Chapter 2

Overview of the Australian credit card market

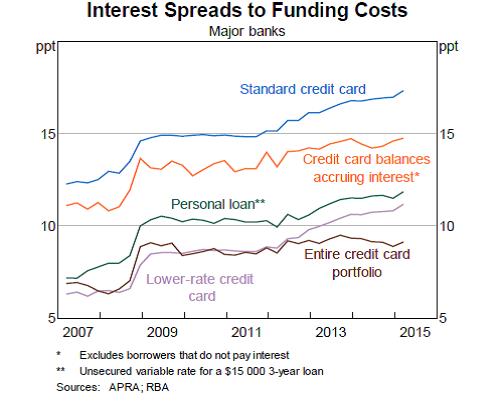

2.1

This chapter provides an overview of the Australian credit card market.

It begins with a brief summary of the importance credit cards have in the

Australian payments system and sets out key data in relation to the value of

credit card transactions and outstanding balances. In turn, this chapter

explains the critical distinction between cardholders who pay off their balance

in full each month and thereby avoid paying credit card interest

('transactors'), and cardholders who carry part of their balance over at the

end of the statement period and therefore incur interest charges ('revolvers').

2.2

This chapter further provides information on the number and type of

credit card providers in Australia, along with an explanation of the current

situation and trends with respect to credit card interest rates and their

relationship to the RBA cash rate. Comparisons are also provided between credit

card interest rates in Australia and overseas.

2.3

This chapter also summarises the responsible lending obligations that

apply to credit card lending.

Use of credit cards in Australia

2.4

In recent decades, credit cards have grown to become a critical

component of the Australian payments system. There are currently around

16 million credit cards on issue in Australia, and approximately 40 per cent

of Australian adults have at least one credit card.[1]

There are also a large number of credit card providers and products available

to Australian consumers: according to CANSTAR data cited by Westpac, as at July

2015, there were at least 83 institutions offering 266 credit card

products.[2]

2.5

Credit cards and debit cards account for approximately two-thirds of

non-cash transactions in Australia (although only about 3 per cent of

the value of total transactions, with high-value non-cash transactions typically

using payment methods such as electronic funds transfer). In 2014–15,

Australians made 2.2 billion credit card payments, with a total value of

$285 billion. According to the RBA, in the June quarter of 2015 new credit

card transactions averaged around $24 billion per month.

At the end of June 2015, the total quantum of outstanding credit card debt was

$51.5 billion. Of this total, $33.1 billion was accruing interest.[3]

2.6

Credit cards comprise a small and (as discussed further below) declining

proportion of total household borrowings, at about 2 per cent according to

the Australian Bankers' Association (ABA), or a little

under 3 per cent according to the RBA.[4]

However, according to the ABA, 'this metric tends to underplay the importance

of credit cards in household finances because they are a revolving credit

facility with loans generally taken for short periods, partly or totally

repaid, and then drawn again'.[5]

In this sense, credit cards provide revolving credit facilities which can play

an important role in helping households manage cash flows.[6]

2.7

Credit cards also play a significant role for Australian merchants. In

its submission, the Australian Retailers Association outlined some of the

benefits credit cards provide to merchants:

[Credit cards] have reduced the risk for merchants having to

keep large amounts of money on the premises and made the point of sale

experience faster and easier. Before credit cards, many retailers held accounts

for customers (where they could take their goods and pay for them at a later

date) for several weeks, thus accepting and carrying the risk of not being paid

for the duration—and in some cases, not being paid at all. With the use of

credit cards, retailers are paid overnight and do not have to worry about

credit losses.[7]

2.8

Typically, interest on credit card debt is only applied if a cardholder

does not pay their balance in full at the end of the one-month statement

period. As cardholders generally have about 14 to 25 days to pay their monthly

balance, this means there is usually an interest fee period of up to 44 to 55

days, or thereabouts. If a balance from a statement period is not paid off in

full, then interest will be applied to the outstanding balance, and any

transactions made since the end of the statement period will also attract

interest from the date of transaction.[8]

