The Prostheses List in Practice

Introduction

2.1

The Prostheses List Framework has been subject to a number of reviews

since its introduction in 1985. Successive reviews have consistently raised

similar issues suggesting that there are a number of challenges to reform. However,

while the inquiry has shown that there is general support for reform, there is

little agreement on the areas which require reform and how this should be

achieved.

2.2

The absence of agreement may be a symptom of both a segregated system where

stakeholders have limited interaction with each other and a system which lacks

transparency.

2.3

This chapter provides an outline of previous attempts at reform in this

area, the roles and relationships of each stakeholder and the impact of the

Prostheses List (PL) on stakeholders, private health insurance premiums and

consumers.

History of reform

Introduction of the Prostheses List

2.4

The PL was introduced in 1985 with a view to reduce hospital waiting

list for procedures involving surgically implanted prostheses. The government

passed legislation to require private health insurers to pay a benefit equal to

the amount determined by the Minister, or the price of the prosthesis if it was

less than the amount determined by the Minister.[1]

Deregulation

2.5

In 1999 PL benefit amounts were deregulated in response to concerns raised

by the private health insurance industry about the rate of increase of

benefits.[2]

2.6

However, under the period of deregulation, private health insurers

negotiated the benefit amount directly with device manufacturers on the

condition that there would be no gap payment for patients. This condition

undermined the private health insurers' ability to negotiate benefit amounts

and prostheses benefits almost doubled between 2000-01 and 2002-3.[3]

Reregulation

2.7

The Government announced new arrangements in April 2003 in response to

concerns about the rapid increase in prostheses benefits during deregulation.[4]

The new arrangements were developed in consultation with private health

insurers, private hospitals, clinicians, sponsors of prostheses devices and

consumers.[5]

2.8

The new arrangements came in to effect on 31 October 2005 and ensured

that independent clinical advice was integral to determining the clinical

effectiveness of a device. The department advised the process for determining

the benefit levels:

Prostheses for use in hip and knee replacement surgery,

intraocular lenses and cardiac defibrillators, pacemakers and stents were

clinically assessed and their benefit amounts negotiated with their respective

sponsors.

Benefits for the remaining prostheses were determined by

applying the weighted average benefit calculated using benefit levels and

utilisation data on individual prostheses from each insurer that had an

agreement in place with the sponsor as at 31 October 2004.[6]

2.9

Under the new arrangements, benefit levels for new prostheses were

negotiated by the Prostheses and Devices Negotiating Group, acting on behalf of

the Prostheses and Devices Committee (precursor to the Prostheses List Advisory

Committee (PLAC)), who undertook commercial-in-confidence negotiations directly

with medical device sponsors.[7]

Doyle Review

2.10

In accordance with section 12 of the National Health Amendment

(Prostheses) Act 2005, The Honourable Robert Doyle undertook an independent

review of the prostheses arrangements in October 2007 entitled the Review of

the Prostheses Listing Arrangements (Doyle Review).[8]

2.11

The Doyle Review made 15 recommendations for structural, operational and

administrative changes. However, few of these recommendations were adopted and most

were deferred until completion of the Review of Health Technology Assessment

in Australia (HTA Review).[9]

Review of Health Technology Assessment

2.12

The HTA Review was released two years later in 2009 and highlighted that

the process to establish consistent groupings of prostheses with similar

clinical effectiveness had been slow.[10]

2.13

The HTA review recommended that the process to establish consistent

groupings be completed by a dedicated resource within the Department of Health

(department) and that negotiations of benefits for individual prostheses should

cease and that a single benefit level should be established for all prostheses

in each particular group.[11]

2.14

This lead to a decision that in order to expedite the grouping process,

a 25 per cent utilisation benchmark would be used to determine the

minimum benefit amount for prostheses in each group.[12]

The committee heard that this process entrenched benefit levels which had been

negotiated in the preceding years when prices were high and negotiations lacked

transparency.[13]

