Chapter 2

Cooperatives, mutuals and member-owned firms

2.1

The committee received evidence during the inquiry which used the terms

co-operative, mutual or member-owned firm interchangeably. The approach taken

in this report is informed by the Business Council of Co-operatives and Mutuals

(BCCM), who describe their member organisations as Co-operative Mutual

Enterprises (CMEs). The statement by Mr Graeme Nuttall, who in 2012 reviewed

employee ownership in the UK for the Department for Business, Innovation and

Skills, probably put it more succinctly by stating that, 'All co-operatives

are mutuals, but not all mutuals are co-operatives'.[1]

The committee would add...but both are member-owned firms.

2.2

As the peak representative body for CMEs in Australia, the BCCM

contends that:

...CMEs are not well understood in markets or by regulators in

Australia. They are formed to pursue different purposes from investor-owned

companies but they exist and compete in the same markets as those entities. A

greater understanding of their purpose and their governance model will provide

a basis for the development of policies that enable Australia to obtain the

best value from this business model.[2]

2.3

Contextually, BCCM sees CMEs contributing widely to the Australian

economy.

...They distribute wealth, control and ownership...they are

self-help organisations that bring diversity, competitive forces and consumer

choice to markets. They address market failure by enabling smaller market participants,

enterprises or individuals, to compete in markets that favour larger entrants.

Finally, they present an alternative public service delivery model for

government that combines commercial focus, community ownership and a commitment

to the pursuit of the social purpose. The submission will provide a comparison

between the privatisation and the mutualisation of government services and

assets.[3]

2.4

The BCCM doesn't distinguish the two business models, rather it combines

the two types of enterprise and differentiates them only in terms of the

regulatory environment they operate in, and their contrast with other business

models:

CMEs include both not for profit and for profit entities.

They run lean and efficient business operations for their members and their

communities...There are regulatory differences: co-operatives are incorporated

and regulated under state and territory laws, mutuals are regulated under the

federal Corporations Act.

Despite regulatory differences, CMEs share important

characteristics that distinguish them from companies. They are a self-help

response to the mutually identified needs of individuals or organisations. They

are driven to meet both financial and social goals.[4]

Table 1.1 – Types of cooperatives and mutuals

|

Type

|

Description

|

Examples

|

|

Consumer owned

|

- Members jointly purchase programs and services, improving value for money and access to expert advice.

-

Formed by members to increase their bargaining power in the market (e.g. bulk buying from suppliers to gain volume discounts).

|

- Consumer

retail societies:

The Barossa

Community Store

Co-op

- Collective

purchasing cooperatives:

The Co-op (University

Bookshop) (also

see consortium

enterprises)

- Customer

owned banks

and credit

unions: Teachers Mutual

Bank, bankmecu

-

Motoring clubs:

NRMA, RAC

WA

-

Health mutuals

and non-profit

health insurers:

HCF, Australian Unity

|

|

Employee owned

|

- Provide members with an income as well as empower employees with a stake

in the organisation’s decision-making process.

-

Pursue long-term strategies that smooth out the peaks and troughs of the business cycle.

|

- Employee

benefits trust

cooperatives: Sunderland Homecare

Cooperative

- Worker

cooperatives: Cooperative

Home Care,

Nundah Community Enterprise

Cooperative

-

Not all

employee-owned businesses

are cooperatives

(for example,

accounting and

legal firms

are limited

liability partnerships).

|

|

Enterprise owned

|

- Enable self-employed members and member businesses or community groups to band together and find strength in numbers.

-

Includes secondary cooperatives, a consortium cooperative where all members are cooperatives and consortium mutuals which umbrella organisations with like needs.

|

- Consortium

cooperatives: Community

Child Care Cooperative

- Community

cooperatives: Dandenong

and District Aboriginal

Cooperative

- Agricultural

cooperatives: Murray

Goulburn, CBH Group;

Coleambally Irrigation

Cooperative Limited

- Market

trader cooperatives:

Capricorn Society,

Hunternet

-

Artisan cooperatives:

Associated Newsagents Cooperative

SA, Hairdressers’ Cooperative

|

|

Hybrid – multi- stakeholder

|

-

Hybrid cooperatives

combine any

elements of

the three

other types

of cooperatives.

|

-

Housing cooperatives:

Common Equity

Housing Ltd

– a consumer

and enterprise

cooperative

|

2.5

Table 1.1 (above), produced by Ernst and Young (EY) describes the

typical types of CMEs currently operating in Australia, and provides examples

of each type.

