Chapter 2

The context of this inquiry

2.1

Some of the reasons for this inquiry are readily apparent. Over the past

several years, there has been ongoing and widespread concern in the community

about rising electricity prices and the actions of electricity network

businesses that have contributed to these increases. The attention given to

this issue has resulted in terms like 'gold plating'—that is, excessive

expenditure on 'poles and wires'—emerging into common parlance.

2.2

This is certainly not the first inquiry to examine high electricity

prices. Indeed, as some of the industry stakeholders were quick to point out, this

inquiry follows at least 17 other inquiries and reviews since 2010.[1]

These inquiries resulted in various changes to the rules underpinning the

regulation of networks; with the upcoming revenue determinations these new

rules are being tested for the first time.

2.3

This inquiry, however, differs from the others in several key ways. First,

it follows specific allegations by a whistle-blower that Energex, a Queensland

distribution network service provider, sought to mislead the regulator. Other concerning

and inefficient practices at Energex were also highlighted by the whistle‑blower.

Second, as this inquiry has taken place after the flurry of regulatory and

other changes made since 2012, and as the first revenue determinations since

these changes are being finalised, the committee can, to some extent, examine

these changes. Of particular interest to the committee is how network businesses

and the regulator have responded to both the rule amendments and changes to

market conditions. It is also evident that concern about high electricity

prices and their effect on consumers and economic activity has not gone away.

In fact, the latest regulatory proposals have been an additional source of

frustration in some quarters.

2.4

Finally, this inquiry is considering electricity network regulation in

the context of innovation and disruptive technologies, such as the rise of photovoltaic

panels and the potential for cost-effective battery storage. State-wide networks

with centralised generation and linkages between states that create an almost

national network have, overall, served Australia well. However, there is no

guarantee that this will be the most-effective model in the future. An

expensive but under-utilised network could mean that stranded assets will be

the next thorny issue in energy policy.

2.5

In summary, this inquiry builds on previous reviews by seeking to

uncover whether there are fundamental problems with the system of electricity

regulation in Australia. This chapter provides an overview of principal issues,

which will inform the discussion in the remaining chapters of the report.

High electricity prices and 'gold plating'

2.6

While the other components of electricity supply, namely generation and

retail, contribute to the prices end users pay for the electricity they use, the

concern about electricity prices in recent years has been linked to a

noticeable increase in the proportion of an electricity bill that is attributed

to network costs.[2]

For example, the Energy Users Association of Australia (EUAA) stated that

residential network prices in Queensland and New South Wales have more than

doubled, in real terms, between 2007 and 2013. Large industrial consumers have

faced even greater increases: the EUAA advised that some of its members

have seen their network tariffs increase by over 200 per cent during that same period.[3]

Cotton Australia compared the increases in electricity prices to the increases

in the prices of other goods and services; it noted that electricity prices

have significantly outstripped inflation during the past 15 years, with

electricity prices increasing by approximately 350 per cent since 2000, compared

to inflation of 45 to 50 per cent.[4]

Network cost trends, demand

forecasts and international comparisons

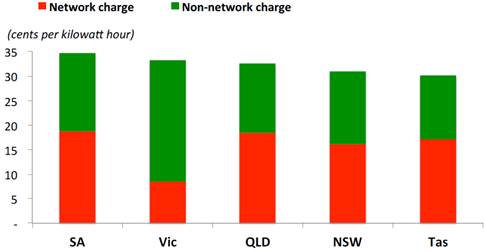

2.7

Network costs now represent between 30 per cent and 60 per cent of a

consumer's electricity bill.[5]

Figure 2.1 shows how the network costs differ between states.

Figure 2.1:

Average electricity network and non-network prices by jurisdiction in 2014

Source: Mr Bruce Mountain, Submission

19, p. 5.

2.8

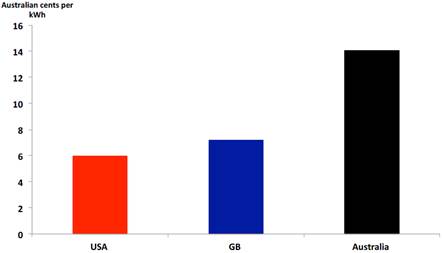

The high prices in Australia relative to other countries were noted.

