Chapter 3

Problems the bill seeks to address

3.1

The ARDB's tasks would relate to the financial viability of Australian

agriculture and associated industries, and the financial arrangements entered

into by these industries. This chapter examines the stated reasons for

establishing the proposed ARDB and considers whether there are strong grounds

for creating such a board within the RBA.

Challenges facing regional Australia

3.2

The committee received many submissions from farmers and people in rural

communities that expressed support for the proposed ARDB. Submitters cited many

of following challenges affecting regional Australia when arguing for the creation

of an ARDB. These included:

-

access to finance and changes in bank lending practices since the

global financial crisis;

-

declining farm profitability;

-

farm debt levels and their sustainability;

-

the flow on effects of challenging agricultural production and

market conditions for small businesses reliant on farming businesses;

-

market interruptions, such as the suspension of live cattle

exports to Indonesia in 2011;

-

recent natural disasters, such as drought and floods;[1]

and

-

the sustained high Australian dollar.

3.3

Many who participated in the inquiry drew attention to problems being

experienced in parts of rural Australia. They spoke of excessive debt, unserviceable

loans, foreclosures, insolvencies and rural suicides as evidence that the ARDB

model was needed.[2]

For example, Mr Rowell Walton stated:

Reports recently garnered from our community suggest some are

now faced with no income, the banks are in retreat and unprepared to further

lend, some people are said to be unable to feed themselves. As an Australian I

am embarrassed to have come to this place. I imagine the bankers would feel no

particular comfort; the solutions rightly belong in the public domain.[3]

3.4

Indeed, Mr Walton told the committee that many people were now saying

that they had 'never seen it as difficult as this in their history or to their

knowledge' with capital values falling while rates were 'in fact rising'.[4]

In this context, a number of submitters gave their personal accounts of

life in regional Australia. Mr John Whitehead, whose family had owned and

operated Mentone Station in central Queensland since 1914, argued that the drought

affecting beef producers was a major disaster because it followed other

particularly unfavourable events and market conditions:

Over the 100 years of our time

here there have been plenty of droughts and hard times, but there has been

nothing like the time we are experiencing at the moment. In the past they used

to earn enough in the good times to ride them through the bad times and they

would come out the other end knocked around a bit but they would get up and

start off again. Now we earn enough in the good times to just cover costs and

put a bit away, but nowhere enough to get us through a disaster like the one we

are experiencing now. There have been plenty [of] times when we have had worst

dry spells then this, but never the combination of negative forces against us.

This drought has had the perfect lead up for a major disaster, the global

financial crises, out of control expenses, the live export ban, low stock

prices, high wages, higher than normal stock numbers and these are just the

major issues. There are plenty of local issues affecting us as well.[5]

3.5

Mr Xavier McKinnon, a veterinarian from Cobden, Victoria, whose business

relies on the local dairy industry, advised that at least a quarter of his

clients have told him their bank is not lending any more money for feeding

cows. Mr McKinnon provided the following outline of his views as to why

his local dairy industry was under pressure:

In the last 10 years we have had the boom and bust of the

managed investment schemes that pushed the price of land up to an unaffordable

level, they promised returns they could never produce and got tax breaks by

doing this! This new supposed value of land lead to banks' lending against

unrealistic valuations and leaving the farmer exposed to any downturn no matter

how minor it may have been! Now that the price of land has dropped the banks

are putting pressure on the farmers telling them that their debt levels are too

high. We have also had the price of milk drop to unrealistic levels at the

farm-gate, a high Australian dollar making it harder to compete on the export

front, one of the wettest seasons ever followed by one of the driest seasons

ever! We also had a little thing called the Global Financial Crisis which has

impacted the export market![6]

3.6

A 28 year-old farmer from the Western Darling Downs wrote that, after

studying agribusiness at university, he decided not to return to his family's

farm after concluding that the farm's income could not support him. He also

highlighted the flow on effects that occur in regional communities when

agriculture struggles:

Agriculture has seen a perfect

storm in that we have seen near a decade of drought to be finished off with

floods while the GFC cause[d] the dollar to rise which reduced the value of

commodities and has made it harder to obtain working capital. This poor decade

has made it very difficult for farmers to operate as the level of debt has

increased across the board.