2.6

In their submission, EY submitted that the difference between

co-operatives and mutuals is historical, except for the fact that co-operatives

have to subscribe to the seven principles of the International Co-operative Alliance

(see para 2.10). Their submission added that historically the term mutuals

referred to 'member-owned businesses in banking, superannuation and healthcare.'[5]

Definitions

2.7

The following definitional sections provide descriptions of the types of

co-operatives and mutuals that fall under these business models.

Co-operatives

2.8

The defining characteristic of a co-operative is that it is owned by

their members and acts in the interests of their members, rather than to

provide benefit to shareholders or investors. Two types of cooperatives are

provided for under current Australian law: Distributive and Non-Distributive.

2.9

A Distributive Co-operative, commonly known as a Trading Co-operative, is

typically a commercial enterprise where members may share the financial surplus.

Whereas a Non-Distributive Co-operative uses any surplus to 'further the

activities of the co-operative'.[6]

2.10

Co-operative Development Services Ltd provides a list on their website

of further characteristics that both types of co-operative typically have. A

trading

co-operative is characterised by the following:

-

A member must support an activity associated with the primary

activity of the co-operative, e.g. a dairy farmer is required to deliver an

agreed quantity of milk to the co-operative in any given period to remain an

'active' member.

-

A trading co-operative must have a share capital.

-

Disclosure statements are required for formation and issuing

shares.

-

Bonus shares can be issued to members upon asset sale or

revaluation.

-

Shares can be issued at a premium.

-

Members may be required to subscribe to more shares or lend money

to the co-operative.

-

Surplus funds can be distributed to members by way of a 'limited'

dividend on shares held, bonus shares and/or a rebate in proportion to the

business done by the member with the co-operative.

-

Surplus funds from winding up is distributed to members in

proportion to share capital held by a member.

2.11

A trading co-operative or distributive co-operative, can provide a

pecuniary benefit to members, and as such, is subject to a disclosure regime

under Australian

co-operatives legislation. A non-trading co-operative is not subject to the

disclosure regime. Surplus funds from winding up are distributed to another

similar

'not-for-profit' organisation approved by members of the co-operative.

2.12

A non-trading co-operative has the following features:

- A member must maintain a relationship with the co-operative

associated with its primary activity, e.g. a parent must have a child enrolled

in a child care co-operative to be an 'active' member. Payment of a regular

subscription by a member is also sufficient to establish 'active' membership of

a non trading co-operative.

-

No disclosure statement required for formation (except NSW) or

issuing shares.

-

Shares cannot be issued at a premium.

-

Bonus shares cannot be issued either from asset revaluation or

sale, or from profits.

-

Members cannot be compelled to acquire more shares or lend money

to the co-operative.

-

Profits made from trading are reinvested in the co-operative

and/or distributed to a charitable organisation.[7]

2.13

To mark the UN International Year of Co-operatives in 2012, the

Australian Bureau of Statistics published an article setting out the typical

characteristics and activities. The article described how both the distributive

and non-distributive

co-operatives would 'require their members to maintain an active relationship

with the co-operative'....and this can 'include purchasing or supplying goods or

services, paying an annual subscription, or being a tenant of a housing

co-operative.' The article also described the range of activities that are

often undertaken by co-operatives in Australia:

[C]onsumer (buying and selling goods to members at a

competitive rate); marketing (branding, marketing and distributing members’

products and services); service (providing services to members, such as health,

electricity or housing); and community (resource, information and skill sharing

that encourages ownership and participation). Financial co-operatives comprise

credit unions, mutual building societies and friendly societies.[8]