Dr Gabrielle Kuiper from the Public Interest Advocacy Centre observed that

while the contribution of network costs to electricity prices can vary

significantly within Australia—for example, network costs in New South Wales

are double those in Victoria—all states have higher network charges than Great

Britain, Canada or the United States of America.[6]

Mr Bruce Mountain, the director of Carbon and Energy Markets Australia (CME),

an energy economics consultancy, supplied a chart that illustrated this point (Figure

2.2).

Figure 2.2: Network services charges for average usage

households in 2013

Note: PPP-adjusted exchange

rates, constant currency.

Source: Mr Bruce Mountain, Submission

19, p. 6.

2.9

Mr Mountain claimed that differences in population density between

Australia and other countries do not explain the network pricing outcomes. He

argued that:

-

Australia is one of the most urbanised countries in the world[7]

and although the National Electricity Market[8]

(NEM) covers an extensive geographic area, a large part of each state in the

NEM is neither inhabited nor covered by network infrastructure;

-

much of the additional length of Australia's networks consists of

'inexpensive single wire earth return or 11 kV [kilovolt] overhead distribution

lines', with an additional cost that is 'much less per kilometre than an

underground high voltage urban or metropolitan network' (he noted that

underground networks 'can typically cost many times more than overhead

networks');

-

much of the rural network 'has been funded fully or partially

from customers' capital contributions'; and

-

network density 'does not explain the changes in prices or

assets', given that changes in prices and assets occurred for both metropolitan

and rural distributors and the density of the networks increased while the

expenditure was taking place.[9]

2.10

Before further outlining some of the concerns about electricity pricing,

it is instructive to acknowledge that consumers value both low prices and a reliable

electricity supply. These two outcomes of an electricity system are related:

electricity prices need to fund maintenance and provide incentives for

appropriate levels of investment that respond to growth and ensure the supply

remains reliable. An example of this tension between price and reliability was

given by the Queensland distributor Energex. Energex noted that although its

network is now 'very safe and reliable', reliability has been a flashpoint in

the past. Mr Terence Effeney, Energex's chief executive officer,

explained:

If you go back just a decade or so, when there were severe

storms and high load conditions, our network did struggle to meet customers'

requirements. At the time, both government and customers expressed some extreme

dissatisfaction, and this led to what was called the Somerville review in those

days. We call it the EDSD review as well. That review led to a whole range of

mandated inputs which we then had to build and plan our network to. In

particular, it mandated security and service standards for our network, and it

also mandated maintenance and response programs.[10]

2.11

Nevertheless, in recent years there has been sustained community and

industry displeasure about the level of electricity prices. Further, there has

been growing recognition that rising network costs have been a significant

contributor to higher final prices. The increase in network costs has led to

allegations of excessive investment in the networks, known as 'gold plating'.[11]

2.12

In the absence of an alternative suitable explanation, the regulatory framework

has been identified as the culprit for high electricity prices.

Mr Bruce Mountain told the committee:

I do not believe there is any exogenous reason such as demand

growth, growth in customer numbers or growth in energy supply or quality of

supply that justifies the rather disastrous outcomes that have been observed in

these states. In fact, to the contrary, I think the rate of the Australian

dollar to the US dollar and other currencies has been very, very useful and in

our favour at a time when large capital items have been imported. If anything,

I would contend that the expenditure programs should have turned down.[12]

2.13

This over-investment, many have argued, indicates a failure of

electricity regulation. It is claimed that the regulatory rules encourage

network companies to engage in excessive, and inefficient, expenditure on

assets as the current regulatory arrangements provide that this expenditure

will be passed through to consumers, helping drive the network company's future

revenue and profits. It is also evident that, for state government-owned

networks, the dividends from increased profits provide a lucrative revenue

stream for their government owners.[13]