2.15

Submitters raised concerns during the inquiry that the 25 per cent

utilisation rule was anti-competitive and did not provide an incentive for

device sponsors to lower their prices.[14]

The department explained that the PLAC has moved away from that rule and is

looking to at better ways to arrive at pricing, but clarified that prostheses

are still added to groups on the PL which were subject to the 25 per cent

utilisation rule.[15]

Industry Working Group on Private

Health Insurance Prostheses Reform

2.16

The Industry Working Group on Private Health Insurance Prostheses Reform

(IWG) is the most recent body to consider reform of the PL. The IWG operated

between January and March 2016 and was established to examine opportunities for

reform of the arrangements governing prostheses and pricing in the private

health insurance sector.[16]

2.17

The IWG's report was the impetus for the Government's decision in October

2016 to reduce the minimum benefit amount for cardiac devices and intraocular

lenses by 10 per cent, and reduce hip and knee replacement joints by 7.5 per

cent. These reforms came into effect on 20 February 2017.[17]

2.18

At the same time the Government also announced the reconstituted PLAC,

investigating a more robust and transparent price disclosure model and considering

a transparent way to reimburse hospitals for the costs of maintaining inventory

of medical devices.[18]

The IWG's final report and its recommendations will be discussed further in

Chapter 3.

Effect of the Prostheses List Framework

2.19

The PL has been described as being left on 'set and forget mode' with

almost half of all items on the list priced at the same benefit level in 2016

as they were in 2011.[19]

2.20

In any other market this would indicate that prices have not risen with

inflation and were therefore below what they should be. In fact prostheses

prices have not risen in real terms in the past seven years.[20]

However, some submitters argued that prices were initially set artificially

high and this cost is being passed on to consumers.[21]

2.21

An area of key concern is that '[t]he high price of prostheses impacts

on health insurance premiums, and therefore contributes to concerns about the

affordability of private health insurance.'[22]

Private health insurance premiums

2.22

Private Healthcare Australia (PHA) submitted that price sensitivity

modelling indicates that private health insurance premiums will become

unaffordable for at least one-fifth of current customers in five to six years.[23]

2.23

Already private health insurers are reporting that their members are

decreasing their level of cover in an effort to reduce the premium paid.[24]

New private health insurance customers are also choosing to take out less

comprehensive policies with a higher excess amount in order to pay a lower

premium. For example, HBF noted that '[i]n 2010, 32% of people taking out

hospital cover with HBF chose "top hospital" or the equivalent but by

2016 this had fallen to just 13%.'[25]

In 2013-14, 69 per cent of HBF hospital cover policies had zero excess but

this declined to 54 per cent in 2015-16.

2.24

The committee heard that in the quarter ending September 2016, 14 per

cent of private health insurers' hospital cover reimbursements were for

prostheses. Medical benefits consisted of 16 per cent, whereas private hospital

costs such as accommodation, theatre fees and nursing care accounted for 70 per

cent of total reimbursements paid.[26]

The Medical Technology Association of Australia (MTAA) therefore considered

that a review of private hospital costs was more likely to result in

substantial savings, rather than reforming or decreasing the minimum benefit

amounts of the PL.[27]

2.25

Device manufacturers also noted that private health insurance premiums

have increased by 40 per cent in the past seven years in contrast to PL

benefits which have not increased in real terms over the same period.[28]

Mr Fox-Smith of Johnson & Johnson Medical Devices ANZ pointed to an

increase in utilisation of private health care in Australia as contributing to

an increase in costs for private health insurers rather than the price of

prostheses.