Australian tax law

2.14

Co-operative companies are defined in Australian tax legislation as a company

that has certain limitations on its shareholding and trading, and that has one,

or all, of the following as its object:

- the acquisition of commodities or animals for

disposal or distribution among its shareholders;

- the acquisition of commodities or animals from its

shareholders for disposal or distribution;

- the storage, marketing, packing or processing of

commodities of its shareholders;

- the rendering of services to its shareholders;

- the obtaining of funds from its shareholders for

the purpose of making loans to its shareholders to enable them to acquire land

or buildings to be used for the purpose of residence or of residence and

business.[9]

International Co-operative Alliance

principles

2.15

The International Co-operative Alliance sets out a list of principles that guide how co-operatives should operate,

and that distinguish them from other forms of enterprise:

1. Voluntary and Open Membership

Co-operatives are voluntary organisations, open to all

persons able to use their services and willing to accept the responsibilities

of membership, without gender, social, racial, political or religious

discrimination.

2. Democratic Member Control

Co-operatives are democratic organisations controlled by

their members, who actively participate in setting their policies and making

decisions. Men and women serving as elected representatives are accountable to

the membership. In primary co-operatives members have equal voting rights (one

member, one vote) and co-operatives at other levels are also organised in a

democratic manner.

3. Member Economic Participation

Members contribute equitably to, and democratically control,

the capital of their co-operative. At least part of that capital is usually the

common property of the co-operative. Members usually receive limited

compensation, if any, on capital subscribed as a condition of membership.

Members allocate surpluses for any or all of the following purposes: developing

their co-operative, possibly by setting up reserves, part of which at least

would be indivisible; benefiting members in proportion to their transactions

with the co-operative; and supporting other activities approved by the membership.

4. Autonomy and Independence

Co-operatives are autonomous, self-help organisations

controlled by their members. If they enter into agreements with other

organisations, including governments, or raise capital from external sources,

they do so on terms that ensure democratic control by their members and

maintain their co-operative autonomy.

5. Education, Training and Information

Co-operatives provide education and training for their

members, elected representatives, managers, and employees so they can contribute

effectively to the development of their co-operatives. They inform the general

public - particularly young people and opinion leaders - about the nature and

benefits of co-operation.

6. Co-operation among Co-operatives

Co-operatives serve their members most effectively and

strengthen the co-operative movement by working together through local,

national, regional and international structures.

7. Concern for Community

Co-operatives work for the sustainable development of their

communities through policies approved by their members.[10]

Mutuals

2.16

Similarly, the distinguishing characteristic of a mutual organisation is

that it 'is owned by its members, and run

exclusively for their benefit, rather than for the benefit of outside

investors'.[11]

2.17

Internationally, mutuals tend to be larger organisations than co-operatives,

and specialise in specific business sectors. In Canada mutuals are often

insurance companies where the policy holder is a participant in the business.[12]

According to

Co-operatives and Mutuals Canada this results in a 'very stable and successful

business model'. [13]

2.18

In the UK the Communities and Local Government Committee used the

definition of a mutual from Mutuo who described mutuals in similar terms to

co-operatives:

...organisations which are owned by, and run for the benefit of

their current and future members. These are different to social enterprises in

that a large proportion of the business should be owned by either employees

and/or the local community.

2.19

However the UK committee's report also pointed out the differences

between the two concepts, differentiating them on the basis that co-operatives

subscribe to the following principles of the International Co-operative

Alliance:

An autonomous association of persons united voluntarily to

meet their common economic, social, and cultural needs and aspirations through

a jointly-owned and democratically-controlled enterprise...[14]

2.20

The advantages of the mutual model in comparison to other business

structures was highlighted by Regis Mutual Management set out what it sees as

the economic benefits unique to mutual enterprises:

Cost effectiveness

– Mutuals deliver better value, broader and more appropriate

insurance protection for members as well as a reduction in overhead costs.

Increased Competition

– Mutuals drive competition and diversity into the market. This is

particularly important in the financial services sector.