2.14

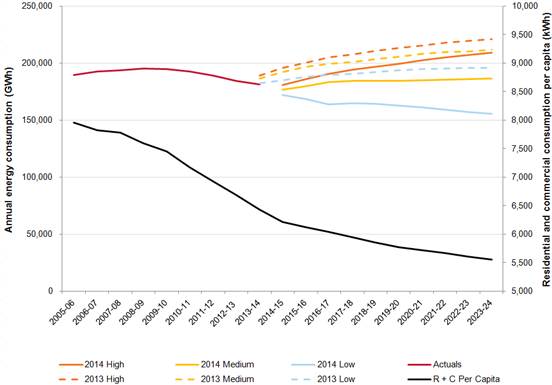

Another aspect of the over-investment submitters were concerned about is

that the forecasted increase in demand used to justify the investment was

incorrect. Demand has fallen and is forecast to be flat in the NEM in upcoming

years (see Figure 2.3). The following assessment of forecasted

electricity consumption published by the Australian Energy Market Operator

(AEMO) in 2014 highlighted the stagnant nature of demand throughout the

country:

Queensland is the only region in the NEM experiencing

industrial growth, due to LNG projects. It also has the strongest growth in

rooftop [photovoltaic (PV)]...installations, which drives down overall

consumption from the grid.

New South Wales experiences a decline in consumption, due to

reduced large industrial forecasts.

Victorian consumption is forecast to decline, driven by large

industrial and manufacturing plant closures, including the Point Henry

aluminium smelter in August 2014.

South Australian consumption is forecast to decline, with the

desalination plant reducing consumption due to the completion of operational

tests. Decreasing residential and commercial consumption is a result of the

highest existing levels of installed rooftop PV per capita across the NEM.

Tasmanian consumption is forecast to decline despite

increased production at the Norske Skog Boyer paper mill. The decline reflects

the lowest population growth in the NEM and high rooftop PV installations.[14]

Figure 2.3: Annual energy forecasts for the National

Electricity Market

(as at December 2014)

Note:

R + C is residential and commercial annual energy consumption.

Source: AEMO, National electricity forecasting

report 2014 update, December 2014, www.aemo.com.au/Electricity/Planning/Forecasting/~/media/Files/Other/planning/NEFR/2014/2014%20Updates/2014%20NEFR%20Update%20NEM.ashx

(accessed 23 March 2015).

2.15

The Department of Industry (the department) suggested that, despite

falling electricity consumption, new network investment could still be required

occasionally. Examples given included 'replacing electrical protection devices

and power lines to mitigate bushfire risk, upgrading metering infrastructure to

accommodate smart meters, and modifying equipment to deal with power flows from

rooftop solar systems'. Further, the department noted that there may be some

areas of the network where it is more critical to ensure reliability of supply

compared to others.[15]

2.16

However, it was argued that network companies have been shielded from

the change in demand. EnergyAustralia submitted that generation and retail, the

competitive aspects of the electricity sector that EnergyAustralia is involved

in, have 'felt the impact of lower demand', while the regulated monopoly

transmission and distribution services 'have continued to recover against their

regulated asset base at a higher rate per unit sold'.[16]

Furthermore, submitters questioned the flexibility of the regulatory system.

They noted that expenditure forecasts and the resultant high electricity prices

were locked in for five years when demand began to decline. For example,

in its submission the Electrical Trades Union of Australia stated:

While it is not possible to accurately predict the future,

important data such as demand projections should not be totally wrong, and

there needs to be sufficient flexibility in the regulatory process to allow

adjustments that protect consumers from having to foot the bill of bad

investment decisions via bloated AER determinations.[17]

Continued growth in prices and the

broader economic impact

2.17

Concerns about high prices have been examined by past inquiries. At a

rudimentary level, the concept of network businesses gold-plating their networks

appears to be widely acknowledged and understood. Despite this, many submitters

to this inquiry considered that little has been done to address this issue. In

particular, many submitters grappled with following question: why are prices

still increasing given the past investment and declining demand? The following

extract from the Central Irrigation Trust's submission is an example of the

frustration submitters expressed:

We have endured significant price increases with the promises

of upgrading an aged network. We now expect a significant drop in capital

expenditure and subsequent network prices. There is no justification for

increasing capital expenditure when total demand is decreasing and this trend

continuing. Some big energy users such as Holden will close their doors soon

and recognition of further demand decreases must occur.