2.26

This view was supported by information provided by HBF. In their

submission, HBF stated that in 2014 an average of 3.3 prostheses were used per

procedure and that this number has increased to 3.6 prostheses per procedure in

2016. HBF attributed the increase in utilisation to changing technique,

industry behaviour and the addition of new devices to the PL.[29]

2.27

Medibank Private also noted that since 2011 the number of hospital

admissions per customer has increased by 19 per cent and the average amount

paid by Medibank Private per admission has increased 10 per cent.[30]

2.28

It is estimated that the PL reforms announced in October 2016 will

reduce costs for private health insurers by $86 million in the first year.[31]

Medibank Private advised that this would result in a reduction of between

$22 million and $24 million for their company and a 0.35 per cent

reduction in fees for their customers.[32]

Both Medibank Private and Bupa, Australia's largest private health insurers,

have provided assurances that any savings will be directly passed on to

customers through lower premiums.[33]

2.29

While hospital admissions and utilisation of prostheses has increased in

recent years, the evidence heard by the committee does suggest there is a

direct relationship between PL minimum benefit amounts and private health

insurance premiums.

Price differences

2.30

A number of submitters described the price of prostheses in the private

hospital system as 'inflated' or 'high', particularly in comparison to the

prices paid by public hospitals for the same device.[34]

2.31

This view is supported by a 2009 Productivity Commission report on the

performance of public and private hospital systems which suggested that 'the

cost of prostheses in public hospitals is considerably lower than in private

hospitals.'[35]

2.32

The Independent Hospital Pricing Authority (IHPA), an independent agency

established under the National Health Reform Act 2011 to contribute to

reforms to Australian public hospitals, provided data to the committee on the

number of episodes and cost of prostheses for intraocular lenses, cardiac, hip,

knee and spinal prostheses. The tables below provide data for public hospitals

in 2014-15 and for private hospitals in 2013-14. The IHPA urges caution in

comparing the data given it was collected for different years, and was

collected using different standards and different collection methods.

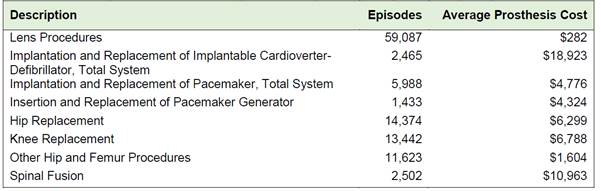

Table 2.1: Number of episodes and

cost of prostheses provided to public hospital patients in 2014-15

Source: Independent

Hospital Pricing Authority, Submission 37, [p. 2.]

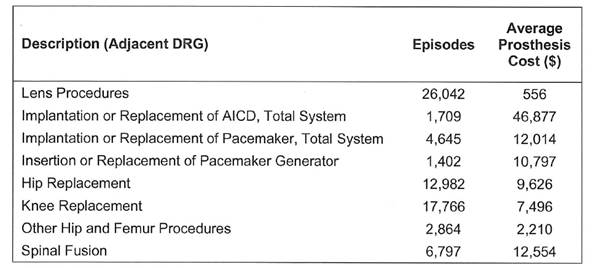

Table 2.2: Number of episodes and

cost of prostheses in private hospitals 2013-14

Source: Independent Hospital

Pricing Authority, answers to questions on notice, 15 March 2017, (received 3

April 2017).

2.33

In its submission, Bupa cited the following examples which demonstrated

the price difference between private and public hospitals:

-

a standard branded ceramic hip is

purchased by the Prince of Wales Public Hospital in Sydney for $4,900 while a

private patient in the hospital next door pays $11,000;

-

an uncemented Zimmer Trilogy cup

cost Western Australia Health $1939, which is just under $1000 less than the

listed benefit on the Australian Prostheses List of $2,900;

-

an implantable cardiac

defibrillator cost Western Australia Health $19,000 while the current listed

benefit on the Prostheses List is $52,000 - $33,000 more expensive.[36]

2.34

Medibank Private also provided examples of prostheses which it had

funded at the PL minimum benefit amount and the price paid for the same device

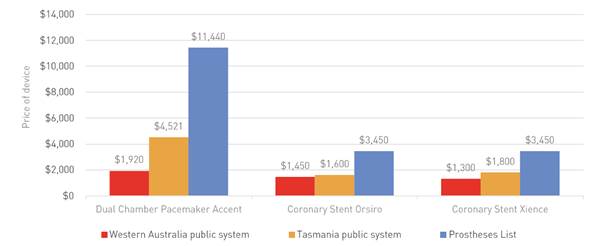

in the Western Australian and Tasmanian public health systems. Figure 2.1 below

demonstrates the price difference paid.