Supporting Australian Financial Services Sector - Insurance or

reinsurance business that might otherwise be ceded to foreign markets can be

retained within the domestic market.

Creating Jobs

- The use of mutual structures has the potential to create greater

domestic employment in areas which benefit the community.[15]

The scale and extent of the sector

2.21

The scale of CMEs in Australia and

internationally is significant. The UN's International Year of Cooperatives

(IYC) was launched in recognition of the scale of the sector, citing the

International Cooperative Alliance's membership of 800 million alone.[16]

2.22

The UN IYC was also promoted on the basis that cooperatives have the

ability to extend far beyond the reach of other businesses in areas such as job

creation, social inclusion and achieving positive environmental outcomes:

Cooperatives represent a model of economic enterprise, which

when effectively implemented, promotes democratic and human values as well as

respect for the environment...Cooperatives help create, improve and protect

income as well as they generate employment opportunities and contribute to

poverty reduction. As of 2007, cooperatives were responsible for more than 100

million jobs worldwide. Cooperatives also promote social integration and

cohesion as they are a means of empowering the poor and marginalized groups. As

such, they also play an ever-increasing role in the promotion of gender

equality and the social and economic empowerment of women. [17]

2.23

In Australia the Australia Institute estimates that eight in ten

Australians are members of some form of CME, but tellingly, only a fraction of

that number actually realise it.[18]

2.24

The Australia Institute also estimated the size of the sector in

Australia and worldwide, the economic and social impact it has through the

creation of jobs, and the types of industries where cooperatives and mutuals

thrive:

Table 1.2: Overview of member owned businesses

|

Worldwide

|

Australia

|

|

1,000

million members

|

13.5 million members (estimated)

|

|

$1,700 billion annual

turnover

|

1,600 co-operatives

|

|

100 million employed

|

103 financial mutuals

|

|

Three billion livelihoods secured

|

$83 billion combined total assets of

financial mutuals

|

|

23% share of global insurance market

|

$17 billion: top 100 turnover in 2011

|

|

196 million

credit union

members

|

Seven million automobile club members

|

Source:

Cooperatives UK (2011); The UK co-operative economy 2011 – Britain’s return to

co-operation; World Council of Credit Unions; ABS (2012); socialbusiness.coop,

Cooperatives Australia (2012).

Measuring CMEs

2.25

A key element in measuring the economic and social impact of the work of

CMEs is the collection of data that illustrates the work of CMEs across a

variety of sectors, as well as the effect the Co-operatives National Law (CNL)

is having on the sector.

2.26

Robyn Donnelly, a former employee of the NSW Registry of Co-operatives

who was on the intergovernmental committee that developed the CNL, submitted

that the paucity of data on the breadth of activity by CMEs is preventing a

full picture of the sector being developed, and thus hindering the development

of appropriate policies to address the issues facing the sector:

The development of good policy requires information. There is

no national database for co-operatives. State Registrars do not generally

publish statistics about the number of co-operatives in their jurisdictions or

the number of co-operatives that transfer incorporation or that are

deregistered. Unlike the monthly publication of statistics by companies there

is very little information to test the impact of any regulation for

co-operatives. [19]

2.27

The Mercury Centre in Sydney contended that the lack of data and

subsequent understanding of co-operative and mutual enterprises (CMEs) in key

government agencies is systemic and detrimental:

The BCCM summary identified that the key barriers are those

areas of recognition, education and regulation. The Mercury Centre concurs with

this assessment, particularly in the context of government regulation,...However,

the Mercury Centre considers that further important issues include (1)

structural efficiency and organisational capacity, (2) measurement and impact

and (3) community and public asset ownership.[20]

2.28

To help alleviate this lack of data around the sector, BCCM commissioned

the University of Western Australia's Co-operative Enterprise Research Unit

(CERU) to undertake a study into the top 100 CMEs in Australia. Dovetailing

with this work is the continued development of the Australian Co-operative and

Mutual Business Index (ACMI) that commenced in 2012, also being undertaken by

the Co-operative Enterprise Research Unit (CERU) within the University of

Western Australia (UWA) Business School. The research is designed to map the

size and structure of the sector, to provide a 'better understanding of these

Australian Co-operative and Mutual businesses and their contribution to the

national economy.'[21]