As a customer we find the reliability of the network

satisfactory and do not see the need for further upgrades, for changed bushfire

prevention activities or hardening of the network against lightening and

storms.[18]

2.18

Electricity supply activities contribute to an energy sector that

comprises a sizable part of Australia's economy. The Energy Supply Association

of Australia advised that the 36 electricity and downstream natural gas

businesses it represents 'own and operate some $120 billion in assets, employ

more than 51,000 people and contribute $16.5 billion directly to the nation's gross

domestic product'.[19]

However, while the energy sector has grown, concern was expressed in

various submissions that high electricity prices are affecting the viability of

other industries. Submitters noted that network service providers were

'extraordinarily profitable entities'.[20]

The Central Irrigation Trust, which manages several irrigation districts in

South Australia, provided the following evidence of how high electricity prices

had affected businesses and economic activity in its region:

...in the 14 businesses that are part of the Riverland

association, there are a number of projects where people are looking at

significant investments for future developments and they are putting those on

hold until we can get some resolution of this...It is a significant issue in our

own business. We would love to put more people on, but, in fact, we have

had to decrease over time. You could say some of that is power and some of that

is the drought and the like. But it is putting on significant pressure and we

do have an unemployment issue, as does regional Australia. We also have the

capacity to drive productivity and GDP in Australia. We are an export dominated

industry. We bring revenue into Australia from those exports and we want to

continue to do that. Unfortunately, I cannot give you the exact numbers, but

you can see how SA Power Networks are growing. You have got the numbers in

their annual report. Most of that growth is coming out of our businesses.[21]

2.19

Another specific instance of businesses suffering under the burden of

high electricity prices was provided by Canegrowers Isis, which gave the

example of a Queensland canegrower whose electricity costs have increased by 80

per cent in nominal terms over the past five years:

In 2010 his electricity costs for supplying the water to his

property and applying it onto the property were $20,800, or about eight per

cent of his gross income. In 2014, five years later, the electricity cost to do

roughly the same task was $37,500, and equated to about 23 per cent of his

gross income. That is a significant change, from eight per cent to 23 per cent.[22]

2.20

Large energy users also reported significant increases in their

electricity network costs. Big Picture Tasmania, which represents large energy

intensive companies in Tasmania that are directly connected to the high voltage

network, stated that 'since 2008 transmission costs have effectively doubled'

for the businesses it represents. Big Picture Tasmania described this as a

'perverse situation' that has 'undermined Tasmania's economic and social

security'. It added:

Allowing this perverse situation to continue without

significant reform by Federal and State Governments is bordering on neglect.[23]

2.21

One submitter observed that energy costs 'are a fundamental building

block of any economy', and although Australia 'should have cheap energy', it

does not. The submitter presented the following assessment of the effect

that high electricity prices are having on Australia's economy:

Electricity and gas prices are globally uncompetitive and

have risen so rapidly that they are causing social damage as retail customers

simply cannot afford the product. The current explicit high energy price

policies being followed by the government are hollowing out the Australian

economy. Mineral processing industries are leaving our shores, manufacturing

has been decimated and our economy is being reduced to a 'houses and holes'

economy, reliant on mining and housing to drive the economy.[24]

Impact on other reforms

2.22

It was also noted that high electricity prices were undermining other

reforms, such as water efficiency efforts. The New South Wales Irrigators'

Council (NSWIC) explained that electricity 'has become a major input factor in

irrigated agriculture as more irrigators have upgraded their on-farm equipment

to conserve water and remain competitive'. This has resulted in productivity

gains and water savings, however, irrigators' electricity use and costs have

increased. For irrigators that have implemented water efficiency measures, the

NSWIC reported that rising electricity prices have presented irrigators with

the following dilemma:

The trade-off between water efficiency and energy intensity

is extremely difficult to reconcile in irrigation and as a consequence of the

escalating electricity costs many irrigators have taken drastic measures

(including locking off their pumps or converting back to diesel energy) and

reverted back to low energy but water-intensive production methods. The impacts

in terms of efficiency and productivity are immense and continuously

increasing.[25]

2.23

Canegrowers Isis similarly noted that efficiency gains quickly diminish

when electricity prices increase and, as a result, irrigators are less willing

to adopt or further invest in improved technologies.[26]