Figure 2.1: Examples of differences

in pricing between the Prostheses List Minimum Benefit amount and public sector

pricing

Source: Medibank Private, Submission 14, p. 5.

2.35

Medibank Private submitted that in the 2015 calendar year it had funded

the Dual Chamber Pacemaker Accent 328 times and paid up to $3.12 million more

for the same device compared to a Western Australian public hospital.

2.36

Price information released by WA Health for cardiac, ophthalmic and

orthopaedic prostheses showed that on average, public hospitals in Western

Australia pay approximately 45% less than the price set by the PL.[37]

This is consistent with the Doyle Review which found that 'some sponsors were

willing to provide prostheses to public hospitals at 30 to 40 per cent less

than the PL minimum benefit.'[38]

2.37

Similarly, submitters noted that Australian private patients pay significantly

more for the same device compared to international markets. For example:

-

A Consulta CRT-P model C3TR01 triple-chamber pacemaker costs €4000 in France (approximately $5

840 AUD) compared to $13 520 on the PL.[39]

-

A St Jude

Medical pacemaker costs £16 448 (approximately $27 000 AUD) in the United

Kingdom compared to $52 000 on the PL.[40]

2.38

Private health insurance companies submitted that these price

differences are contributing to the rising cost of private health insurance

premiums.[41]

However, the MTAA who represents prostheses manufacturers disagrees with this

view and noted that since December 2009 medical device inflation has increased

by only 2.3 per cent, compared to medical and hospital services which have

increased by 55.1 per cent in the same period.[42]

Committee view

2.39

The committee recognises that in many instances the minimum benefit

amount of a prosthesis listed on the PL and paid by private health insurers is

significantly greater than the price paid by public hospitals for the same

device and internationally.

2.40

The committee notes that the cost of prostheses is one aspect which

influences the cost of private health insurance premiums, however, utilisations

rates are also a factor. The committee is concerned that the rising cost of

private health insurance premiums may make health insurance unaffordable in the

future and therefore place greater pressure on the public health system.

2.41

The committee notes there is a wide range of views on the reasons for

the price difference between public and private patients and overseas markets

and that there is little consensus between stakeholders as to how this may be

addressed. This will be explored further in Chapter 4.

Relationships between stakeholders

2.42

The framework within which benefits for prostheses paid for through

private health insurance are set is complex, opaque and involves multiple

stakeholders. Privately insured patients in public or private hospital settings

are provided with prostheses that are:

-

chosen by their surgeon or other relevant specialist;

-

purchased by the hospital in which they are being treated; and

-

paid for by a private health insurer at benefit levels

recommended by a committee appointed by the Minister for Health.

2.43

The majority of benefit levels were set some years ago in an opaque process

when prostheses prices had inflated substantially over a short period of time

and seem, at least in some cases, to have been set at levels far in excess of

what is paid in the public sector domestically or in comparable countries

internationally.

2.44

At the heart of this inquiry are the consumers, affected by rising

private health insurance premiums, and taxpayers, who subsidise a significant

proportion of private health insurance premium payments.

2.45

The committee heard that the relationships between stakeholders with a

vested interest in the PL are not transparent and siloed which means each

stakeholder has a limited understanding of the practices of other stakeholders

and their relationships with each other. Figure 2.2 below outlines the

interaction of stakeholders in the operation of the PL.

Figure 2.2: Prostheses value chain

Source: Private Healthcare

Australia, Submission 7, [p. 15].

Private hospitals and doctors

2.46

The MTAA submitted that the PL enables patients in private hospitals to

access a greater range of prostheses and more complex technologies than public

patients as a patient's surgeon is able to choose the prostheses which best

meets their patient's circumstances.[43]

2.47

A surgeon simply advises the hospital of the prostheses required and the

private hospital will acquire the prosthesis requested.[44]

While some submitters raised concerns that this freedom of choice may lead to perceived

conflicts of interest, the Australian Orthopaedic Association (AOA) told the

committee that they recommend any surgeon 'involved in the manufacture,

promotion or study of a device or is on a recommendation board'[45]

disclose this information to their patient if they are using that prosthesis.

