Communicating with Centrelink

I sat with my daughter—and I have worked for the public

sector for many years—and attempted to go through the questions which were in

this form with her. Some of the questions were nonsensical. I had no idea what was

being asked. You cannot progress unless you answer the question, so people are

making a guess. They are putting in whatever information in order to get the

form completed. They do not understand.[1]

Power imbalance

3.1

Throughout this inquiry, the committee heard wide-ranging evidence

regarding the difficulty individuals and organisations faced in communicating

with the Department of Human Services (department) to discuss online compliance

intervention (OCI) related debt matters. Communication problems included

letters not being received, trouble contacting the department via phone, difficulty

in receiving intelligible income data used to calculate purported debts, hard

to navigate online communication portals, difficult to understand

correspondence and a lack of material translated into other languages. These

were all listed as individual barriers to effective communication between the

public and the department.

3.2

However, a number of organisations raised a separate critical issue that

acts as a barrier to all forms of communication – that there is a significant

power imbalance between income payment recipients and the department, and

communication therefore does not take place on a level playing field.

When confronted with a large public entity like Centrelink, many

people feel that they simply must comply with the requests and that they have a

limited capacity to advocate for themselves and limited confidence in the

system's willingness to interact with them. I think this has been exacerbated

by the loss of human oversight of these processes.[2]

3.3

In discussing the impacts of this power imbalance, where individuals

tend to assume 'the department is right', organisations pointed to a number of

adverse outcomes for individuals, such as people paying purported debt notices

without question and people accepting pre-filled income data that averages

their income without checking it for accuracy, leading to incorrect debt

calculations. The evidence presented to the inquiry points to a tendency among

individuals to assume the department is correct, and when a person does see an

error, they feel they do not have the power to change it.

A lot of people get one of the letters and assume that the

debt is correct, so they go into an agency and say: 'I've got this Centrelink

debt and I can't afford it. What can I do?' That is when the agency says:

'Maybe you better actually check to see whether the debt's correct. Go to the

Welfare Rights Centre.'[3]

3.4

The Australian Council of Social Service (ACOSS) cited communication at

the commencement of the program as having created a climate of fear among debt

letter recipients:

We also know that, because of the communications from the

responsible minister in the lead-up to this program being unleashed, there has

been a perception created that if you do not comply you may go to jail.[4]

3.5

The Queensland Council of Social Service put forward the view that in

order to achieve procedural fairness in the OCI process, government is

responsible for ensuring that communication is clear and effective:

The government has a responsibility to provide clear and

comprehensive information to individuals affected. The government has a

responsibility to ensure that there is sufficient support for clients affected.

The government has a responsibility to provide a number of channels of support:

digital, phone or face-to-face. The government also has a responsibility to

provide a myGov website that is easy to access and navigate.[5]

3.6

As discussed in Chapter 2, evidence from multiple submitters also points

to the shift in the onus of communicating. Where the department previously checked

income discrepancies, by communicating directly with employers, under the new

OCI system, the onus for seeking that information and communicating it to the

department in a highly proscribed form is now the responsibility of the income

payment recipient:

In the past, DHS would investigate these discrepancies and

would seek to obtain sufficient information from the person or employer to

enable an accurate assessment to be made. Under the new

process, DHS does not seek to obtain sufficient information to enable an

accurate debt assessment to be made. It is instead used as the online platform,

which is an automated system that makes a debt assessment based on the data

match information alone if the person does not provide further information for

any reason.[6]

3.7

The outcome of this communication with the department is critical for

individuals – if they get it wrong they could incur a debt they do not owe. This

chapter will review the various challenges people find in communicating with

Centrelink, and the impact that challenges have specifically on their purported

debt matters and more broadly on their lives.

Initial letters

3.8

Chapter 2 provided a breakdown of the OCI process, whereby the first stage

is the data-matching process itself, and where a possible reported income

discrepancy is found, an initial letter is sent to the individual asking for

clarification around that income discrepancy.

3.9

The department provided evidence around this first stage of communicating

with people who may have an income discrepancy. Firstly, the department

explained that initial contact was not a 'debt notice.'[7]

Instead, the department referred to this step as a 'request for clarification':

We match data with the tax office to see if there is a

difference between the information the ATO has about employment and the

information the recipient has told us. If there is a difference, we do not make

an assumption about whether that is a debt or there is no debt; we simply ask

the person to clarify the difference and provide either confirming information

or updated information.[8]

3.10

However, the National Social Security Rights Network expressed concern

that, as individuals tend to assume the department is correct, the wording of

the letter itself could lead individuals to not provide detailed and accurate

information:

The very first version of the letter said, 'Go online to

confirm your ATO information.' 'Confirm' is an extremely confusing word to use

because generally the ATO information is correct... A number of people simply

went online and all they did was confirm it and then averaging resulted or they

did not go online because, understandably, they said, 'It's correct. I probably

don't need to worry about this.'[9]

3.11

People with Disability Australia were also critical of the confusing

nature of the initiating letters from the department, stating that 'We raised

concerns with the Ombudsman early on that the initial letter sent to welfare

recipients failed to include crucial information and provided information that

confused and frustrated some of the people who contacted us.'[10]

3.12

One individual who received a letter, Michael, pointed out that the

subject line of the letter itself does not encourage people to open the

communication, because the letter 'is marked "general" in the inbox.

It is not labelled "urgent", "please respond", or "information

needed". It is labelled "general". I think that seems foolish.'[11]

3.13

The Welfare Rights Centre, South Australia pointed to the difficulties

individuals had in responding to the letters because the person may 'lack the

internet literacy to adequately respond to the letters and some letters are

never received as the customer has moved.'[12]

These two issues are discussed in detail below.

3.14

The Council on the Ageing Tasmania pointed out that beyond internet

literacy, general literacy levels are also a barrier to some people responding.[13]

General and internet literacy is discussed in greater detail in the later

section on communication barriers.