2.9

While the RBA advised that about 75 to 80 per cent

of credit card transactions do not accrue interest, about 65 per cent

of the total quantum of credit card debt (or, as noted above,

$33.1 billion) is accruing interest. To clarify, interest paying

cardholders 'account for about 30–40 per cent of accounts, about 20–25 per cent

of transactions, but close to two-thirds of the outstanding stock of debt'.[9]

2.10

The RBA observed that the proportion of credit card debt balances

accruing interest has fallen from around 75 per cent to

65 per cent since 2012. Balances accruing interest have also fallen

in absolute terms since peaking in late 2011 (as shown in Figure 1). The RBA

suggested the decline 'possibly reflects a range of factors such as changes in

consumers' financial behaviour, government reforms that took effect in 2012

relating to repayments and limit increase arrangements, and possibly also the

effect of competition for balance-transfer offers'.[10]

Similarly, the CBA suggested the trend might be attributed to 'higher customer

repayment rates and aggressive zero per cent balance transfer

offers'.[11]

Figure 1: Balances outstanding on credit and charge cards

Source: Reserve Bank of

Australia, Submission 20, p. 15.

2.11

Credit card debt has also declined as a proportion of overall household

debt in the past decade, from about 4.5 per cent in 2001 to a little

below 3 per cent now. It is important to note that while the ratio of

household debt to income has remained relatively stable over this period, the

ratio of credit card debt to household debt has declined. The RBA observed that

this trend might reflect the increasing availability and use of mortgage offset

and redraw facilities (mortgage interest rates being lower than credit card

interest rates).[12]

2.12

While the use of credit cards grew strongly through the 1990s and early

2000s, since 2004–05 spending on debit cards has grown more strongly than on

credit cards.[13]

The RBA suggested that this trend:

...is likely mostly a reflection of broader macroeconomic

trends, as the period to the mid-2000s was one where the ratio of household

debt (especially for housing) to income grew significantly and where the

household saving rate was falling. By contrast, the period since the mid-2000s

has seen a broad stabilisation in the household debt ratio, a recovery in the

saving rate and more conservative trends in card use and debt.[14]

2.13

The ABA pointed to similar trends in how Australians were using their

credit cards. It noted that while the overall value of credit card transactions

is currently growing at around 4 to 5 per cent a year, over

the past decade repayments on credit cards, excluding interest, have exceeded

new transactions:

Over the year ending May 2015, repayments exceeded the value

of transactions by $8 billion; the value of transactions on credit cards was

$293 billion and repayments were $301 billion.[15]

2.14

Whereas the RBA referred to recent declines in the amount of credit card

debt accruing interest and the proportion of credit card debt to overall

household debt, a joint submission from the Financial Rights Legal Centre and

Consumer Action Law Centre highlighted higher levels of credit card

indebtedness in the past decade:

Australian credit card debt is continuing to grow rapidly, in

line with a huge growth in household debt. The majority of Australian

households now have a net credit card debt. Statistics released by the Reserve

Bank of Australia show that as at May 2015 there were 16 million credit cards

with outstanding balances of $51.2 billion. Almost 64% of outstanding balances,

or $32.6 billion, was accruing interest. This represents an incredible 47.3%

increase in balances accruing interest over the past 10 years. These statistics

correspond with the huge increase in household debt. Since March 1977, we have

seen the percentage of household debt to disposable income increase from nearly

40% to over 140%.[16]

'Revolvers' and 'transactors'

2.15

Industry and regulatory analysts commonly categorise cardholders as

'revolvers' and 'transactors'. Revolvers typically pay interest on their

balances (as they carry forward, or 'revolve', card balances over time),

whereas transactors typically pay off their balance in full and thereby avoid

paying interest on their balances. According to the RBA, revolvers are more

likely to hold lower-rate cards than transactors, and transactors are more

likely to hold higher-rate rewards cards.[17]