2.48

The AOA Code of Conduct also states that members 'must declare any

conflicts of interest, in particular, financial relationships with prosthetic

companies or hospitals and other corporate entities or persons.'[46]

However, as there is limited development of prostheses in Australia it is

unlikely for a need for disclosure to arise.[47]

2.49

It is also important to note that surgeons do not work for the hospital

in the same sense that doctors in the public sector work for a public hospital.

Manufacturers and private hospitals

2.50

The committee repeatedly heard that information around the price of

prostheses paid by private hospitals to manufacturers was not available due to the

commercial-in-confidence nature of the contracts between private hospitals and

manufacturers regarding the purchasing of prostheses and other medical devices.[48]

2.51

A representative of Catholic Health Australia told the committee that '[t]he

commercial arrangements between vendors and hospitals are complex, opaque and

vary in their structure.'[49]

2.52

A further issue is the value of rebates which private hospitals receive

for purchasing a number of medical devices from one manufacturer. An

orthopaedic surgeon told the committee that at the hospital they performed

procedures in, these rebates were referred to as Stryker dollars, Zimmer

dollars and J&J dollars, and that these could be used to purchase other

consumable products from the manufacturers.[50]

2.53

The Australian Private Hospital Association explained how the rebates

operate:

Those who are a bit larger and in a stronger negotiating

position have arrangements, I am advised, that are typically on two bases.

There is a volume basis. So, if you hit a particular target for a

whole-of-business spend, for example, you spend X million dollars or X hundred

million dollars a year—and that is not necessarily just on prostheses but also

on consumables, theatre equipment or whatever that particular company

supplies—then a rebate regime will kick in.[51]

2.54

This practice nets Ramsay Health Care, Australia's largest private

hospital company, rebates of between five and seven per cent of the $700

million Ramsay spent on 650 000 individual prostheses last financial year,

equating to between $35 million and $40 million.[52]

2.55

PHA described the practice as 'price shielding' and suggested that the

practice provides an incentive to choose devices on the PL with a higher

minimum benefit amount to maximise the level of rebate paid, as private health

insurers are required to pay the minimum benefit amount, regardless of the

amount paid by the hospital for the device.[53]

2.56

Some submitters argued that one third of the price difference between

prostheses in public and private hospitals goes to the private hospital and the

remaining two thirds to the manufacturers of prostheses.[54]

However the opaque and confidential nature of the contracts which contain these

rebates means it is difficult to quantify this amount.

Private hospitals and private

health insurers

2.57

Private health insurers are required to pay the minimum benefit amount

listed on the PL for a prosthesis received by one of their customers.

2.58

Dr Andrew Wilson of Medibank Private described private health insurers

as merely bill payers who have no visibility of the relationship between

private hospitals and manufacturers.[55]

2.59

As outlined above, there is no transparency regarding the price actually

paid by the private hospitals for a particular prosthesis compared to the

amount paid by the private health insurer, as required by the PL.

2.60

Last financial year Medibank Private (including AHM) spent $540 million

on prostheses devices as part of the total $5.1 billion spent on healthcare.[56]

Excluding AHM, Medibank alone spent $485 million on prostheses in the 2015-16

financial year. This is in addition to $904 million for hospital benefits and

$204 million on medical benefits associated with the cost of prostheses.[57]

Private health insurers and consumers

2.61

An advantage of the PL for consumers is that it offers certainty for

consumers that any prostheses which they receive from the PL will be covered in

full by their private health insurer.[58]

However, private health insurers then pass the cost of prostheses onto their customers

through the price of health insurance premiums. PHA estimated that this adds

$150 per year to each private health insurance premium.[59]

2.62

Consumers are required to place a significant amount of trust in the

information provided to them by their surgeon. The committee heard that

consumers are often unaware of the costs or rebates associated with the device

chosen for them by their surgeon.[60]