Incorrect addresses

3.15

The inquiry received evidence from a range of organisations relating to

the apparent lack of updated contact details held by Centrelink, which resulted

in many individuals not receiving the initial 'clarification' letters.[14]

ACOSS estimated that this resulted in over 6 500 people hearing about their purported

debt from a debt collector rather than from Centrelink.[15]

3.16

The department discussed this problem at the second Canberra hearing,

and outlined changes it made to the distribution of postal letters. The

department initially used the 'last known address' to post letters. Around 5

000 people did not receive initial letters as the 'last known address' was not

up to date.[16]

The department said it now sends letters via registered post and that, after an

initial settling in period, 'the registered post system is more mature and we

are able to reach that 10 000 mark' of letters being delivered each week.[17]

The department also acknowledged that in some cases, lack of up to date details

meant that letters were sent to deceased people.[18]

3.17

ACOSS provided evidence that while the use of registered mail will

resolve the issue of whether initial contact can be verified, '[t]hat does not

address the matter of people who have previously been contacted under this

program, who have not received that information, and are currently trying to

address an alleged debt.'[19]

3.18

The issue of people who first heard about a purported debt from a debt

collection agency instead of the department is discussed in further detail in

this chapter below. The process by which people challenge the estimated debt

amounts is discussed in chapter 4.

People 'not engaged'

3.19

The department discussed the difficulty they face, across many different

payment areas, in having people engage with the department's requests for

information. The department provided evidence that in one payment area, over 20

per cent of people did not respond to requests for information:

Last year we sent out about 300,000 [reminders] and, even

after we had sent reminders, still [65,000] people received a debt because they

had not updated their details, they had not engaged with us. Of those 65,000

people who had a debt, about 21,000 subsequently had the debt reduced to

zero—because they had done everything; they just had not told us. This is a

pattern that we have. We actually have to suspend a number of payments every

year from recipients who we ask for information—we ask them to update their

details; we ask them to notify us of earnings—and they do not give it to us.

After we have tried on a number of occasions, we actually have to suspend their

payments in order for them to engage with us again. So I think it is going to

be a key lesson learnt for us about just how many people are not responding to

calls for action.[20]

3.20

The department further stated that it had underestimated 'how many

people would not clarify and would not engage'[21]

after receiving the initial letters and claimed that much of the communication difficulties

specific to the OCI program were caused by this lack of engagement by individuals:

I think it is a problem when the recipient or the former

recipient does not engage with us. That is why the refinement has been to

ensure as best as possible that we can engage with the recipient. Sometimes we

will really struggle to engage with either a recipient or a former recipient

because they do not want to be engaged with us, or it may be that for whatever

personal reasons they do not want to engage.[22]

3.21

Witnesses raised a number of reasons as to why many individuals do not

respond to communications from the department.

3.22

ACOSS provided evidence that often, communication with individuals is

not done through a printed letter sent to an individual's residence. Instead, a

person can be contacted via text message or email, letting them know there is a

letter from Centrelink available on their myGov account. ACOSS submitted that

in the case of the OCI, many people ignored such communications, thinking it

was not relevant because 'they no longer have anything to do with Centrelink,

and they thought they had done the right thing. They just thought it was an

administrative error.'[23]

3.23

Other witnesses pointed to many people's long-term reluctance to engage

with Centrelink processes:

[W]e know of many people who have received letters from

Centrelink and never open them. Clients will come in with a bundle of 10

letters from Centrelink that they have never opened. While that could be seen

as being irresponsible, for many people it is a sense of hopelessness or

helplessness in the face of a system that they often do not understand well.[24]

Timing

3.24

The inquiry heard evidence that the timing of the department sending out

initial letters was poorly chosen. The Federation of Ethnic Communities'

Councils of Australia (FECCA) pointed out that during the Christmas period when

many people received initial letters, advocacy services for Culturally and

Linguistically Diverse (CALD) Australians were closed, leaving people to 'deal

with it on their created difficulties for individuals due to the lack of legal

advice available, but also because of the increased stress that vulnerable

individuals and families experience during Christmas. The Financial Counsellors

Association of Western Australian described a typical call for assistance:

'So I've had this letter, but I've got all these other debts.

I'm just about to start my kids at school, I've got to buy uniforms, I've got

to buy books, school fees. I've had a moratorium on my utility, I've got to now

find the money for that, I've got the credit card debt after Christmas, and now

this has come.'[25]

3.25

Mission Australian echoed this evidence of the distress caused by the

timing of letters:

In the lead-up to Christmas Mission Australia in Tasmania

experienced a significant increase—around 20 per cent—in the number of calls

from people who were overwhelmed or traumatised by the amount of debt they owed

to the government and the urgency with which they had to pay that back. The

majority of these callers were not aware of the supports available to them or

how to challenge the claims of debt. The huge amounts of debt and the tight

time frames to respond to them left people anxious and distraught—for example,

some clients received these letters just before Christmas and did not know

whether they could afford food or last-minute gifts. Then, towards February, we

got feedback from some people that they were unable to provide school supplies

and uniforms for their children as they were paying back a debt to Centrelink.[26]

3.26

Ms Campbell, Secretary of the department, claimed that much of the

distress was caused, not by the letters themselves, but by the media attention,

stating 'I think that in the lead-up to Christmas and into January people

became even more distressed because of the significant media attention around

these issues. I think that half of the stories that appeared in the media were

not part of this system—they were general debt matters but, because of some of

the stories in the media, there was a belief that all debts were wrong.'[27]

3.27

The department also provided evidence that seasonal variations are taken

into account, and stated 'there was a significantly lower number of debt

assessments initiated in December, because we are aware that that is a

difficult period.'[28]

However, Ms Campbell, Secretary of the department went on to say:

It is a difficult management system around when you can and

cannot send out letters. If we do not send them out in November, December and

January then we have to send out letters in February, March and April, and then

people say, 'It's Easter.' It is very difficult to find a good time of year to

send a letter to someone asking them to clarify their details.[29]

Committee

view

3.28

The committee notes that for the 6 500 people who did not receive their

initial letters before the department moved to using registered mail, those

people lost the opportunity to 'clarify' income data discrepancies. A

significant proportion of those 6 500 people would have had their purported

debts reduced or acknowledged as incorrect, had they had the opportunity to

provide information to the department.