The flow on effect of such increased debt within the industry

is that farmers have reduced their spending on inputs which is causing local

companies that supply these inputs out of business while also making the

agricultural industry increasingly inefficient. In my search for employment

away from the farm I have seen that the level of positions available is reduced

due to the reduced capital that farmers are spending.

The agricultural industry is too large and affects too many

people across the country for it to fail, the government must step in and

restructure their polices to help this industry before it is too late. The

Australian Reconstruction and Development Board is desperately needed to

maintain efficiency and not lose our land to less efficient foreign investors.[7]

3.7

A Western Australian farmer submitted that changes to lending practices

following the global financial crisis had made their financial position

difficult:

Up until the GFC and subsequent run of seasons we had

received unwavering support from our bank. This gave us the confidence to

invest in our industry and take on risk (which has not always been a Yilgarn

farmer's desire or strength)...Since the GFC we have had to endure risk profile

recording, increasing annually our risk margin, now seeing finance costs 2‑3%

above that of a housing loan for the general public, a re-evaluation of our

land at our own cost ($8,500) and a cap on bank lending forcing us to seek out

third tier lenders for short term deferred accounts at interest rates up to

18%.[8]

3.8

Debt dominated the concerns raised in submissions. Ms Erin Lawless wrote:

We really only have one (1) sustainability issue: our costs

of production will always increase, while there is no mechanism in the market

for our prices to meet rising costs.

We are a 'book-end' in the market. Unlike other industries

and other sectors of this industry, there is no one to whom we can pass on our

costs. We absorb and absorb and innovate as best we can, but eventually we

have haemorrhaged people from our industry and communities, and tried to patch

this market-structure problem with unsustainable, treacherous levels of debt.[9]

3.9

Other submitters pointed to a range of other challenges they believe

Australian agriculture faces. A citrus farmer from the Riverina region of

New South Wales expressed discontent with numerous government

policies:

...Australia's blind following of the belief in free trade and

deregulation has left farmers suffering and unable to compete with juice or

fruit coming from countries which don't have the same environmental, social or

quality standards. These are forced onto us but not onto imports. Social issues

include minimum wage, [occupational health and safety] and super contribution.

Quality include safe use of chemicals, product traceability and various

accreditations and registrations. Environmental includes carbon tax, water

reform and restricted farm practices. All of these come at a cost burden to the

Australian producer and are not placed on the equivalent imported product.[10]

3.10

Another submitter argued that deregulation and the removal of tariffs

meant that funds needed to be made available to rebalance the financial

circumstances of many farmers, as well as industries dependant on farming:

Producers who have as a result of a change in government

opinion, and policy, had all risk amelioration removed from their industries,

dairy, grain and every industry which has lost its protection, whether

countervailing market power, import protection via tariffs, or simply drought

and exceptional circumstance provisions. Government have effectively passed all

the risks of production on to the producer, this has been both deliberate and

profound. Unfortunately many have carried excess debt, in the circumstance,

provided and based upon a system, which now simply does not exist. It may well

be there is an argument for compensation to readjust debt levels more in line

with risk now set by policy.[11]

3.11

The combination of numerous factors places the financial viability of many

Australian farms at risk. Indeed, the majority of the 145 submissions were

concerned about the level of debt in rural Australia and the struggles facing

farmers trying to keep their businesses afloat. In the following section, the

committee explores the extent of this problem and whether it provides a solid

basis for government intervention.

Is there a rural debt crisis?

3.12

As noted earlier, rural debt was specifically cited as a problem that an

ARDB would address. The Explanatory Memorandum drew attention to the fact that

rural Australia was:

...struggling under an insurmountable debt burden,

characterised by low farm income and lending practices of financial

institutions in deregulated financial markets. In 1980, debt in Gross Value

Farm Production was at 32% and this has escalated to historically high levels

of debt, reaching 135.4% in 2012. With escalating debts, many farmers and

producers are facing foreclosures. Forced sales are widening loan-to-value

ratios, leading to a risk of 'fire sales', which could precipitate a raging

financial contagion that may not be contained to rural and regional Australia.