2.16

The RBA advised that the proportion of revolvers is higher among

low-income households and when high-income households do fall into the revolver

category, they are more likely to be 'occasional revolvers' as opposed to

'persistent revolvers'.[18]

2.17

Drawing on data from the household, income and labour dynamics survey in

Australia (HILDA), Treasury also noted that low-income households have more

credit card debt relative to their incomes and pay more in credit card interest

relative to their incomes than high-income households (although higher income

households pay more interest in absolute terms). HILDA data similarly shows

that low net worth households pay higher proportions of interest relative to

their income.[19]

Summarising the data in its submission, Treasury advised that low income

households:

...would be more likely to be paying the high interest rates

charged on credit cards and be more likely to be subject to high additional

fees and charges. In particular, they will be more affected by the practice of

backdating interest charges when cardholders fail to pay off their full balance

at the end of each billing cycle.[20]

2.18

The committee also received evidence suggesting that people on low

incomes, including many disadvantaged and vulnerable people, are more likely to

use credit cards for cash advances.[21]

In addition to generally being subject to specific fees, cash advances are not

eligible for any interest free period and typically attract an even higher rate

of interest than the ongoing purchase rate on a credit card.

2.19

The RBA's 2013 Consumer Use Survey showed that

73 per cent of cardholders participating in the survey typically pay

off their account in full within the interest free period, implying that

27 per cent typically do not. Industry estimates suggest the

proportion of cardholders who typically pay interest is slightly higher, at

between 30 and 40 per cent. The RBA ventured that the gap

between its survey results and industry data may reflect hoped-for, rather than

actual behaviour on the part of consumers.[22]

2.20

A similar point was made in a joint submission by the Consumer Action

Law Centre and Financial Rights Legal Centre. They referred to a recent ANZ

financial literacy survey which found that 65 per cent of cardholders

claimed they had always paid their main card balance in full over the last

12 months:

However, the proportion of credit card balances accruing

interest indicates this figure is overly optimistic. A significant number of

consumers are actually 'revolvers': consumers who pay minimum monthly

repayments or a fraction of the outstanding balance and incur high interest

rate charges—around two thirds of outstanding balances actually attract

interest. This tendency towards identifying oneself as a transactor, when in

fact you are a revolver, is a basic behavioural bias. Consumers tend to

underestimate or are blind to factors that can impede repayment of their credit

card balances. People are overly optimistic and have other biases in assessing

risk, meaning they are overconfident when it comes to estimating the amount of

debt they will incur.[23]

Providers of credit cards

2.21

As noted above, there are currently over 80 institutions offering more

than 250 credit card products in Australia. CANSTAR data provided to the

committee by Westpac showed that of the 83 institutions offering credit cards

in July 2015, 30 were banks, 45 were credit unions and building societies and 8

were not Authorised Deposit-taking Institutions

(ADIs).[24]

The number of providers operating in the market obscures the fact that the

Australian credit card market is dominated by banks, and in particular the four

'majors' (the CBA, Westpac, ANZ and NAB, and their subsidiaries). The ABA

informed the committee that banks provide approximately 88 per cent

of credit cards on issue in Australia, and account for approximately

81 per cent of balances outstanding.[25]

The four majors alone account for about 68 per cent of balances

outstanding.[26]

2.22

As Treasury noted, while the four major banks' share of the credit card

market is high, this reflects the 'concentration of the Australian banking

system more generally rather than being a unique feature of the credit card

market'.[27]

It can also be noted that the majors' 68 per cent share of balances

outstanding has fallen slightly over the past decade (from around

74 per cent in 2004, although it has increased from about 66 per

cent immediately prior to the GFC) and is lower than the major banks' share of

household deposits, which stands at just over 81 per cent.[28]

2.23

It is also important to state that neither Visa nor MasterCard, the two

most widely used credit card brands, actually issue any credit cards

themselves. Rather, they are both operators of payment networks that are

utilised by banks and other providers of credit cards. As such, Visa and

MasterCard do not have any role in determining credit card interest rates (or

indeed any other aspect of credit card pricing), and do not receive any revenue

from interest payments.[29]

Credit card interest rates and spreads: variations and trends

2.24

The persistence of high interest rates in the credit card market,

despite a falling RBA cash rate, has been an important focus of this inquiry.