3.29

The committee remains highly concerned that a proportion of this cohort appears

to have paid these purported debts without question, meaning the department was

likely recouping monies it was not owed, from people who could least afford it.

3.30

The committee notes it is clear there is a significant communication problem

when 65 000 from 300 000 people do not respond to requests from the department

to engage. When the proportion of non-respondents is so high, it is also clear

the communication problem lies not with the recipients, but with the department.

These communication problems were exacerbated under the OCI program, but are

clearly a broader systemic issue.

3.31

There is no doubt that the sending of a significant number of letters in

the period before Christmas caused additional distress to people receiving the

letters.

Communication barriers

3.32

The inquiry heard evidence from a range of organisations and

individuals, that communication barriers experienced by people were not

adequately taken into account by the department in its communication strategy

for the OCI program. These barriers included having a vulnerability indicator,

language barriers, or a communication disability.

Vulnerability flags

3.33

The department uses a system of a 'vulnerability indicator' on a

person's record to indicate a jobseeker who has a 'psychiatric problem or

illness, cognitive or neurological impairment illness or injury requiring

frequent treatment, drug/alcohol dependency, homeless, recent traumatic

relationship breakdown, significant lack of literacy and language skills or a

nationally approved vulnerability.'[30]

3.34

The department submitted that vulnerable people are not subject to the

OCI program, including 'those who are culturally and linguistically diverse, if

the person is in a period of bereavement, affected by a natural disaster or

resides in a geographic location with limited access to digital services. The

identification of vulnerable recipients is based on the information the department

has on record.'[31]

3.35

ACOSS noted that the OCI program would likely include some vulnerable

people who do not yet have a vulnerability flag on their record:

That may happen, for instance, where the person did not have

a vulnerability at the time they received a Centrelink payment from where the

alleged debt arose, but have subsequently acquired one—for instance, they may

be subjected to domestic violence or have depression and anxiety. Those people

may well be caught up by this program.[32]

3.36

The National Social Security Rights Network agreed with this view, and

went further to state that this system may not be appropriately targeted because

'these indicators are applied to job seekers and, as the example below shows,

may not be applied to recipients of non-activity tested payments such as

sickness allowance.'[33]

3.37

FECCA also pointed out that while many individuals have a vulnerability

flag, and would therefore not have received letters, many vulnerable people

would still be subject to the debt-recovery program:

By definition, those receiving support from Centrelink will

likely have vulnerabilities, whether or not they are severe enough to be noted

with a vulnerability indicator in their record. That vulnerability is likely to

be compounded if you are from a CALD background.[34]

3.38

By contrast, Basic Rights Queensland submitted that indicators aside,

most income support payment recipients are vulnerable:

Centrelink does say it has those vulnerability indicators but

then, by definition, most of the people who contact us are quite vulnerable in

one way or another—it is just that it hasn't been officially categorised as

such.[35]

3.39

The Tasmanian Council of Social Service (TasCOSS) agreed with this view,

stating 'any human service system we have in place in this country should

actually already acknowledge the level of need that anyone accessing a safety

net might have, rather than people having to be stereotyped or stigmatised by

having a flag next to their name.'[36]

3.40

TasCOSS put forward the view that the reason for this, is that there are

sensitivity issues around creating those vulnerability indicators in the first

place, which may mean many vulnerable people are not identified as such:

The need for an individual or the desire of an individual to

disclose vulnerability is very personal. Many people have gone through their

whole life very carefully guarding the fact that they may be illiterate, for

example, and they become very clever at how they deal with covering that up.

Equally, someone with a mild intellectual disability will be very proud of the

fact that they fully function within the community within their capacity and do

not want to be classified as a person with a disability, and nor should they. [37]

3.41

TasCOSS also submitted that vulnerabilities often co-exist in areas of

socio-economic disadvantage such as Tasmania, where the impact would be felt

harder than in other regions:

It was always likely that the system would have a

particularly egregious impact in Tasmania. Tasmania has the highest rate in the

nation of children living in low-income, welfare-dependent families (30%), the

highest youth unemployment rate (16.2%), and the highest rate of female

sole-parent pensioners (5.5%). It also has high levels of inadequate adult

literacy (less than 50% of Tasmanian adults have literacy skills at or above

OECD level 3). Tasmanians, like many in rural and remote parts of Australia,

have very limited access to legal assistance services and effectively no access

to pro bono legal services.[38]

3.42

Mental Health

Australia concurred with this view, and stated that 'it should not be a requirement

for Centrelink customers to disclose mental health issues for debt collection

activity to be conducted in a manner that is sensitive to their needs.' Mental

Health Australia pointed to the disbanding of mental health specific

consultative groups within the department as being a contributing factor to the

failure of the department to appropriately institute risk-mitigation processes

to support people with mental health issues.[39]

To rectify this problem, Mental Health Australia recommended:

[T]he Department should employ a co-design methodology to

ensure that debt recovery processes, and Centrelink services more broadly, are

fit-for-purpose and have necessary protocols to protect vulnerable cohorts,

including people experiencing mental health issues. As a mechanism for

co-design, the Department should immediately reconvene the Consumer

Consultative Group, the Service Delivery Advisory Group and the Mental Health

Advisory Working Party as a core element of the Department's continuous

improvement process, which would by supported by user testing.[40]

Literacy

3.43

A common concern raised by multiple witnesses, is the level of literacy

of recipients of the departments communications, and the style of language used

by the department, which together can create a significant communication

barrier. The Law Society of South Australia noted:

The initial notices are received frequently by

poorly-educated individuals and not infrequently by individuals who have a

limited command of the English language. It is to be expected that some will

interpret the initial notice as actually being a notice of demand.[41]