2.63

Applied Medical observed that consumers are the only advocates for lower

prices in the current system. Only one of the twenty-one members of the PLAC

represents consumers.[61]

Consumers are at a further disadvantage as they are under resourced and are not

commercial entities so do not have the required knowledge or influence to

negotiate within a complex system.[62]

The role of government

2.64

The government is both the regulator of the PL as well as a

purchaser/funder of medical devices in the public and private sectors. The

government regulates private health insurance through a range of legislative

instruments, including the Private Health Insurance Act 2007 and, of

particular interest to this inquiry, through the Private Health Insurance

(Prostheses List) Rules.[63]

2.65

The government is also a significant purchaser or funder of medical

devices through its support for veterans, administered by the Department of

Veterans' Affairs (DVA). In 2015-16 DVA provided access to a range of health

services for approximately 200 000 veterans, war widows and dependants.

Expenditure for hospital services over this period was $1.6 billion, with $853

million in the private sector and $743 million in the public sector.[64]

2.66

DVA private hospital contracts use the PL as the basis for funding

medical devices for veterans. The table below shows DVA's expenditure on

medical devices in private hospitals over five years to 2015-16.[65]

Table 2.3: DVA expenditure on

medical devices in private hospitals

| |

2011-12 |

2012-13 |

2013-14 |

2014-15 |

2015-16 |

| Expenditure |

$110 473 079 |

$105 748 801 |

$107 026 717 |

$103 962 144 |

$101 284 452 |

| Items |

116 580 |

111 352 |

110 274 |

103 276 |

101 769 |

| Average cost |

$948 |

$950 |

$971 |

$1007 |

$995 |

Source: Department of

Veterans' Affairs, Submission 20, p. 3.

2.67

DVA estimated that its public hospital expenditure for medical devices

was $9.6 million in 2015-16. DVA stated the difference in funding between the

two sectors can be attributed to a number of things, including 'the expected

economies of scale that can be realised by the public hospital system through

purchasing arrangements.'[66]

2.68

While the government regulates the PL, the Australian Medical

Association (AMA) submitted that 'the current construct of the reimbursement

system is currently swayed towards industry, ultimately at the expense of

consumers and the Government.'[67]

2.69

The department is similarly segregated from other stakeholders stating

that 'there are financial transactions going on between private hospitals,

prosthesis makers and private health insurers which are, at some level, opaque

to the public and the department.'[68]

This is a concern as the government is a key stakeholder, as the regulator of

the PL, yet does not have full visibility of the system and how it operates in

practice.

2.70

The complex nature of stakeholder relationships and the operation of the

PL was reinforced by the department who noted that 'no-one has a complete

understanding, and no-one has a complete dataset.'[69]

Committee view

2.71

The committee notes that through the operation of the PL, the relationships

between stakeholders are complex and not transparent and has resulted in some stakeholders

having limited interaction with each other.

2.72

The committee believes that the complex relationships and competing

interest of stakeholders has made past reform challenging. The committee is

concerned that the lack of transparency has reinforced the operation of the

existing PL Framework and contributed to the slow rate of reform.

2.73

The committee notes the role of the government as a significant

funder/purchaser of medical devices on the PL and considers that government

could achieve significantly cheaper prices if it purchased devices directly.

Issues identified by submitters

2.74

Submitters raised a number of issues during the inquiry which have been

the identified by previous reviews of the PL and the subject of past attempts

at reform. These issues are outlined below and will be further discussed in

Chapter 4.

Lack of transparency

2.75

In addition to concerns around the transparency of relationships between

stakeholders as discussed above, the committee heard that many aspects of the PL

lack transparency including the benefit setting process.