An uncertain future: the rise of 'disruptive technologies' and concern

about a 'death spiral'

2.24

From 2000 to the start of the global financial crisis in 2007–08,

networks were faced with increasing demand and the need for ageing assets to be

replaced or upgraded. Mr Terence Effeney, the chief executive officer of

Energex, stated that the load on Energex's network increased by about 40 per

cent over six years, largely due to the widespread installation of air

conditioning. He explained:

Fifteen years ago about 25 per cent of homes in South East

Queensland had air conditioning. Now over 75 per cent of homes will have air

conditioning. Even with the global financial crisis, which occurred across 2007

and 2008, we were still experiencing record growth, and, in fact, across 2008

and 2009 we were still seeing some of the greatest demands that we had seen,

with over 120 additional homes and businesses connecting to our network every day.[27]

2.25

Indeed, summer peak demand in Queensland increased significantly during

the 2000s decade. The peak demand during the summer months of 1999–00 was

around 6,300 megawatts (MW); by 2009–10 summer peak demand had increased to

around 8,900 MW.[28]

However, AEMO figures indicate that the growth in maximum demand in Queensland

during the 2000s largely occurred during the first half of the decade.[29]

Although maximum demand was around four per cent higher in the summer of

2006–07 compared to the previous year, it fell sharply in the following year.

Between 2005–06 and 2009–10, maximum demand increased by approximately seven per

cent, around 1.5 per cent a year on average. Table 2.1 shows the AEMO's maximum

demand figures for Queensland between the summers of 2005–06 and 2013–14.

Table 2.1: Queensland

maximum demand, summer, various years

| Summer |

Residential and commercial

maximum demand (MW) |

Operational maximum

demand (MW) |

| 2005–06 |

6,414

|

8,280

|

| 2006–07 |

6,774

|

8,611

|

| 2007–08 |

6,260

|

8,086

|

| 2008–09 |

6,645

|

8,707

|

| 2009–10 |

6,803

|

8,897

|

| 2010–11 |

6,714

|

8,826

|

| 2011–12 |

6,524

|

8,714

|

| 2012–13 |

6,260

|

8,479

|

| 2013–14 |

6,191

|

8,374

|

Source:

AEMO, National electricity forecasting report 2014: Final NEM and regional

forecasts data – Queensland, June 2014, www.aemo.com.au/Electricity/Planning/Forecasting/~/media/Files/Other/planning/NEFR/2014/2014%20Updates/NEFR_2014_QLD_forecasts_template_values.ashx

(accessed 16 April 2015).

2.26

In any case, demand has fallen throughout the NEM and is not predicted

to return to its previous growth rate. Consumers are also already increasingly

becoming involved in their own electricity generation. The committee was told

that in 2008 there were just over 14,000 solar photovoltaic (PV) systems in

Australia; as at February 2015 that were over 1.3 million rooftop systems and

another 900,000 solar hot water systems.[30]

2.27

The starting point for a discussion about the future of Australia's

electricity networks is the so-called 'death spiral'. The concept of a death

spiral follows the line of reasoning that high prices encourage consumers to

reduce their energy consumption and/or to generate their own electricity. The EUAA

provided the following statement that discussed the concept:

Over the past five years it has become apparent that

electricity demand has declined and has significantly decoupled from economic

growth. This has been driven in large part by consumers reducing their

consumption in response to the dramatic increases in network prices. In

addition, consumers are increasingly moving to self-generation as the relative

costs of distributed generation are becoming more attractive, thereby further

reducing the energy being delivered by the networks. The networks have

responded by further increasing their prices to recover their guaranteed

revenues over a reduced volume.

As a consequence, network assets are becoming increasingly

under-utilised and the industry's productivity is in serious decline.