3.44

This view was echoed by #NotMyDebt, who stated 'The multistage review

process is convoluted, protractive and oppressive, especially for vulnerable

clients with low literacy, self-esteem, language skills or mental health.[42]

3.45

The Youth Network of Tasmania agreed the communication from the

department was overly complex, and noted that in relation to younger income

support recipients:

[I]t is also about the

complexity of the language and complexity of the information they are required

to provide and about the understanding of the disclosures that they need to

make every step of the way.[43]

3.46

The Launceston Community Legal Centre told the inquiry that the

complexity of language used by the department meant that in order to achieve

progress, an individual was best served by a professional who understood the

specialised language:

[T]he best and most helpful way for those matters to be

handled is for me or someone to assist the client to get all of their material

evidence together and get it into Centrelink. There is a particular set of

words you have to use. It is what I call Centrelink English, which is quite

different to Australian English. If you do not use the right words, you do not

always get the right outcomes.[44]

3.47

Ms Basterfield, a consultant speech pathologist, concurred with this

view of the complexity of language used by the department, but stated she

simply referred to it as 'government English'.[45]

3.48

TasCOSS told the inquiry that literacy can be a greater challenge,

depending on location. TasCOSS pointed to the multiple levels of intersecting

communication barriers faced in their jurisdiction:

Tasmania has the highest rate of population receiving any

kind of income support payment and across all different payments available.

Tasmania has the highest proportion of our population with a disability,

including an intellectual or a learning disability. Nearly 50 per cent of the

Tasmanian adult population has very low levels of functional literacy and

numeracy. A recent national report released by Telstra shows that Tasmania has

the lowest levels of digital access and digital capability. Tasmanians, like

many Australians living in rural and regional areas, have limited access to

legal assistance and extremely low levels of access to pro bono legal services.

So, putting aside any other issues that have occurred with this system, these

factors alone mean that dealing with any system that relies on online written

communication will be fraught with difficulty. This should have been foreseen

by the government and it should have been addressed.[46]

English as a secondary language

3.49

A number of submitters raised concerns around Centrelink clients for

whom English is a secondary language. The Welfare Rights Centre South Australia

maintained that:

Another problem is that the letters go out in English,

regardless of whether the person can read English. Communicating with people

from non-English speaking backgrounds has always been problematic for

Centrelink, but even more so when the decision to communicate is made by an

automated decision-making system.'[47]

3.50

ACOSS contended that language barriers for culturally and linguistically

diverse (CALD) people in and of themselves are often not enough to cause a

'vulnerability flag' on a person's account, but such communication barriers do

in fact often create serious disadvantages for CALD people.[48]

3.51

FECCA also raised issues relating to the intersecting difficulties faced

by the CALD community, which went beyond simple language barriers:

Many migrants and refugees learn English as their second

language and report that, at times, they struggle to use Centrelink's automated

systems due to comprehension difficulties. Some claim that they may be entering

their details incorrectly due to a lack of understanding of the system. Clients

are exasperated at the lengthy call-wait times and the limited non-automated

support. They suggest that it is almost impossible to receive face-to-face

support from a person without waiting for significant periods of time and, once

they do, they are referred to an online form, which is no good to them. Older

clients, new migrants and refugees report that they have difficulty in

completing the online forms because they do not have a computer and the

internet, and nor do they understand how to use digital technology.

Furthermore, they do not have someone who is available on a routine basis to

provide assistance with income data reporting. Some clients have been told that

they have needed to provide pay slips, bank statements and letters from their

employers dating back to five years ago. This has proven difficult for some

clients, as their previous organisations have closed and no longer exist.[49]

Disability-related communication

barriers

3.52

Children with Disability Australia told the committee they were not

aware of any communication assistance that had been put in place to help people

with a disability or their families in navigating the OCI system.[50]

3.53

This evidence is supported by the personal experience of Michelle, who

provided evidence to the committee that when she attended the Centrelink office

to query her debt notice, she was directed to use the phone system, despite the

fact she is deaf and had a communications support person with her:

At first they asked me to ring and I said, 'Hang on, I'm

deaf.' My support worker was getting agitated going, 'Look, she's deaf—this

can't happen.' They tried to force her to become the contact person, and that

person did not want that; that person respects my privacy. They ended up

forcing her to ring, and she did not want to and then walked out. My carer

ended up walking out because they forced us to ring, whereas they should have

done their job and assisted me.[51]

3.54

LawRight provided evidence relating to a client they assisted who has

'the reading age of a five- or six-year-old and the maths age of a six- or

seven-year-old.' LawRight did not specify whether this person had a

vulnerability flag, but submitted that in communicating with this person, the

department sent 'a printout of payments made to the client dating back to 2001'

but that the print out was not accompanied by any explanatory notes and was so

complicated that even the LawRight lawyer did not understand the information.[52]

3.55

Access Easy English submitted that there is a requirement for important

information to be provided to people with a disability-related communication

barrier in an 'Easy English' format, but found that 'CentreLink complaints processes

and forms are not presented in a way these particular clients can use, to raise

their concerns about access

to written information.' To address the deficiency, Access Easy English

recommended the department implement a 'whole of CentreLink/DHS approach to

Accessible Information, in particular, Easy English.'[53]

Geographic barriers

3.56

The committee received evidence of the impact that geographic barriers

to communication has had on individuals. In particular, the committee notes

that the need to travel long distances to Centrelink offices and/or legal

services has increased the hours individuals have spent in resolving purported

debt matters:

There are alleged debts that people have travelled hours to a

Centrelink office to talk to somebody about, because they could not reach

anybody through their call centre network, only to find after two visits that a

debt had not occurred. The one example that a member told me about was somebody

that had to get on a bus for an hour and 15 minutes to get to a Centrelink

office not once, not twice but three times before the matter was resolved.[54]

3.57

The National Union of Students stated travel distances have impacted

students who tried to attend Centrelink offices to resolve their cases:

We have had students in rural

and regional areas drive out or catch the bus to be told that they could have

just done it at home and then they subsequently have had to wait even longer.[55]

3.58

This issue was also discussed in media reports on the OCI program, with

the ABC's Background Briefing radio program outlining the case of Greg Steen,

who lives over 100 kilometres from his nearest Centrelink Office. After a

number of trips Mr Steen had travelled over 1000 kilometres to resolve his

purported debt matter.[56]

Committee

view

3.59

The committee notes evidence that there is a broad systemic problem with

the way the department engages with vulnerable clients, which has been

exacerbated by the OCI system.