In such circumstances of uncertainty and risk to nationally

important agricultural and associated industries, reconstruction is critical to

re‑establish a sound financial basis, and development funds to maintain

and sustainably develop capabilities.[12]

3.13

A number of submitters agreed with this view that parts of rural

Australia faced a most serious situation with crippling debt—a situation worsened

by the fear of contagion. Mr Ben Rees, an economist with the rural debt

roundtable and retired farmer, argued that there was a 'long term policy

failure characterized now as a rural debt crisis'. He indicated that prior to

the global financial crisis, lending was based on debt-to-equity ratios

dependant on asset inflation. The crisis, however, 'brought asset inflation to

an abrupt end':[13]

Suddenly, farmers were asked to repay loans from income. The

difficulty was that debt to equity lending had never been designed to be repaid

from incomes. Consequently, overvalued rural assets were written down to more

realistic market levels. The effect of falling land prices undermined the

solvency of farmers who had borrowed in the halcyon days of debt to equity

lending and ever rising land values.[14]

3.14

Dr Mark McGovern argued that during 2013, farm funding became very

difficult for many. He submitted that the use of standard mortgages and growth

in debt funding since 2000 was a cause of the current illiquidity in farm

finance. Dr McGovern argued that the mortgages 'by design assume stable

incomes' despite 'changing production and market realities'. He added there was

also a disconnect between income and servicing obligations, with expected

performance not matching actual results.[15]

According to Dr McGovern, the market response, asset deflation, would be

damaging—'a crisis is triggered by income problems and changes in valuations

leading to spreading concerns about equity levels and repayment prospects'. He

stated:

Contagion becomes a real risk as falling asset values affect

all farms, even those with no debt. Liquidity dries up until the down slide is

seen as complete only after the property overhang is liquidated.

Markets typically overreact, with needless loss of wealth.

With active assets, such as farms, capacity is also destroyed. Serious new

entrants, having delayed until both prices had bottomed and income:asset ratios

rectified, now face considerable restoration costs. A once productive farm

becomes derelict if restoration is too difficult or expensive, not for

production, environmental or like reasons but due to a fatal financial

exposure.[16]

3.15

The Western Australian Farmers Federation also expressed concern about the

current level of farm debt and the potential for property devaluation contagion:

WAFarmers believes strongly that the current farm debt

situation, which is believed to be in the vicinity of $64bn, is untenable.

Aligned with a five-year average national agricultural gross

production value of $42.24 billion (ABS 2014), this represents a debt to income

ratio of exceeding 1.5, which at that level, is considered by the mainstream

banking sector 'to be at significant risk' in terms of the industry's inability

to service the existing debt.

There are certainly sectors within the industry whose

relative debt loading would be proportionally higher than the average,

particularly grains, dairy and livestock systems dependant on the live export industry.[17]

3.16

The National Farmers' Federation (NFF) noted concerns about increasing

rural debt levels. Despite capital investments, which 'ideally hold farmers in

good stead into the future', the NFF argued that 'total farm debt levels at

above $60 billion place the agricultural sector at considerable exposure to

increasing credit costs and ongoing viability'.[18]

The NSW Farmers submitted that the escalation of rural debt in Australia and

the ability to finance this was 'a serious issue for the industry'.[19]

3.17

The committee sought evidence about farm debt and rural lending

practices from relevant government bodies.

3.18

Treasury submitted that rural debt had trebled over the past 15 years.[20]

It noted that rural debt had risen from around 100 per cent of rural output in

the early 1990s to almost 200 per cent in 2012–13.[21]

