

Apr 2015*

|

|

Qld/NSW

|

Directlink

|

1 Jul 2015 – 30 Jun 2025

|

27

Nov 2014

|

30

Apr 2015

|

|

Vic

|

AusNet Services

|

1 Apr 2017 – 30 Mar 2022

|

30

Jun 2016

|

31

Jan 2017

|

|

Qld

|

Powerlink

|

1 Jul 2017 – 30 Jun 2022

|

30

Sep 2016

|

30

Apr 2017

|

|

SA

|

ElectraNet

|

1 Jul 2018 – 30 Jun 2023

|

30

Sep 2017

|

30

Apr 2018

|

|

Vic/SA

|

Murraylink

|

1 Jul 2018 – 30 Jun 2023

|

30

Sep 2017

|

30

Apr 2018

|

|

Electricity

distribution

|

|

NSW/ACT

|

Ausgrid, Endeavour Energy, Essential Energy, ActewAGL

|

1 Jul 2015 – 30 Jun 2019

|

27

Nov 2014

|

30

Apr 2015*

|

|

Qld/SA

|

Energex, Ergon Energy, SA Power Networks

|

1 Jul 2015 – 30 Jun 2020

|

30

Apr 2015

|

31

Oct 2015

|

|

Vic

|

CitiPower, Powercor, Jemena, Jemena, AusNet

Services, United Energy

|

1 Jan 2016 – 30 Dec 2020

|

31

Oct 2015

|

30

Apr 2016

|

|

Tas

|

TasNetworks

|

1 Jul 2017 – 30 Jun 2022

|

30

Sep 2016

|

30

Apr 2017

|

* These

determinations involved a transitional year determination 2014–2015 and a final

determination for 2015–2019.

Source: AEMC, Submission 41,

pp. 17–18.

The 'building block' approach

3.33

The NER outline a 'building block' approach to setting the revenue that

networks are allowed to recover from their customers. The building blocks are

estimates of the various costs a network business needs to incur while

efficiently providing network services to customers over the RCP. These

building blocks are added together to determine the maximum amount of revenue

that a network business is allowed to recover from its customers.[25]

The four blocks are outlined in Table 3.4.

Table 3.4: Regulatory building blocks

|

Building block

|

Description

|

|

Operating

expenditure

|

Allowance

for recovering of operating costs such as forecast labour costs, maintenance

expenses and corporate expenses

|

|

Return

on capital

|

Allowance

for the recovery of capital invested by the business, which is calculated by

multiplying the regulatory asset base (RAB) by the allowed rate of return

|

|

Return

of capital

|

Allowance

for the depreciation of existing assets

|

|

Tax

allowance

|

Estimated

corporate income tax over the period

|

Source:

AER, Submission 36, p. 3.

3.34

In its 2013 report on electricity networks regulation, the PC explained

that the building block model consists of two equations: the revenue equation

and the asset base roll forward equation. These equations are as follows:

MAR=WACC × RAB+depreciation+operating expenditure+

tax +incentive

payments/penalties

and

new RAB=previous RAB –depreciation+capital expenditure

where:

MAR is maximum allowable revenue

WACC is the post-tax nominal weighted average cost of

capital

RAB is the regulatory asset base

tax equals the expected business income tax payable.[26]

3.35

The AER noted that the largest component of the building block approach

is the return on capital, which may account for up to two-thirds of the revenue

allowance. Operating expenditure can typically account for 30 per cent of the

revenue allowance.[27]

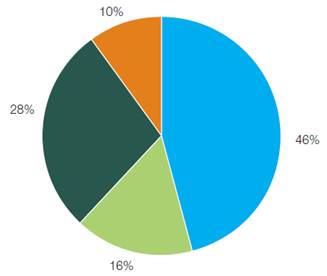

Figure 3.2 provides an indicative breakdown of electricity distribution network

revenue by each building block, based on the determination in place for the

Tasmanian distribution network service provider.

Figure 3.2: Indicative composition of electricity

network revenues, based on Tasmanian distribution

Source: AER, State of the

energy market 2014, p. 69.

3.36

The following paragraphs provide an overview of the key building blocks

and concepts involved in the determination process.

Regulatory asset base and costs of

capital

3.37

The return on capital is calculated by reference to the regulatory asset

base (RAB) and the weighted average cost of capital (WACC). Specifically, the

NER prescribe that the return on capital for each regulatory year in a RCP must

be calculated by applying a rate of return to the value of the regulatory asset

base (RAB) at the beginning of that regulatory year.

3.38

EnergyAustralia provided the following description of the RAB:

The RAB is, conceptually, the regulatory valuation of the

stock of (typically) physical assets used to provide network services. It

represents the cumulative depreciated valuation of the capitalised sunk

expenditure.