3.60

The committee is deeply concerned for the people in the system who have

not been properly identified as vulnerable, noting that to some extent,

everyone who uses income support payments is vulnerable in some way.

Debt notices

3.61

The inquiry received a range of evidence that people often first found

out about their purported debt when they received a debt notice from the

department, or when they were contacted by a debt collector. As noted earlier

in this chapter, an estimated 6 500 people did not receive the initial

letter requesting income clarification from the department, due to incorrect

addresses being used. ACOSS noted that '[w]hile Centrelink could not track down

these people to provide them with the information about a discrepancy or,

indeed, an alleged debt, debt collectors have seemingly had no trouble doing

so.'[57]

3.62

Whether or not a person knew about the purported debt, the receipt of

the formal notification of the purported debt was noted by many individuals and

organisations as a stressful experience for people:

Life is stressful enough on Newstart, living from week to

week and trying to find work and making a better life for yourself. It is only

made worse by stressful events such as receiving a debt notice. I can only

imagine the suffering someone who received a larger debt would experience.[58]

3.63

This experience was echoed in evidence presented by advocacy

organisations such as the Welfare Rights Centre South Australia Inc:

Many clients are extremely distressed by such letters and

believe they are being accused of cheating. I personally spoke to a young woman who suffers from anxiety,

who was extremely agitated and upset. She was crying and repeatedly told me

that she was not a cheat. She was frightened that the debt, which was $17,000,

would result in her going to jail.[59]

3.64

Tom characterised the debt notice as a fishing expedition, stating 'the

debt notice was like a fraud; it was like a scam. You cannot send a letter

saying, 'I accuse and you are guilty.'[60]

3.65

The inquiry also received evidence of individuals who first became aware

of a purported debt, because deductions were made from their income support

payments. In these cases, the individuals had not received any prior communication

regarding the purported debt matter. Queensland Advocacy Incorporated (QAI)

discussed the case of a client who told QAI 'she did not receive a notice or

letter, but she simply noticed that there was $86 missing from her Newstart

allowance of $536 per fortnight. This is obviously a substantial

proportion—more than 10 per cent—of the allowance.'[61]

3.66

Financial Counselling Australia outlined its understanding of the

process for Centrelink to begin automatic deductions from income support

payments, and the impact this can have on individuals:

When the Centrelink system identifies a debt for a person

currently in receipt of Centrelink payments, this triggers automatic deductions

of 15% of that person's pension or income support as repayment. As people in

receipt of Centrelink benefits typically already live below the breadline, 15%

of income support can mean the difference between being able to afford

essentials or needing rent/food relief from an emergency relief provider.[62]

Access to information

3.67

Throughout this inquiry, individuals and legal and advocacy

organisations from around Australia gave evidence that the department withheld

information that a debt letter recipient needed to understand how the purported

debt was calculated. This included information to enable them to work out what income

information may be incorrect and have the effect of creating an incorrect debt

amount. Many organisations stated they resorted to Freedom of Information (FOI)

requests to force the department to release information that was denied on

initial requests.

It seems to me to be quite ludicrous that we even have to go

to freedom of information. I used to think that the child support letters were

incredibly complex, until this started. But at least with the child support

letters, if a person who had sought our service had a difficulty, I could read

about the period over which that debt was incurred, what incomes were taken and

the percentages of shared care, and then we could work through it together.

But, as someone trying to assist, I will ask the question: 'Why do you have

that debt? How long have you had it for? What payments do you receive?' People

say, 'I don't know—I just have this debt.[63]

3.68

Many individuals provided copies of the information they received from

the department, to show how difficult the data was to understand:

This thick wad of paper is the FOI, and it is total

gibberish. It is just rubbish. None of the income numbers in there make any

sense, and none of them correlate. I cannot make any sense of it.[64]

3.69

Even when information was provided, individuals had difficulty in

understanding how the department had calculated a purported debt amount. Tom, a

retired Chartered Public Accountant, described the information he was provided

with as 'pure kafka' and said that as a trained financial professional, he found

the department's explanation of how the purported debt was calculated as

'crazy' and stated 'I am a practical person. I am a trained accountant. I

cannot listen to stuff like that.'[65]

3.70

The Australian Privacy Foundation put forward a similar view, stating

that in trying to establish that a purported debt is owed, the onus of

communication sits with the department:

I use the fundamental justice principles, which are that you

either make your case for the debt being owing or you do not have a case.

Failing to provide information is a separate issue of the responsibility

obligations between the individual and Centrelink. When it comes to debt, the

justice system is quite clear. It is just that Centrelink does not want to comply

with those principles.[66]

3.71

The Welfare Rights Centre South Australia contended that despite

requesting information to clarify an income discrepancy, in many cases that

information already sat within the department's information systems:

Some customers do not have the information necessary to

demonstrate their compliance. If, for example, a debt is raised up on the basis

of income earned seven years ago, it is unlikely the client would have the

information necessary and it is unreasonable to expect them to. The irony is

that in many of these cases Centrelink already has the information necessary on

the customer records which a human decision-maker could assess.[67]

3.72

The difficulty in accessing appropriate information was raised by legal

services as being a key impediment to providing advice and assistance to

individuals in relation to their purported debt matter. Basic Rights Queensland

told the inquiry:

Centrelink's debt calculations are not actually freely

available to the public. There is a debt calculator on the online compliance

site where Centrelink customers can enter their figures and get an estimate,

but experience from our colleagues interstate indicate that once a person has

appealed a debt that calculator is no longer accessible. This means it is really

difficult for advocates like us to actually assist a person... The system is

failing to meet minimum requirements of procedural fairness because, despite

the fact that it is actually possible to provide the correct information, it is

not always accessible and there is insufficient information about how to use

it.[68]

Committee

view

3.73

The committee is deeply concerned with the lack of clarity in

information provided regarding individual purported debt matters. This includes

both sufficient depth of information as well information provided in an

appropriate form particularly for vulnerable people and people with

communication barriers.