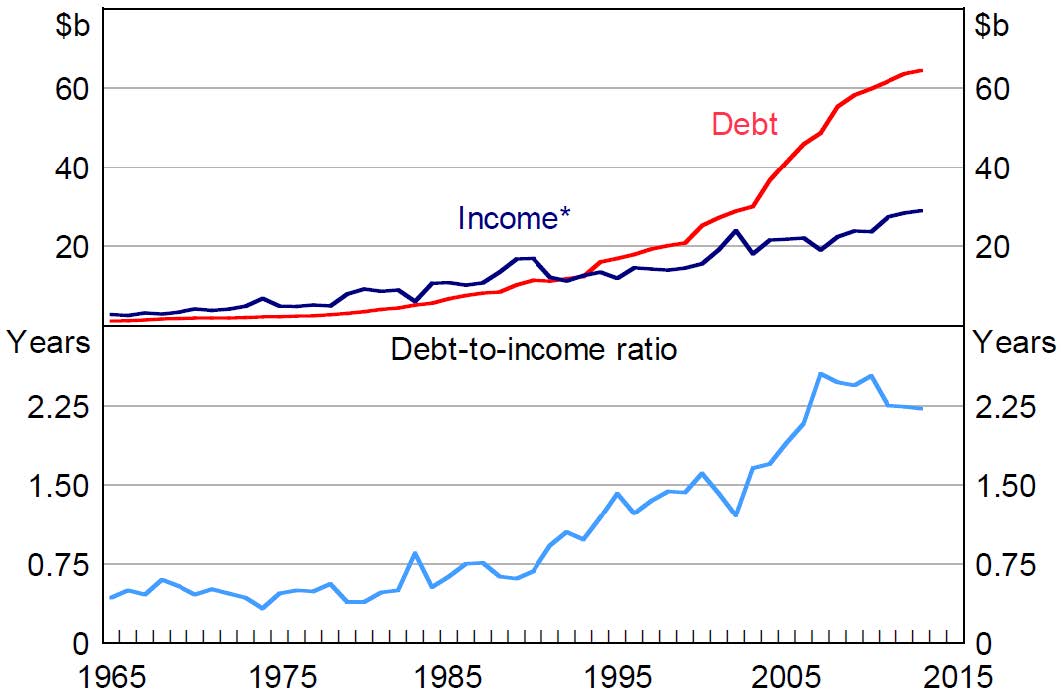

The growth in rural debt relative to income is depicted at Figure 3.1.

Figure 3.1:

Rural debt and income

* Rural income is after deduction of taxes and

subsidies on production and before deduction of depreciation, property income

and cash operating expenses.

Source: Reserve Bank of

Australia, Submission 93, p. 2; based on ABS, APRA and RBA Rural Debt

Survey data.

3.19

According to Treasury, rising cost pressures, over the long term, had

'necessitated increases in productivity in order for farmers to remain

profitable and keep operations viable'.[22]

Land purchases have been a key cause of increased indebtedness, although

Treasury noted that other sectors in the economy had also seen increased

indebtedness since the 1990s. For example:

-

between the early 1990s and 2012–13, the ratio of household debt

to disposable income rose by almost 100 percentage points to 146 per cent; and

-

over the same period, the aggregate credit-to-GDP ratio grew from

around 80 per cent to approximately 140 per cent.[23]

3.20

Treasury added that much of the rural debt was 'held by a relatively

small proportion of mostly large farms'.[24]

3.21

Ms Karen Schneider, Australian Bureau of Agricultural and Resources Economics

and Sciences (ABARES), recognised that debt was an important source of funds

for farm investment and continuing working capital.[25]

She also identified the many factors that have influenced the growth in farm

debt over the past two decades which included:

...lower interest rates, increased use of interest-only loans,

structural adjustment—primarily the shift into cropping, which is relatively

capital and input intensive—higher variability in incomes, increases in the

size of farm enterprises, use of more intensive production technologies and the

slowdown of loan repayments and increases in borrowing to meet working capital

requirements during drought.[26]

3.22

The RBA acknowledged that rural debt had more than doubled over the past

decade, explaining that the marked increase in debt over that period was:

...partly driven by borrowing for farm improvements and capital

investments. The reduction in farm incomes resulting from the widespread

drought in the 2000s also contributed, as farmers increased borrowing to meet

their working capital requirements.[27]

3.23

The RBA stated further that:

Notwithstanding the high debt-to-income ratio, lower business

lending rates and the slowdown in rural debt growth have led to a decline in

the rural sector's interest payments as a share of income since 2008. However,

recent RBA liaison with agricultural businesses indicates that some individual

farms may be finding it difficult to access additional funding due to their

existing high debt levels.[28]