2.76

Mr Glenn Cross of AusBiotech Ltd noted that the '[c]urrent benefit

setting processes are opaque.'[70]

This view has been consistently expressed throughout reform of the PL. For

example, hirmaa submitted that in 2005 when the PL was reregulated, '[t]he

underlying basis upon which benefit amounts were negotiated and determined is unknown.'[71]

2.77

Concerns were also raised by the AMA that the scope and methods which

PLAC used to set prostheses benefits was unclear. The AMA pointed out that

'under "commercial in confidence" protection, the PLAC does not have

access to all commercial and industry data to make an assessment on appropriate

prostheses pricing.'[72]

2.78

The department suggested that further reform was necessary to achieve

transparency commenting that 'in order to get greater transparency, we need to

change arrangements.'[73]

Reducing duplication and redundancies

2.79

Submitters also identified areas of the PL Framework which should be

reformed with a view to reducing duplication of processes between the PLAC and

the TGA, for the PLAC to operate more efficiently and reduce the number of

items included on the PL.

2.80

Ausbiotech observed that '[a] big opportunity for cost-saving is in

reducing red tape and redundancy across the application and evaluation process

of the prosthesis list.'[74]

The MTAA shared this view and suggested that devices

already approved by the TGA could be added to an existing group on the PL

without review by the PLAC in order to improve the efficiency of the Health

Technology Assessment process.[75]

2.81

However, the benefits of the clinical advisory groups in providing

advice on safety and effectiveness were affirmed through, for example,

detection of safety concerns in relation to the 'VAIOS' prosthesis.[76]

2.82

Bupa identified that reviewing the number of items on the PL and

removing those which are not clinically effective or are rarely used would

enhance the operation of the PLAC. Since 2008, 2,746 items from the current PL have

never been used, accounting for 26 per cent of items on the list.[77]

2.83

Minimising duplication and improving the listing process forms part of

the PLAC's work program following the final report of the IWG.[78]

The PLAC's work plan also includes undertaking a number of targeted category

and benefit reviews such as low cost high volume items which could be

rationalised.[79]

International price benchmarking

2.84

As discussed earlier in this chapter, private health insurers identified

a significant difference between the price paid by Australian consumers compared

to international markets. A number of submitters suggested that reform to the PL

should include international price benchmarking.[80]

However, a number of device manufacturers cautioned against this approach:

...we find that comparing prices in Australia's private and

public healthcare systems or benchmarking to international healthcare systems

is an incredibly simplistic notion—one which demonstrates no understanding of

the reality or the complexity of the environment or why it is unworkable to

directly compare without taking into consideration other factors.[81]

2.85

Medtronic agreed that an effective international price benchmarking

system would be difficult to establish stating that:

An international referencing system would be extremely

complex and fail to consider the varying factors impacting supply and purchase

of medical devices in the Australian healthcare system:

-

It does not take into account

differences in healthcare market structures, local costs of doing business,

market size, economies of scale, service provision and delivery models,

currency volatility;

-

Many types of products – not just

medical devices – exhibit a range of price variation for a range of reasons

both within and between countries for the same product; and,

-

To our knowledge, no other

Government price disclosure process, including for the PBS, uses international

referencing.[82]

Potential savings

2.86

PHA reported that a 45 per cent decrease in the private prostheses

expenditure would amount to approximately $800 million in savings.[83]

However, this figure is disputed by a number of stakeholders on the grounds

that it was based on flawed methodology and data.[84]

2.87

For example, the MTAA argued that the calculation was made on a very

small sample of only 41 of the approximately 10 400 devices of the PL. These

devices were also from a narrow range of categories on the PL and were devices

that were more likely to included additional services and ancillary support.[85]

2.88

The department was also unable to verify the accuracy of the $800

million savings figure .[86]

Committee view

2.89

The committee acknowledges the concerns of stakeholders regarding the

veracity of the $800 million in potential savings from reforming the PL.

However, the committee believes that there is significant scope for reform and

savings in this area.

2.90

The committee notes that stakeholders identified a number areas in the PL

Framework which would benefit from reform. The committee considers the lack of

transparency in the PL framework to be a barrier to further reform and

consideration of alternative models such as price benchmarking an reducing

redundancies.

Navigation: Previous Page | Contents | Next Page