3.74

The questionable action of reversing the burden of proof onto income

payment recipients, where people are being asked to prove they do not owe a purported

debt, is discussed in great detail in chapter 4. What makes this reversal more

problematic, is the lack of information provided to individuals and their

advocates, that they need in order to prove the purported debts are not correct.

Centrelink communication channels

3.75

The department has three main communication channels for individuals to

interact with Centrelink: storefronts, online portals and via phone. The

inquiry received evidence of difficulties people faced with all three communication

channels.

3.76

The department discussed the various communication channels available to

individuals, and told the inquiry that individuals were encouraged to use phone

and online communication portals, as frontline staff at Centrelink offices have

not necessarily had the appropriate training to assist people with the OCI

process:

We encourage staff to get recipients to go online, and one of

the main reasons for that is that, once they are online, they can also contact

the 1800 number. If you go to a Centrelink office—there are 350 throughout

Australia—it is not always likely that the person there will be deeply

experienced in these matters.[69]

3.77

The inquiry received evidence that this encouragement of use of online

portals was not always considered by Centrelink officers to be the best way to

resolve purported debt matters. The Community and Public Sector Union told the

inquiry:

Frontline service officers reported when they get customer

details on the screen, when they are face-to-face with people, they would often

find errors that they would be able to correct very quickly but they were told,

quite quickly, not to do that and to push people back onto self-service portals

to get them to use the online system to correct their own details. They also reported

that people in the debt management teams were instructed only to deal with a

very small portion of the debt management process despite their experience

telling them that there were errors in other parts of the record.[70]

3.78

Multiple witnesses to this inquiry, both individuals and organisations,

stressed the need for flexibility in the communications channels. While a large

proportion of people may find online systems convenient, many people require

telephone or face-to-face assistance for a variety of reasons. These issues are

discussed in the following section.

Centrelink online portals

3.79

As outlined in earlier this chapter, the premise of the OCI program is

to require individuals to provide detailed income data to retrospectively

verify their eligibility for income support payments. In the first instance,

the department directs people to provide this information via its OCI online

portal.

3.80

The online portals, both myGov and the OCI-specific website, were described

by many as being very difficult and complex to navigate, and 'inhibits people's

ability to provide accurate information that is very much needed when looking

at whether or not someone owes a debt.'[71]

3.81

For many people subject to the OCI program, simply accessing the online

world is a challenge. The Legal Services Commission of South Australia told the

inquiry:

They do not have internet and they may not have mobile

phones, so their preference is to go personally to Centrelink and seek

assistance. It was specifically noted by her that those who have casual jobs or

intermittent positions prioritise other necessities, and the internet and

mobile phones may not necessarily be high on those lists.[72]

3.82

This evidence was repeated by People with Disability Australia, who told

the inquiry:

[W]e know that there is a problem with access to the

internet, generally, for a lot of people. Whether that is because of where they

live, whether that is because there is not community access in the communities

that they live in, it is definitely a problem. Having someone to call, having

someone to talk to, having a place to go and see people in person is absolutely

imperative.[73]

3.83

One witness

pointed out that although many people could access the internet through places

such as a library, there were privacy concerns for sending personal data over a

publicly accessible internet system. Susan stated that 'I could tell you a

little about having to give my bank records, which I had to do in a public

library. I was very scared someone was going to access my bank details over the

wi‑fi.'[74]

3.84

Access

Easy English submitted that a significant proportion of the Australian

population, 52 per cent, has non-functional numerical literacy which is 'critical literacy for the correct

administration in areas such as meeting attendance, planning and time management,

adherence to conditions in CentreLink letters, to name a few.' Of greater

import, Access Easy English submitted that in testing of problem solving

technology-based information (online information), 62 per cent of users were

found to be non-functional, and furthermore, 1 in 5 households do not have

access to the internet.[75]

3.85

Even for highly digitally literate people, communicating via the online

portal created difficulties in uploading information requested by the

department. Basic Rights outlined a process a client took to upload income data

to show there was no debt owed:

They went through an enormous process to try and address

this. They made seven separate attempts to upload the correct pay

documentation—keep bearing in mind that this is a tertiary educated person. As

they could not get this to work, they photocopied the pay slips and sent them

by registered mail on 26 October.[76]

3.86

Conversely, Ian explained his difficulty in communicating with the

department was that while he was told he must submit information via the online

portal and not via an email, the department said it would accept information

via fax:

I said, 'Yes, I'll email it to you.' They said, 'No, we don't

use email here.' I said, 'What! It's the 21st century.' They said, 'We don't

use email here.' They said, 'You could send it by myGov.' And I said, 'Well, I

don't have a myGov account.' ... The only other option they gave was to fax the

letter through to them. And, of course, who has a fax machine in their home? To

go to the post office, I think it was going to cost me $4.50 a page to send

this letter through. It was a letter of some eight or nine pages—so $40 to get

a letter to Centrelink.'[77]

3.87

However, evidence was received that suggests the difficulties

experienced are not limited to simply accessing the online portals, but stem

from the design of the online website itself. The National Social Security

Rights Network stated the key problem was the usability of the site:

The outstanding impression I have had so far is that the

majority of people who have struggled are not people who are unwilling to use

online channels, they have just had great difficulty using this. There are some

people for whom on line is inappropriate or difficult or they do not have

access, but the main cause of problems is that DHS fundamentally underestimated

how usable their system was.[78]