3.24

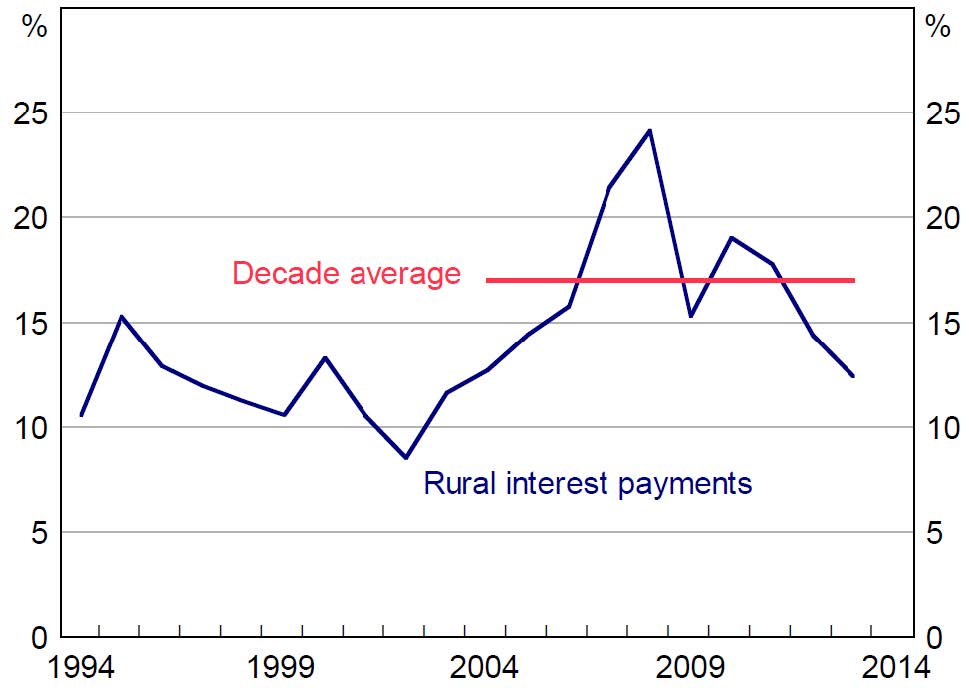

According to the RBA, in recent years, there appeared to have been a

slowdown in rural lending and debt growth, as well as a decline in the

proportion of the rural sector's income allocated to interest payments (Figure

3.2).[29]

The RBA attributed these developments to factors including:

-

farmers increasingly recognising the importance of managing their

balance sheets following previous episodes of drought;

-

growth in rural incomes;

-

higher perceived risk from climate variability;

-

increased economic uncertainty;

-

lower business lending rates; and

-

reassessments by financial intermediaries of the terms associated

with the supply of credit, as part of a broader review of loan performance and

lending standards since the global financial crisis.[30]

Figure 3.2: Rural interest payments* as a share

of rural income

* Estimated using rural debt

outstanding and the average business lending rate.

Source: Reserve Bank of

Australia, Submission 93, p. 3; based on ABS and RBA data.

3.25

The Australian Bankers' Association (ABA) recognised that rural debt had

'grown significantly over the past 10 years'. It did not agree, however, with

the contention that there was 'a rural debt crisis'. The ABA provided the

following summary:

The banking sector has a

strong record in recent times of supporting the rural sector through the 'decade

of drought' on the East Coast and more recently through a prolonged drought

period in the West Coast grains industry. These areas have been recovering and

rebuilding equity. Bank Pillar 32 Reporting indicates that less than 1.5%

of loans to agriculture are more than 90 days in arrears. Bank losses on the

portfolio of rural loans are less than 0.5%. Impaired loans, including 90 days

plus in arrears are estimated by the ABA to be less than 3% of bank loans

outstanding to agriculture.[31]

3.26

The ABA, however, was not disputing that there were people on the land

struggling and that there were people being forced off the land, sometimes

after multiple generations of working that land:

We do acknowledge that there are farmers in specific areas

and industries that are under financial pressure. In the case of Northern Beef

Cattle producers their position has been obviously exacerbated by disruptive

events such as the live export ban and more recent drought. In light of recent

droughts in Western Australia and more recently in Northern Queensland it may

be timely for Government to again review the effectiveness of changes made to

drought programs and assistance provided. The impact of drought affects

producers, at all levels, regardless of whether the[y] hold bank debt.[32]

3.27

Mr Steven Münchenberg,

ABA, cited figures taken from the northern beef industry at the end of the 2014

financial year, where the banks had 1,258 customers in northern Queensland and

of those, 43 were 90 days in arrears equivalent to 3.4 per cent.[33]

Importantly, he acknowledged that there would be customers who were keeping up

with their repayments 'through selling assets including stock'.[34]

While not disputing that there were segments of the agricultural sector

currently in severe difficulty, the ABA contended that:

...the proposition of this bill is based on there being some

form of nationwide problem. They may be solutions that are needed to be looked

at in particular circumstances. But this bill, which would have serious

implications for the risk assessment of lending to agriculture across

Australia, is a systemic response to an issue that is not systemic.[35]

3.28

According to the ABA, government policy should be put in place to

respond to rural debt.[36]

Particular sectors and rural debt

3.29

There is no doubt that rural debt levels have risen over the last

decade. According to the Agricultural Competitiveness Green Paper:

Most of the rise in gross debt over the last decade occurred

prior to 2008 and debt has been relatively stable since then. Key drivers of

the increase included lower interest rates, increasing farm scale, structural

change towards more capital intensive operations, and the availability of

interest-only loans...Higher debt in the 2000s was also supported by rising land

values, with these often not backed up with higher returns that could be earned

from that land.[37]

3.30

The Green Paper noted further that some farms were experiencing debt 'at

unsustainable levels, at least during times of poor cash flow'. It indicated

that impaired loans had risen over the last two years and accounted for around

3 per cent of loans nationally. This rate was slightly above levels experienced

for other Australian businesses in 2010, following the Global Financial Crisis.

Pointedly, however, it noted that:

Impaired loans may be significantly higher than the national

average in some parts of the sector and some geographical areas.

...

The northern Australian cattle industry has been particularly

affected by financial stress—due to a combination of drought and the mid-2011

government-imposed disruption to live cattle exports to Indonesia, which

resulted in lower cattle prices, falling pastoral property valuations and

consequently higher debt-to-equity ratios.[38]

3.31

Indeed, the Australian Beef Association informed the committee that the

cattle industry was 'severely damaged' and needed radical action if it were 'to

be a productive, sustainable and Australian owned and operated industry'.[39]

It indicated further that it was unlikely Queensland cattle producers would

'ever be able to repay the current debt out of income'.[40]

3.32

The Australian Beef Association drew on their members' experiences to

highlight the size of the debt burden. It noted that in 2001 the average debt

per head of cattle was $191, which had ballooned out to $727 per head in 2011.[41]

3.33

Mr Ben Rees, an economist with the rural debt roundtable, could not

reconcile the evidence regarding rural debt given by the ABA and the various

government departments and agencies with that of farmers with on-the-ground

experience. He explained:

I was a speaker, along with Dr McGovern, at the Winton crisis

meeting on 5 December. The Catholic priest of Longreach...said there were at

least 43 people in and around Longreach that he knew were either in

receivership or at risk. On Monday, I took the opportunity of going into Miles

to talk to our local government agent, who helps people when they become

involved in difficulties. She identified 12 people either in receivership or

close to it, and many more, she believed, were at threat.

...Dr McGovern, Mr Walton and I have addressed a number of

farmer meetings across Australia: a thousand people in Merredin, in Western

Australia; 200 at Colac, in Victoria. I and Mr Walton addressed 70 at Hughenden

in December 2013. Mr Walton was present. There were 500 members at Richmond,

farmers, who attended. Dr McGovern and I addressed a meeting at Winton: 350

farmers. This idea that it is just confined to northern New South Wales and

Queensland, to me, is pretty hard to believe.[42]

3.34

Clearly there is a mismatch in perceptions or understanding of the level

and extent of rural debt. A major problem appears to stem from incomplete data

on rural debt, and, while figures about aggregates are quoted, it would seem

they mask the particular and serious difficulties facing certain sectors or

regions in rural Australia.