While the issue is explored in detail in chapter three, some general contextual

information regarding credit card interest rates is offered below.

2.25

Interest charged on credit cards varies widely depending on the type of

card and provider. According to an August 2015 search of comparison website

Mozo, there is a 15.5 per cent gap between the lowest rate card, a

Quay Credit Union Visa Credit Card with an ongoing purchase rate of

7.99 per cent, and the highest rate card, a GE Money MasterCard

at 23.5 per cent.[30]

2.26

While there are a range of credit cards available offering a variety of

rate features and pricing structures, cards on issue can be broadly categorised

as either 'low-rate', 'low-fee' or 'rewards'. With respect to interest rates,

the RBA maintains and publishes two data series: one on 'standard' cards, a category

that most reward and many low-fee cards fall into, and which commenced in

January 1990; and the other on low-rate cards, commencing in November 2003.[31]

The RBA explained in its submission that while there is a wide variation in the

advertised interest rates for credit cards, standard cards currently tend to

bunch around the 20 per cent mark, while lower-rate cards bunch

around 13 per cent.[32]

2.27

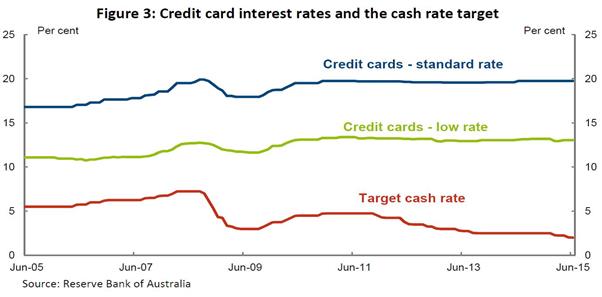

As Treasury confirmed in its submission, while the RBA cash rate has

declined by 2.75 percentage points since late 2011, credit card interest rates

have remained essentially unchanged over the same period (see Figure 2).[33]

According to consumer advocacy group CHOICE, if credit card rates had moved at

the same rate as the cash rate over that period, Australian credit card holders

would have paid $2.07 billion less in interest since mid-2011.[34]

Figure 2: Credit card

interest rates and the cash rate target

Source: Treasury, Submission

17, p. 3.

2.28

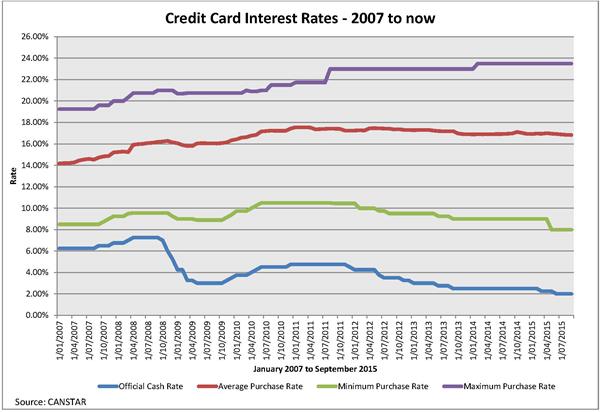

A document tabled by CANSTAR also shows that the gap between credit card

interest rates and the RBA cash rate has grown considerably since 2007,

although the gap has grown rather more slowly in the post-GFC environment.