3.88

People with Disability Australia agreed the online portal was not

user-friendly and described the online portal as having 'some good features to

that but they were not easy to use, they were not easy to navigate and it was

not necessarily clear how to navigate around those. So without that guidance,

those tools may be available but they are difficult to access.'[79]

3.89

UnitingCare Queensland noted that may of its clients required assistance

to navigate the OCI website:

However, in working with these clients, the main concern we

found was with the online service portal and having zero to minimal capacity to

navigate that system. They all stated that that caused a great deal of distress

and that that they needed help via a financial counsellor to navigate that

system.[80]

3.90

The usability of the OCI website formed part of the investigation of the

OCI process by the Commonwealth Ombudsman. The investigation report details

examples where the website does not provide sufficient warning that 'accepting'

the ATO annual income figure data will result in income averaged fortnightly

and a higher chance of a purported debt being calculated.[81]

3.91

The report further expresses concern that even where people are aware

they must enter fortnightly earned income data in order to avoid a purported debt

being calculated, the OCI website itself does not provide a simple method to

insert this data. The report uses an illustrative example of a 'reasonably

well-educated' user who attempted to update her income data but 'found the

questions in the system too narrow, as they only asked her to confirm her

employers and her group certificate amount. After Ms D completed the OCI

process, the system advised her she owed a debt of $2203.24.'[82]

3.92

The committee received evidence from the department that the OCI portal

was developed within the department, and did not receive extensive outside user

testing. The department outlined the testing process to develop the OCI portal

included:

-

an internal exercise to identify if the online compliance system

was working; and

-

a pilot between July and September 2016 of 1 000 people selected

for intervention, with monitoring to check for any process or system generated

issues.[83]

3.93

The department has confirmed that since the date of the above

complaints, the OCI website has been updated, in February 2017. The department

outlined the process it went through for subsequent user-testing of the updates

for the OCI website:

It was an interactive process with users. We had a range of

users we brought in to test screens with and to test explanations in the help

with. So it was an interactive process. Overall, the feedback we had was to

de-clutter the screens.[84]

3.94

The department was asked whether the user-testing included vulnerable

people and those with communication barriers. The department confirmed only

that they used 'a broad sample of recipients and former recipients'[85]

which included 'volunteer members of the public and departmental employees'[86]

and that although other programs conduct testing across Australia, the subsequent

refinements to the online portal were only tested by users in Canberra.[87]

3.95

The pages of the website were provided to the inquiry as a briefing to

the committee, and submitted in hard-copy. The updated website now includes a

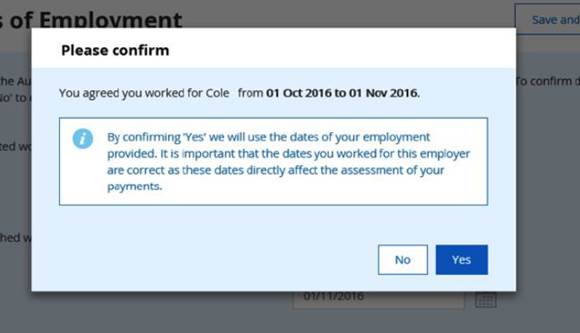

warning that dates of employment will impact the debt calculation – referred to

as 'assessment of payments'. However, the warning appears at the point a person

verifies their overall start and end dates of employment. See image 3.1 below:

Image 3.1

Source:

Department of Human Services, Submission 66.1, Attachment A Employment

Income Confirmation' 1 June 201, p. 19.

3.96

If a person simply confirms the start and end dates of employment but

does not go on to complete the fortnightly income stage of the website, they

will potentially be liable for an incorrectly calculated debt because of the

department's practice of averaging ATO annual income data.

3.97

Concern was raised by ACOSS that if the program was expanded to capture

income sources more likely to be received by the age pensioner population,

difficulties already being found with the online portals would be far greater:

If this program is expanded to income from areas other than

employment—what will mostly be the age pensioner population—there is a much

higher risk that the person will have poor digital literacy and may not even

have access to the internet. It is envisaged that this group is going to need

much more support than that received by the people affected by the current

program. There are also clear concerns about people's vulnerability. It is safe

to say that the proportion of people in the age pensioner population who have

some kind of vulnerability will be much higher than we have seen amongst the working-age

population.[88]

Centrelink storefronts

3.98

Evidence was received from a number of witnesses that individuals

subject to the OCI program were denied service at Centrelink storefronts. The

Community and Public Sector Union raised this as an issue of particular concern

for their members:

Members have been particularly disturbed by reports of

managers instructing frontline staff not to correct errors that they find and

instead to push customers onto self-service mechanisms and/or refer them to a

different part of the department—namely, the OCI teams.[89]

3.99

However, the department discussed this issue and responded that letter

recipients were encouraged to use phone and online communication portals, as

frontline staff at Centrelink offices have not necessarily had the appropriate

training to assist people with this particular issue:

We do not have the capacity to train all our staff up to do

every element of business across the Department of Human Services, so we stream

into expert type areas. This is an expert type area, so what we wanted was for

recipients to engage with the system and then engage with the 1800 number,

which has the people who are expert on this, rather than any of our service

staff in the offices.[90].

3.100

However FECCA pointed out that CALD community members can often have

greater difficulty communicating via phone and online than in person:

Given the reports that Centrelink staff were told not to

process debt disputes in person, if they are unaware of Centrelink's

multilingual phone service, language may discourage them from using the phone

service to challenge their debt letter. Many CALD Australians have limited

digital literacy, and FECCA has done a lot of work around this. Low levels of

English language mean they are unable to navigate government services through

online portals. So they just pay, whether or not they are liable for that debt.[91]

3.101

Conversely, other witnesses pointed to the general inappropriateness of

having to discuss highly personal details in the Centrelink office. The

National Council of Single Mothers and their Children stated '[i]f you are

completely stressed out and go into a Centrelink office, you are publicly asked

what your issue is and someone makes a notation on a tablet if you cannot do

that yourself and then you wait in a very public space.'[92]

3.102

Some witnesses pointed to Centrelink offices as being inappropriate

spaces for vulnerable people due to the level of aggression that can now be

found in Centrelink storefronts:

I am 67 and I am afraid to go into the Footscray Centrelink office.