Each networks' RAB is calculated

at the start of the specified regulatory period based on the asset value at the

end of the previous regulatory period:

-

less the depreciation on that

opening asset base over the regulatory period;

-

plus the depreciated value of the

actual capitalised expenditure incurred in that period; and

-

plus an adjustment to ensure the

asset base is not eroded by monetary inflation.[28]

3.39

The WACC is the expected rate of return required by investors to induce

them to commit funds to the network business. The WACC for a firm is determined

by the return it pays on debt and equity,[29]

the two sources of funding for a firm, 'weighted in accordance to their

relative use and adjusted for the operation of the tax system'.[30]

3.40

To estimate the overall rate of return, the AER uses a nominal 'vanilla'

WACC, which is a combination of a nominal post-tax return on equity and a

nominal pre-tax return on debt.[31]

The WACC is calculated using the following formula:

WACCvanilla

= E(ke)EV + E(kd)DV

where

E(ke) is the return on equity, calculated with reference

to the risk-free rate, the firm specific equity beta and the premium per

unit of market risk (calculated using the capital asset pricing model)

E(kd) is

the return on debt, calculated as the sum of the risk-free rate and the

premium per unit of market risk

EV and DV are proportions of equity and

debt in total financing (the AER assumes that the debt weighting is 0.6 and the

equity weighting is 0.4).[32]

3.41

The PC has made the following comments on how WACC is used as part of

the revenue determination process for electricity networks:

...the regulator estimates the WACC of an efficient network

business at the start of the regulatory period. It is an estimate of the

financing costs of a typical network business with an efficient capital

structure and is used to determine the revenue allowance that network

businesses may recover. For clarity, this estimate is referred to as the

regulatory WACC, while the actual capital costs that businesses face to fund

their investments is referred to as the 'actual' WACC.

The regulator does not consider the individual circumstances

of any particular firm when calculating the regulatory WACC. In theory, this

creates incentives for businesses to source debt and equity financing

efficiently, while considering the financial risks associated with different

financing strategies. For instance, if a network operates in a low risk way,

and as a result, they can access lower cost financing, they can keep the difference

between the actual WACC and the regulatory WACC.[33]

3.42

The AEMC remarked that a good estimate of the WACC is 'essential to

promote efficient investment by network businesses'. It explained:

If the rate of return is set too low, network businesses may

not be able to attract sufficient funds to be able to make required investments

to maintain reliability and safety. Alternatively, if the rate of return of

return is set too high, network businesses may face an incentive to spend more

than necessary and consumers will pay inefficiently high prices.[34]

Capital and operating expenditure

3.43

This section considers capital expenditure, commonly referred to as

capex, and operating expenditure, or opex.

Definitions

3.44

For network businesses, capital expenditure is used for buying and

installing assets, such as poles, wires and other equipment used for

transporting energy, that are needed for the efficient operation of the network.

The AEMC provided the following comments about capital expenditure:

Some types of capital expenditure are relatively certain and

regular. However, more often capital expenditure is lumpy, typically varying

from year to year because capital assets are generally very costly but last for

a number of years. Network businesses earn revenue from capital expenditure

through return on capital (WACC multiplied by the regulatory asset base) and

return of capital, known as depreciation.[35]

3.45

Operating expenditure 'is spent on the non-capital cost of running an

electricity network and maintaining the assets'. Unlike capital expenditure,

the AEMC noted that operating expenditure is 'generally recurrent and

predictable from year to year'.[36]

How capex and opex are determined

3.46

The AEMC explained that as part of the determination process, the AER

approves an overall allowance of estimated capital expenditure at the start of

an RCP. The total capital expenditure allowance for the RCP is based on the

capital expenditure objectives and criteria set out in the NER. These require

the AER 'to determine the efficient costs a prudent network business would need

to meet or manage expected demand, comply with regulatory requirements

(including jurisdictional reliability standards) and maintain safety'.[37]

3.47

The regulatory arrangements for assessing operating expenditure are

similar to those for capital expenditure. Specifically, an overall estimate of

operating expenditure for each network business is determined at the start of

the regulatory period based on the efficient costs the AER considers a prudent

network business would incur. The NER provide 'the AER with discretion to use a

range of methods and information to determine the efficient operating

expenditure'.[38]

3.48

The AER must accept the forecasts submitted to it if it is satisfied

that a network service provider's proposed total capex forecast and total opex

forecast reasonably reflect:

-

the efficient costs of achieving the capex and opex objectives;

-

the costs that a prudent operator would require to achieve the

capex and opex objectives; and

-

a realistic expectation of the demand forecast and cost inputs

required to achieve the capex and opex objectives.[39]