2.29

The initial findings estimated the combined turnover of these

enterprises was approximately $25 billion, while

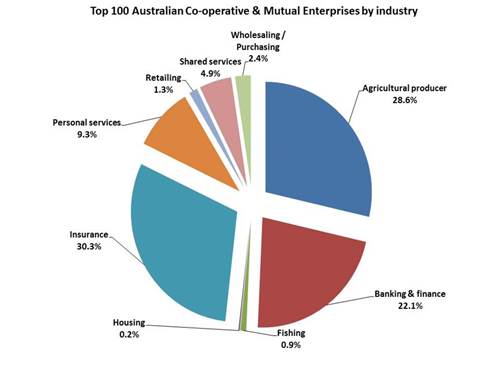

their combined assets amounted to $108 billion.[22]

The pie chart (Figure 1) below illustrates the diversity of the sector, with

CMEs active in a number of key industries.

Figure 1

Australia’s Top 100 CME by industry sector T. Mazzarol (2014)

2.30

A breakdown of these figures by industry and overall value, including earnings

and net profit after tax is set out in Table 1.3 below:

Table 1.3 Top 100 Australian Co-operative and Mutual Enterprises[23]

|

Sector

|

Number

|

Combined

Turnover ($m)

|

Median

Turnover ($m)

|

Median

EBIT ($m)

|

Median

NPAT ($m)

|

Combined

Assets ($m)

|

|

Agricultural

sector

|

13

|

7

217.2

|

210.0

|

0.4

|

0.8

|

4

376 700

|

|

Banking

and Finance

|

38

|

5

570.9

|

78.5

|

7.1

|

4.6

|

84

476 700

|

|

Fishing

|

2

|

228.8

|

114.4

|

1.7

|

1.3

|

66

700

|

|

Housing

|

1

|

41.2

|

41.2

|

1.8

|

1.8

|

683

800

|

|

Insurance

|

25

|

7

638.8

|

106.4

|

9.0

|

9.0

|

10

781 100

|

|

Personal

Services

|

6

|

2

336.6

|

477.6

|

38.8

|

36.2

|

7

003 300

|

|

Retailing

|

7

|

335.9

|

28.7

|

0.4

|

0.3

|

168

500

|

|

Shared

Services

|

2

|

1

237.8

|

618.9

|

9.8

|

7.1

|

110

500

|

|

Wholesale/Purchasing

|

6

|

601.6

|

83.3

|

0.6

|

0.4

|

186

100

|

|

Total

|

100

|

25

208.8

|

|

|

|

107

853 000

|

Notes to table: EBIT = earnings

before interest and tax; NPAT = net profit after tax.

2.31

To supplement this research BCCM recommended that data should be

collected at a state and territory level and then collated at a federal level. An initial first step in this process should be for

the ABS to begin regular collecting/disaggregating and reporting on relevant data

across the CME sector.[24]

Recommendation 1

2.32

The committee recommends that the Commonwealth Government ensures that a

national collection of statistics and data is undertaken to provide an accurate

picture of the scale and extent of the co-operative and mutual sector.

The diversity of co-operatives

2.33

As illustrated at Figure 1 above, CMEs operate in almost every sector of

the economy. The committee received evidence from a cross section of these

organisations.