The number of times that I have been in there where there has been someone who

has become so frustrated with the system that they are angry and threatening

everything from, 'If I had a bomb, I'd blow the place up,' to, 'Someone should

bring in an AKA and just shoot the place up,' means that I now do as much as

possible on the phone.[93]

3.103

The department stated there has been no increase in aggressive behaviour

from customers at Centrelink storefronts and stated 'We do have a small number

of incidents—and those incidents occur every day—where people are aggressive

and take it out on the staff members. But we have not seen an increase in the

last few months on that issue.'[94]

3.104

Evidence received by individuals, and backed up by organisations, points

to the incidents cited by the department above as often being used by

Centrelink staff as an excuse not to provide service to difficult people:

But there are a lot of cases where I have spoken to people

who have said, 'I just questioned the Centrelink staff member on this issue,

and the Centrelink staff member felt unsafe by being questioned'—maybe their

tone of voice was a little higher than usual because they were frustrated.

Instead of engaging with them as humans and trying to work out their problem,

the staff member says, 'I don't like the tone you're speaking to me with, and I

want you to leave.'[95]

3.105

An example of this was provided by Michelle, who told the inquiry:

They actually ordered me out of the office and that made me

feel even worse... I was not abusive, threatening or angry. I was frustrated. I

was complaining about a letter and then I was dismissed. Sadly, it made me feel

as if I had done the wrong thing, but I had not.[96]

Centrelink phone systems

3.106

The issue of people not being able to reach the department by phone was

a key concern raised by many witnesses and submitters throughout this inquiry.

This was exacerbated by the initial letters being sent out without the

dedicated OCI phone number being included. Although the department has since

updated the letters to include this information, the Commonwealth Ombudsman has

pointed out the number is printed on the second page of the letter and 'is not

obvious to the reader'.[97]

3.107

The committee heard that people experienced difficulties getting through

on the phone in the first instance, as well as long wait times after the call was

first answered by Centrelink. The Community And Public Sector Union told the

inquiry:

More than 36 million calls to the Department of Human

Services went unanswered last year as the department is no longer able to

provide a basic level of service to Australians.[98]

3.108

One witness, Jade, summarised the impact this can have on individuals by

stating 'The fact that it is nearly impossible for people to reach Centrelink

on the phone leads to people being more likely to accept the debt and not

challenge it.[99]

3.109

The Victorian Council of Social Service quoted a complaint letter they

received which stated:

On Wednesday 22 March, I phoned 132850, 16 times between 1 pm

and 2 pm. The line was busy for the entire time. At 2.13 pm, I telephoned the

1300306325 line. I was then on hold for three hours and 12 minutes. This is

outrageous and unacceptable. I know this is not a one-off situation as a staff

member I eventually spoke to at Centrelink told me, not once but twice, that

that kind of wait time is common on this line.[100]

3.110

The Financial Counsellors Association of Western Australia stated this

issue did not just impact individuals, but also impacted professionals who were

attempting to provide assistance on debt matters and had experienced great

difficulty in contacting Centrelink via phone when they were in a mediation

session with clients.[101]

3.111

The department has previously provided evidence on the 'average speed of

answer' times for the debt phone lines for the period beginning July 2016 to

end January 2017. The committee notes the department's advice that the average

waiting time for the 1800 Compliance phone line was 40 seconds and two minutes

and four seconds for the Debt Recovery and Raising phone line.[102]

3.112

IsCentrelinkDown described the call

data presented by the department as 'number-fudging' because the department does not record call

handling time at an organisational level, but instead resets the clock every

time a call is transferred.[103]

3.113

IsCentrelinkDown developed a testing program for the phone number

given on the initial debt letter, 1800 076 072, and found that on average, a

call to this number had a 27.44 per cent chance of not being answered, which

went up to 50.0 per cent at 12.00pm when a large volume of calls were made

during people's lunch breaks.[104]

3.114

IsCentrelinkDown noted the cost to individuals as a result of lengthy

wait times to have their questions answered:

Mobile calls to 13/1300 services are always charged with a

flag-fall and a per-minute rate, making long hold times expensive. This makes

no sense that we are lumping those with the least ability to pay for phone

calls with 13/1300 numbers including crisis services. Meanwhile the DHS 'purchasing

helpdesk' for the Dunn & Bradstreet contract is a 1800 number. This

displays poor priorities.[105]

3.115

Once people managed to have their call answered, they reported

difficulty in having to explain a complex situation to one Centrelink officer,

only to have to repeat the same information the next time they call and speak

with a different staff member.[106]

3.116

The National Social Security Rights Network also pointed to the

confusion created when individuals calling Centrelink are unable to find the

right section to speak with about their case:

[a] number of people have also expressed frustration and

confusion about not being able to access the right information when they have

attended a Centrelink office or called through on the general Centrelink

numbers. That reflects, of course, some poor decision making about

implementation, including not making the 1800 direct number to compliance

officers apparent.[107]

Committee

view

3.117

The key concern with the OCI process, is the outsourcing of the income

checking process to individuals. With this comes an inherent reversal of the

burden of proof – the department claims an income discrepancy and requires an

individual to seek the information required to prove the discrepancy does not

exist. If the individual fails, they will owe a debt of potentially many

thousands of dollars to the department.

3.118

The two fundamental resources a person needs to undertake this process

is a method of communicating, and once that communication channel is opened,

the receipt of information that is both comprehensive and comprehendible.

3.119

The department is clearly failing to provide those two necessary tools

to allow people to challenge the income discrepancy, and is reaping the benefit

through debt payments.

Navigation: Previous Page | Contents | Next Page