Data on rural debt

3.35

In his submission, Dr McGovern stated that the overall rural financial

condition was difficult to determine empirically due to the withholding or

limited analysis of data.[43]

Mr Walton stated simply that it was 'unclear how large the actual debt which is

impaired or at risk'.[44]

He stated:

Full and accurate numbers seem very hard to acquire, reports

by the banks that it is all ok flies in the face of ground truthed information.

It is one of the shortcomings of the current information that clarity is not

available. Whether the bankers are compelled to provide full reporting to the

APRA [Australian Prudential Regulation Authority] is unclear, but for certain

whatever data is available does not offer the requisite information for clarity

around quantum.[45]

3.36

The RBA also observed that little public data were 'available on the

performance of rural loans'.[46]

In responding to the observations about the poor quality of data available on

rural debt, the ABA noted that APRA's role in collecting data was 'very much

focused on the stability of the banking system. It will only go to a level at

which they are interested'.[47]

Likewise, Treasury indicated that more data would be useful.[48]

3.37

Ms Schneider, ABARES, agreed that more information was 'always better

than less information' and further that if ABARES had more information on

levels of debt, it would be able to analyse the situation better.[49]

A recent concerted effort brought together ABARES, the Australian Bankers'

Association, the Gulf Cattlemen's Association and the National Farmers'

Federation to share data in order to gain 'a more accurate picture of rural

debt, particularly for the Northern Queensland cattle industry'.[50]

According to Mr Peter Gooday, ABARES:

In terms of the region where the problem is most acute, it is

those regions in the report we did with the ABA and the NFF: northern New South

Wales, northern Queensland, south-west Queensland. It is obvious there that the

proportion of farm receipts required to cover interest payments is

substantially higher than the rest of the country. There is no doubt that there

are issues there. In terms of industries that are most affected at the moment,

the Beef industry stands out as one where, again, the proportion of receipts

required to cover interest payments is higher than most other industries...[51]

3.38

Mr Steven Münchenberg

agreed with the view that there was a gap in information and indicated that

after the joint exercise in 2014, the ABA had approached the government and

suggested that it would provide, on a regular basis, information on the

state-by-state basis and on an industry-by-industry basis.[52]

3.39

Dr McGovern argued that the Reserve Bank was in a position where it

could demand relevant information and 'not be fobbed off' and was also in

contact with the bankers directly.[53]

Committee view

3.40

The committee notes the importance of having a sound understanding of

the challenges confronting rural businesses and communities. The need to hold a

meeting in 2014 when the rural debt situation in northern Queensland had

already been well established indicates that Australia's decision makers have

not been well prepared to make timely and informed decisions. Moreover, the

RBA, ABA and ABARES recognised that more data on rural debt would be helpful.

Recommendation 1

3.41

The committee recommends that the Department of Agriculture and Treasury

consult with the banking sector and the relevant bodies who have identified

deficiencies in the current information available on rural debt. The purpose of

the consultation would be to progress a suitable data collection method to

ensure that the quality of data available to government on rural debt would

provide the information needed for decisions-makers to make timely and well-informed

decisions.

Conclusion

3.42

The committee is grateful to the individuals who were willing to share

their difficult experiences of managing businesses in regional Australia. While

uncertainty and risk are shared by all businesses, the committee understands

and appreciates the additional challenges agricultural enterprises and

businesses reliant on them face.

3.43

The committee is mindful of the need for financial arrangements to be

sustainable. It also notes that there was a divergence of views on the sustainability

of Australia's rural debt. Based on the evidence before it, the committee

observes that levels of debt and the ratio of rural debt-to-income clearly

increased significantly between 2003 and 2008, and have remained high since

then. However, increased indebtedness across other sectors in the economy has

also occurred during this period. Annual growth in rural lending has slowed and

rural interest payments as a share of rural income are currently significantly

below the decade average. Even so, the committee understands that debt levels

vary for different farm businesses, particularly for business that have

encountered natural disasters and other challenges, and currently there are

farming sectors under financial stress and in need of government assistance.

Navigation: Previous Page | Contents | Next Page