2.34

The Voluntary Parents Services Co-operative appeared before the

committee in Sydney and explained how they provided a service which brought

parents together in fundraising efforts for schools across NSW. The

co-operative has reportedly raised $100 million.[25]

2.35

Also in the education field, Australia Scholarships Group (ASG) is a

co-operative of parents established more than 40 years ago to assist them to

plan for the children's education. As the largest member-owned education

services provider in Australia and New Zealand, ASG provides a range of

education plans across public, independent and private school systems, to more

than 155 000 members.[26]

2.36

Supporting the tertiary education sector is the Co-op Book Shop, an

institution across Australian university campuses. It operates in half of

Australia's universities with 60 book shops and is Australia's largest

co-operative with nearly two million members.[27]

2.37

Yenda Producers Co-operative are a growers' co-operative of around 1550

producers in the Riverina region of New South Wales. The committee heard that

while they have similar goals to other business entities in that they have to

make a profit, the impact of their activities in the local community goes well

beyond that:

In the local area, we employ 80-odd local people and their

families who contribute to our local community. The wages bill is around $4½

million in the year just gone. As well as that, we support over 100 local

charities and schools—you name it; if someone puts their hand up, generally we

are there to support them in the local area. We are a distributing co-op, so we

do pay rebates and dividends back to our shareholders. In the last five years,

those dividends and rebates have amounted to over $7 million back into the

local community.[28]

2.38

A very different co-operative of bus operators in Victoria also provided

evidence to the committee. The Bus Association Victoria (BusVic) is a member-owned,

voluntary professional association for Victoria's private, accredited bus and

coach operators. The co-operative represents its members in a variety of ways

including advocacy with respect to their relations with government, which

includes contract negotiations and legislative and regulatory compliance

issues.[29]

2.39

The Central New South Wales Renewable Energy Co-operative Ltd (CENREC)

and the Community Power Agency Co-operative Ltd are two organisations in the

growing co-operative energy sector. CENREC was formed by a number of community

members in Bathurst and Orange to invest in a proposed project by Infigen

Energy to develop a windfarm at Flyers Creek.[30]

Community Power Agency Co-operative Ltd provides support some of the 60

community energy projects around Australia.[31]

2.40

Another organisation established to assist and support other

co-operatives and social enterprises, is the Mercury Centre Co-operative. The

Mercury Centre advises business on how to establish and develop social

enterprise business models through collaboration and shared resources built on

community and ethical values.[32]

2.41

The community and social housing sector also features many co-operative

organisations. SouthEast Housing Co-operative Ltd. in Victoria told the

committee that while the sector is relatively small in Australia to date,

internationally it is the preferred model for the provision and maintenance of

social housing.[33]

2.42

In response to community concerns around the lack of affordable GPs and

healthcare, the National Health Co-operative was established in 2006 in the West

Belconnen community of North Canberra. The co-op is now open at six locations

in Northern Canberra. These clinics are fully accredited to the RACGP 4th

Edition Standards and Charnwood is also accredited as a GP Registrar training

practice. Regular clinics are also conducted at six nursing homes closely

located to the practice sites. Members have access to bulk-billed GPs and

allied health visits (subject to MBS guidelines and regulations), and 30,000

people have now registered as patients.[34]

Mutuals

2.43

Many of the largest mutuals provided evidence to the committee. The

Customer Owned Banking Association (COBA) is the peak body for Australia's

credit unions, building societies and mutual banks. The sector represented by

COBA are collectively the largest holder of household deposits outside the four

major banks.[35]

2.44

The National Roads and Motorists' Association (NRMA) are another one of

Australia's most well-known and largest mutuals with 2.4 million members in NSW

and the ACT. They, along with other motorists' organisations and car clubs

under the banner of the Australia Automobile Association, have seven million

members. The NRMA is a for-profit organisation.[36]

2.45

Australian Unity is a large mutual organisation that has been operating

for 175 years, and provides health care, aged care and financial services to

around 850 000 people. Again, it is run on a for-profit basis, but as with all

mutuals, these profits are re-invested in the organisation for the benefit of

its members.

2.46

Another area where mutuals have a strong presence is the insurance

industry. Hirmaa appeared before the committee representing 18 health

insurance organisations. These organisations collectively provide insurance to

around one million people, and comprise a variety of the business structures,

with mutuals or member-owned insurers being the most prevalent.