3.49

The AER's approach to estimating total capital expenditure is outlined

in a guideline. Among other techniques, the AER uses economic benchmarking,

modelling and analysis to compare the capital expenditure proposed by a

business with estimates the AER develops. The NER also require that network

businesses undertake a public regulatory investment test (RIT) process for

major projects where expenditure exceeds $5 million.[40]

The AEMC advised that the RIT process is:

...designed to test whether the

businesses' proposed investment is the most efficient solution (eg whether it

is the most efficient way to meet the applicable reliability standards),

including allowing providers of non‑network solutions to propose

alternative approaches.[41]

Recent rule changes and upcoming determinations

3.50

The final section of this chapter briefly outlines the changes to the

NER made in recent years that have implications for upcoming revenue determination

processes. The AER has started to develop determinations based on these new

rules.

3.51

The rule changes sought to address inconsistencies in the framework and other

issues that may have contributed to high revenue allowances in previous

determinations. For example, regarding the previous approach to determining the

rate of return, the AER explained that the version of the NER in place at the

time:

...mandated inconsistent approaches to setting rates of return

for transmission and distribution businesses, and constrained the AER from

setting rates of return that reflected commercial practices. The AER was locked

into a parameter-by-parameter assessment of the rate of return, with limited

scope to consider the appropriateness of the overall allowance.[42]

3.52

The AEMC and AER outlined the following rule changes made in 2012 that

are relevant to revenue determinations:

-

the AER must set an allowed rate of return that reflects the

efficient financing costs of a benchmark efficient entity and must consider the

appropriateness of the overall rate of return, rather than looking at the

individual parameters that make up the rate of return in isolation;

-

network businesses are provided with incentives to make

cost-effective investment and operational decisions to promote efficient

outcomes for consumers (if the businesses are more efficient than the benchmark

they get rewarded, if not they get lower returns)—specifically:

-

the AER has the power to review the efficiency of capital

expenditure over an RCP that exceeds the efficient amount estimated by the AER;

if it is found that the expenditure was not efficient, the AER may decide that

the business cannot recover that expenditure during the next RCP;[43]

-

the AER may develop specific incentive schemes for capital

expenditure that provide incentives for network companies to incur efficient

capital expenditure;

-

networks are required to consult with consumers about their

expenditure plans and the AER regulatory determination processes have been made

more accessible to consumer representation; and

-

changes have been made to enhance the limited merits review

process (these are examined in Chapter 6). [44]

Regulatory proposals currently

under consideration

3.53

The first network businesses to have RCPs commence under the new rules

are currently having their revenue requirements assessed by the AER. As shown

in Table 3.3, these businesses are the Tasmanian electricity transmission

business, TasNetworks, and ACT and NSW transmission and distribution network

businesses. The next regulatory control period for these businesses commences

on 1 July 2015. The AER's final determinations are due by 30 April 2015.

3.54

Operating conditions for these businesses have substantially changed

since their previous determinations, particularly as a result of reduced

electricity demand and lower costs of capital. It appears that these changing

conditions, and the amendments to the NER, are encouraging substantially

different regulatory decisions to be made regarding the future revenue

requirements of these businesses. The draft determinations issued by the AER in

November 2014 challenged elements of the proposals submitted by the businesses.

For example:

-

the proposed rate of return was decreased—the rate of return

proposed by the businesses was 7.58 per cent for TasNetworks, 8.83 per cent for

the NSW businesses and 8.99 per cent for the ACT network business—the AER

proposed between 6.9 and 7.2 per cent; and

-

proposed operating expenditure was decreased—the AER proposed

cuts of between 10.3 and 38.6 per cent to the base operating expenditure

proposed by the ACT and NSW businesses.[45]

Committee comment

3.55

The AER's latest draft determinations represent a promising development.

It is, however, difficult to determine the weight that should be attached

to each of the various factors that may have led to this outcome. The recent rule

changes may have addressed certain flaws with the determination process,

resulting in the AER having greater flexibility when assessing proposals.

Lessons learnt following the previous regulatory period may mean the regulator

is more sceptical of forecasts presented to it. Public pressure may also be a

factor.

3.56

However, this is not the end of the matter. Although it seems the

regulator is more willing, or able, to reject exorbitant proposals, the

evidence taken by the committee through written submissions and public hearings

largely took place after the draft determinations were released. Some well-informed

submitters still questioned many of the fundamental principles applied in the

economic regulation of network businesses.

3.57

The next chapter starts an analysis of this evidence by considering in

detail how the return on capital and other building blocks are determined.

Navigation: Previous Page | Contents | Next Page