CANSTAR's document tracked the gap since 2007 between the official cash rate

and three other measures of credit card interest rates: the average purchase

rate, the minimum purchase rate, and the maximum purchase rate. The gap between

the cash rate and each of these three measures has, according to CANSTAR's

document, grown since 2007 (see Figure 3). As CANSTAR explained, whereas the

gap between the average credit card purchase rate and the cash rate was

8 per cent in 2007, it currently stands at about

15 per cent. This was, CANSTAR suggested, 'an extraordinary

blow-out'.[35]

Figure 3: CANSTAR data on

credit card interest rates

Source: Documents tabled by

CANSTAR at a public hearing held in Canberra on 22 September 2015.

2.29

The growth in the gap between the cash rate and headline credit card

interest rates appears even more pronounced when annual fees are added to the interest

rate. Mr Ross Greenwood, the Nine Network's Business and Finance Editor,

tabled a document that annualised average fees into average credit card rates

from a range of providers to a card with a $5000 balance. Using this approach,

Mr Greenwood assessed the gap between the adjusted interest rate (the

interest rate with the annual fee annualised into it) and the RBA cash rate. Mr

Greenwood found that for cards provided by the major banks the gap had in

effect blown out to between around 17 and 20 per cent (and

higher still for Amex and Citibank). This compared, according to

Mr Greenwood's analysis, to a gap for the same banks' card offerings that,

using the same measure, was consistently around the 12 per cent mark

in 1998.[36]

2.30

It should be noted that average advertised interest rates do not fully

reflect trends in interest actually paid by cardholders, at least in aggregate

terms. Advertised rates do not, for instance, capture the effect of interest

free periods or low or zero-interest balance transfer offers. According to the

RBA, the effective interest rate received by the major banks on their entire

credit card portfolios—actual interest earned as a proportion of balances

outstanding—has fallen about 2 per cent since mid-2011, and is currently

11.6 per cent.[37]

As noted above, since the current easing cycle began in late 2011, the cash

rate has fallen from 4.75 per cent to 2 per cent, suggesting

that it has fallen a little more than effective interest rates on credit cards

over the same period, but not dramatically so.

2.31

In seeking to understand interest rate spreads,[38]

it is also useful to look at the gap between effective interest rates and the

weighted average of the interest rates paid on banks' sources of funds, as

opposed to the gap between effective interest rates and the RBA cash rate.

While funding costs have moved roughly in line with the RBA cash rate since the

current easing cycle began, Treasury pointed out that funding costs 'have risen

relative to the target cash rate since the financial crisis as banks switched

to a greater proportion of (more expensive) deposit funding'.[39]

Treasury presented a comparison of funding costs and effective credit card

interest rates since 2007 for the major banks (see Figure 4).

2.32

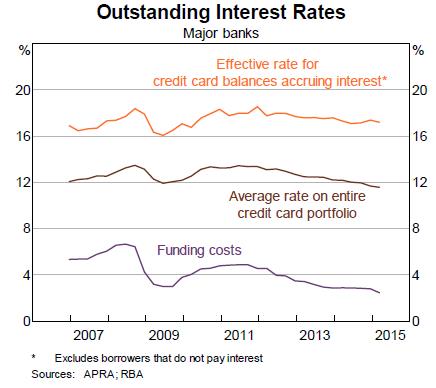

The abovementioned average effective interest rate of

11.6 per cent takes account of the banks' entire book of credit card

loans, including debt that does not yield interest. The effective rate for

cardholders who do pay interest ('revolvers') is around

17 per cent, which is down about 1 per cent since 2011 (see

Figure 4). The RBA concluded:

Taken together, the recent changes in these two series [for

the effective rate for credit card balances accruing interest, and the average

rate on entire card portfolios] are consistent with the observed decline in the

proportion of the stock of debt that is accruing interest (either reflecting

more consumers paying down debt ahead of being charged interest, or reflecting

an increase in the take up of zero and lower-rate balance transfers) and also

some switching by consumers from high- to lower-rate cards.[40]

Figure 4: Interest rates on

outstanding credit card balances

Source:

Reserve Bank of Australia, Submission 20, p. 18.