The natural outcome of the continuation of these trends is

the well documented 'death spiral'—i.e. as demand continues to decline and the

move towards distributed generation increases, the burden of paying for the

networks' costs will be placed on a smaller consumer base until those consumers

can no longer afford to stay connected to the network.[31]

2.28

A death spiral suggests that network assets are currently overvalued,

with the likely future outcome being stranded assets.[32]

On this matter, the Bundaberg Regional Irrigators Group suggested that high

electricity prices were not only affecting the competitiveness of its members

in the sugar industry, but were also 'destroying demand for electricity',

'hastening the change to alternative energy sources' and in turn 'threatening

the viability of...network investments and increasing the risk of electricity

assets being stranded'.[33]

2.29

The current regulatory proposals before the regulator caused some

submitters to suggest that the death spiral was now evident. Referring to Ergon

Energy's regulatory proposal, Mr Warren Males from Canegrowers claimed that

rather than the proposal realistically reflecting the change in demand, a

reading of it revealed the opposite. Mr Males stated:

In other sectors of the economy, if use of your product is

falling, generally you put out a sales price to try and encourage an uptake.

That does not work in the electricity market. If use is falling, then price

goes up so that you can get your revenue cap again. And, if use falls further,

then price goes up further. So it is really a bizarre twist in an energy-rich

economy.[34]

2.30

Anecdotal evidence of the death spiral was also supplied to the

committee. For example, Mr Tom Chesson, a member of the Agriculture Industries

Electricity Taskforce, gave the following account of a business seeking to

minimise its reliance on the grid:

Last week I was speaking to a grower down in the Riverina who

is 10 metres away from his transmission pole. He has just put in a diesel

pump. It is already happening. It used to be that diesel was roughly twice as

expensive as electricity. It is the other way around now...[W]e are all looking

at renewables. A lot of my members have packing sheds and a lot of the dairy

industry already has a 40 per cent uptake of solar panels for their sheds to

try to chill the milk and other things. So we are looking at all options now.

They are all on the table and a lot of them are starting to look far more

attractive, which then will start the death spiral of our electricity networks,

which in some states we still own. So it is a very odd business model where we

are seeing people driven off the network.[35]

2.31

Submitters expressed concern that billions of dollars in network assets consumers

have paid for over many years are at risk. Mr Robert Mackenzie from Canegrowers

Isis stated that continued price rises cannot be absorbed. He expected the

result will be 'a Rolls-Royce network across the whole industry and no

customers'. He continued:

You will not have anybody to buy the power, and you will have

a lot of stranded assets. That is ridiculous. Those assets were bought and paid

for many, many years ago, to a large extent, and I suggest to you that

individuals contributed to the construction of those assets over long periods

of time. If it gets to be just a ghost, left to rot, because there is no way we

can use it, what is the point of that? There are literally billions of dollars

at stake here, both in the irrigation scheme, the on-farm infrastructure and

the electricity network.[36]

2.32

The implications of a death spiral and the rise of emerging technologies

are considered further in Chapter 8.

Privatisation

2.33

Finally, it should be noted that this inquiry took place while proposals

to privatise state government-owned network assets in Queensland and New South

Wales through leasing arrangements were debated and taken by incumbent governments

to their respective state elections.

2.34

The terms of reference for this inquiry does not include consideration

of the merits of these proposals; however, they are relevant in the context of regulatory

arrangements and the performance of network companies. In particular, evidence

received by the committee discussed:

-

whether public or private ownership affects the prices consumers

pay;

-

the implications of state governments being involved in setting the

policy that underpins electricity regulation while also receiving dividends and

other payments from the companies they own; and

-

if the regulatory arrangements have resulted in unnecessary and

inefficient investment with companies receiving excessive rates of return based

on this investment, whether this can be remedied before privatisation.

2.35

These issues are considered in Chapter 5.

Concluding comment

2.36

Electricity costs are a significant burden on households and businesses.

The committee is concerned that the high electricity prices experienced

for several years have damaged the economy, particularly the sectors exposed to

intense international competition. As electricity is an essential input to

business activity, the revenue and profits enjoyed by the electricity network

monopolies detract from the profits of businesses operating in the remaining

sectors of economy. This outcome is made even worse if the high network costs are

a result of perverse incentives in the regulatory rules that encourage

significant investment in an electricity network that may not be used to the

same extent in the future.

2.37

The next two chapters will commence a detailed study of the regulatory

framework by considering how the revenue for a network business is determined.

Navigation: Previous Page | Contents | Next Page