2.47

Superannuation is also a field where the mutual structure is heavily

favoured. Industry Super appeared before the committee and set out the scale

of their operations. From relatively small beginnings where the industry funds

had 200 000 members and managed $2.5 million in assets, they now have a

membership of nearly five million and hold assets of around 376 billion.[37]

Current state and federal legislation governing co-operatives and mutuals

2.48

The development of the Co-operatives National Law (CNL) began in 2012

through the Council of Australian Governments (COAG). The intention was that

each state and territory would pass uniform legislation or legislation

consistent with the CNL by May 2014.[38]

2.49

New South Wales are the lead jurisdiction for the legislation which is

intended to reduce red tape and subsequent business costs involved in

registering and governing a co-operative across jurisdictions. To date NSW,

Victoria, Tasmania, South Australia and the Northern Territory have adopted the

legislation.[39],[40]

WA has amended its Co-operatives Act 2009 (WA Act) to align with the

CNL.

2.50

Nevertheless, some inconsistencies

remain. While Queensland has withdrawn from the agreement altogether, there are

indications that it may yet amend its existing legislation to be consistent

with the national law. ACT is planning the introduction of its enabling laws in

2017.[41]

2.51

There are four elements to the legislation, the enabling Act, the

Co-operatives National Law, the Co-operatives National Regulations and the

local regulations. All jurisdictions that adopt the law will have these

elements.

2.52

The NSW government provided information to the committee explaining the objects

of the CNL, and the expected outcomes. One of the overriding objectives is to

'ensure that there are no competitive advantages or disadvantages for

co-operatives as compared to corporations'.[42]

The main reforms to achieve this are:

-

Improved consistency of co-operatives legislation through the

introduction of uniform template

laws with the option to use alternative consistent legislation;

-

Cross border business

reform, with automatic

authorisation arrangements replacing the requirement for a co-operative to register in each State or Territory

in which it wants to do business;

-

Simplification of financial reporting and audit requirements for

small co-operatives;

-

More flexible options to raise funds from members or external sources through the introduction of co-operative capital

units (CCUs) in all jurisdictions;

-

Responsibilities and duties of directors

and officers of a co-operative updated and made consistent with the Corporations Act 2001 (Cth) (the Act);

-

Improved consistency and referencing of the Act where it can be appropriately applied to co-operatives, such as certain administration and winding up matters;

-

Setting out the responsibilities of the secretary of a

co-operative and the consequences of not meeting those responsibilities;

-

Removing the requirement for a formation

disclosure statement for a proposed

nondistributing co-operative, unless requested

to provide this statement by the regulator;

-

The naming of the types of co-operatives was changed from 'trading' and 'non trading' co-operative to 'distributing' and 'non-distributing' co-operative to better reflect

the nature of the co-operative;

-

Former members' rights have been reduced from 5 years to 2 years duration

in line with stakeholder feedback. Schedule 3 (1) of the CNL provides

for a savings provision in the CNL Adoption Act of a jurisdiction, to maintain the existing former members' rights under their

Co-operatives Act before the commencement of the CNL;

-

Capacity for enforceable undertakings between a person and the regulator

has been introduced to enable a cost effective means of ensuring

compliance by co-operatives with the law;

-

In NSW, about half the fees in its CNL Local Regulations have been reduced,

when compared with the

corresponding fee under the previous

NSW Co-operatives Regulation 2005;

-

Introduction of a fee for the lodging of annual returns or annual reports by a co operative, to help to recoup the costs of the NSW Registry

Services in reviewing these documents for compliance with the CNL. [43]

2.53

To support transition to the new regulatory environment the states and

territories that have enacted the CNL have put

in place administrative arrangements to provide information and assistance to

those seeking to establish a co-operative, or for established organisations.

2.54

Consumer Affairs and Fair Trading in Tasmania for example has published

a number of fact sheets on the CNL as well as documentation on the new fees and

registration processes.[44]

While Consumer and Business Affairs in South Australia has a new section on its

website which includes administrative and governance arrangements as well as

information and advice on how to run a co-operative.[45]

Chapter 3 includes further discussion of the adequacy of information and advice

from state and federal agencies, as well as commentary on the CNL.

Navigation: Previous Page | Contents | Next Page