2.33

Even if effective interest rates have trended down over the current

easing cycle, it is apparent that the spread between bank funding costs and

effective interest rates has grown significantly since the GFC. In the years

prior to the GFC, the spread was on average 6.7 per cent, and did not

vary much from this mark; since the GFC, the spread has been on average

8.7 per cent, and again that spread has not varied greatly in the post-GFC

period (see Figure 5).

Figure 5: Spread between

credit card 'effective' interest rates and bank funding costs

Source: Treasury, Submission 17, p. 3.

2.34

In its submission, the RBA provided an even more differentiated and

detailed picture of trends in interest spreads to funding costs. It showed that

while the spread between funding costs and effective credit card interest rates

on balances outstanding is currently about 9 per cent, the spread for

cardholders paying interest is about 14.75 per cent (see Figure 6).

Figure 6: Various interest

spreads to funding costs

Source: Reserve Bank of

Australia, Submission 20, p. 19.

2.35

The reasons for the apparent decline in the effective interest rate on

credit card portfolios, and trends in the spread between the cash rate and

credit card interest rates (both headline and effective), are explored in chapter

three.

2.36

It is important to emphasise at this point that funding costs are only

one component of credit card costs. Indeed, as discussed in the next chapter,

the major banks advised the committee that funding costs constituted less than

25 per cent of the cost base of providing credit cards. Other costs,

they noted, include but are not limited to credit management and costs

associated with fraud and fraud protection, rewards and product benefits,

insurances and concierge services, technology and systems costs, and innovation

and product development. Card providers also stressed that credit card lending

has a higher risk profile than secured forms of lending, and this higher risk

is priced into credit cards. The relative importance of these various costs in

informing credit card interest rates is considered in chapter three.

Australian credit card interest rates: international comparisons

2.37

Several witnesses told the committee that trends in interest rate

settings on Australian credit cards were not dissimilar to trends in comparable

markets overseas. For example, the ABA argued that comparisons with the United

States and United Kingdom 'suggest the dynamics for interest rates on credit

cards in Australia are not out of line with international developments'.[41]

Similarly, the RBA noted that high-rate cards are not uncommon overseas, and

that it was likely 'some of the same forces are at work' in those markets as in

the Australian market.[42]

2.38

The CBA also told the committee that the spread between the cash rate

and credit card interest rates was not unusual by international standards. It

further suggested that card providers internationally, like the CBA, also

accounted for economic risk in pricing their products:

If you look at international experience, in the UK you will

find credit card rates ranging from about seven to 30 per cent and in the US

probably in the range of 11 to 30 per cent, despite their cash rates being

effectively at zero. That supports the fact that credit card providers, not

just domestically but internationally, are very cognisant of pricing for risk.

Those markets have demonstrated that losses can be substantial in any given

year, and our role is to price competitively and appropriately through the

cycle.[43]

2.39

However, Professor Abbas Valadkhani claimed that the gap between

the cash rate and credit card rates was substantially wider in Australia than

in the United States and United Kingdom. He asserted that if credit card spreads

in Australia were like those in the United States, Australians would be

somewhere in the order of $840 million better off; and if spreads were the

same as those in the UK market, Australians would be $2.2 billion better

off.[44]

Responsible lending obligations for credit card providers

2.40

The National Consumer Credit Protection Act 2009 (National Credit

Act) sets out responsible lending obligations which apply to all forms of

regulated credit, including credit cards. ASIC has

responsibility under the Act for administering the obligations.[45]

2.41

The responsible lending obligations require credit licensees to do

certain things before providing a credit card to a consumer or increasing a

cardholder's credit limit. As ASIC explained, these processes include making

reasonable inquiries about a consumer's requirements and financial situation,

taking reasonable steps to verify the consumer's financial situation, and

making an assessment as to whether a credit contract is 'not unsuitable' for a

consumer based on inquiries made.[46]

2.42

As ASIC noted, its primary guidance on responsible lending, including in

relation to credit cards, is set out in Regulatory Guide 209, Credit

licensing: Responsible lending conduct (RG 209). RG 209 also

provides guidance to credit licensees on ASIC's interpretation of the

responsible lending obligations.[47]

2.43

ASIC also administers obligations that are specific to credit cards and

were introduced by the National Consumer Credit Protection Amendment (Home

Loans and Credit Cards) Act 2011 and associated regulations. These

obligations are as follows:

-

a requirement for card providers to send a 'key facts sheet' to

new card applicants, setting out how minimum repayments are calculated,

interest rates that apply, and interest-free periods and fees;

-

a prohibition on unsolicited offers to increase card limits;

-

restrictions on the ability of providers to charge fees or higher

interest rates when a cardholder exceeds their credit limit;

-

a requirement that repayments on credit cards must first be

allocated towards those portions of a balance to which the highest interest

rate applies (this applies to cards issued after 1 July 2012); and

-

the inclusion of a minimum repayment warning on monthly credit

card statements, highlighting the length of time it would take a cardholder to

repay their balance if they only made the minimum payment.[48]

Understanding the impact of high credit card interest rates

2.44

The foregoing discussion about statistical trends in credit card

interest rates should not obscure the very real and troubling effects that high

credit card interest rates can have on individuals, families and communities.

The committee received a large amount of evidence on these effects which has

played an important role in informing the committee's thinking about credit

card interest rates and the credit card market more generally.

2.45

The Consumer Action Law Centre and Financial Rights Legal Centre

observed that credit card debt can have 'serious and profound impacts':

For those with the most acute problems with credit card debt,

the debt seriously harms their lives. It can cause, amongst other things,

family breakdown, violence, crime and deterioration in health (including mental

health). Significant credit card indebtedness can also have a long-term impact

on the capacity to provide for housing, health, education and retirement.[49]

2.46

The St Vincent de Paul Society advised the committee that it worked with

people every day who in their struggles to manage out-of-control credit card

debts had resorted to:

...borrowing money, selling items of value, taking out

short-term pay day loans, and seeking the assistance of welfare services in

addition to increasing the limit or taking out new credit cards when the offer

is made available.[50]

2.47

A number of organisations relayed personal stories of hardship resulting

from high-interest credit card debt. Good Shepherd Australia New Zealand told

how one of their clients had not only been a victim of domestic violence but

also financial abuse, and had incurred a large credit card debt as a result.[51]

The WA Consumer Credit Legal Service referred to a number of cases it had dealt

with where, as a result of mental illness, family breakdown or other crises, a

vulnerable individual had amassed a credit card debt that they had no prospect

of ever repaying.[52]

Financial Counselling Australia (FCA) provided a number of examples which

showed that people of all ages and from all walks of life could become trapped

by credit card debt. For example, FCA told how a woman in her 30s had accrued a

long-term credit card debt and now felt 'trapped, and unable to move forward

with any financial plans until she had repaid this debt'. The FCA also

explained how a 75 year old pensioner had used his credit card to supplement

his income and avoid homelessness, but in the process had built a credit card

debt so large that he struggled simply to pay the interest.[53]

2.48

Chapter five provides a detailed analysis of the problem of long-term

credit card debt, and sets out some options for helping people avoid the credit

card debt trap and, when that fails, better assisting people experiencing

financial hardship. In addition, reference is made throughout this report to

how the credit card market is currently failing vulnerable and disadvantaged

Australians. In part, this story is told in statistics and headline figures,

including those set out earlier in this chapter. However, it needs to be

emphasised that the committee's concern in this regard has been largely

informed by the compelling and troubling evidence it received of individuals

and families struggling under the weight of high-interest credit card debt.

Navigation: Previous Page | Contents | Next Page