Chapter 4

Impact of the stimulus packages

Australia outperforms

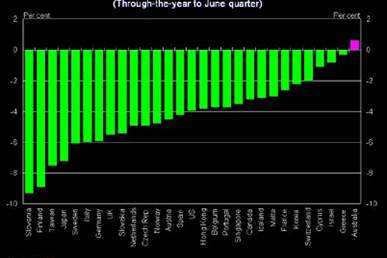

4.1

Australia is the only advanced economy in which real GDP in the June

quarter of 2009 was higher than in the June quarter of 2008 (Chart 4.1).

Chart 4.1: Real

GDP growth rates

Source: Dr Ken Henry,

Treasury, speech to Australian Institute of Company Directors,

23 September 2009.

4.2

This is clearly an impressive performance by Australia. It is not clear

to what extent this is attributable to the stimulus packages, or the legacy of

prior sound economic management, or the relative contributions of these or

other factors.

Australia was in a singularly strong position before the crisis

4.3

Australia was in a stronger position before the crisis than were most

comparable countries. Treasury note:

An additional factor that is likely to have contributed to

Australia's resilience during the crisis is the structural reforms to

financial, labour and product markets undertaken over recent decades. These

structural reforms have lifted the economy's productive capacity and improved

the flexibility and speed with which both firms and individuals respond to both

positive and negative economic shocks. The resilience of the Australian financial

system to the Global Financial Crisis illustrates this point. Macroeconomic

stability also reinforces the economy's structural flexibility and efficiency

by providing businesses and households with more certainty in making their

decisions.[1]

4.4

The Governor of the Reserve Bank cited three reasons why Australia's

performance has been better than that in other OECD economies:

Firstly, our financial system was in better shape to begin

with...Secondly, some key trading partners for Australia have proven to be relatively

resilient in this episode...Finally, Australia had ample scope for macroeconomic

policy action to support demand as global economic conditions rapidly

deteriorated, and that scope was used. The Commonwealth budget was in surplus

and there was no debt, which meant that expansionary fiscal measures could be

afforded. In addition, monetary policy could be eased significantly without

taking interest rates to zero or engaging in the highly unconventional policies

that have been needed in a number of other countries.[2]

4.5

Elaborating on these points, Australia was well prepared to face an

external shock as its financial system was sounder. This is particularly

significant given that the current crisis had its source in the financial

sector. In a number of countries large banks have had to be 'rescued' by

governments injecting equity, making emergency loans or even (temporarily)

nationalising them. By contrast, none of these measures have been necessary in

Australia. The four major Australian banks now constitute four of only nine

among the world's largest 100 banks which are rated AA or better.[3]

4.6

Australia was also supported by the important role played by its mineral

exports. A large proportion of these go to China, whose economy continues to be

the strongest growing in the world. This is partly a fortunate accident of

geography: the tyranny of distance has become the blessing of propinquity. But

it also reflects diplomatic efforts by previous Australian governments to

develop trade ties with China, particularly in the minerals sector. China is

now the major purchaser of Australian iron ore and coal, particularly in

Western Australia. In the earlier part of 2009 the level of Chinese imports of

iron ore and coal increased significantly which in turn provided a boost to the

Australian economy which made an important contribution to preventing this

country going into a technical recession.

4.7

Another important difference between Australia and most other OECD

countries has been the greater fiscal discipline exercised here. Like the

average OECD economy, Australia had a significant budget deficit during the

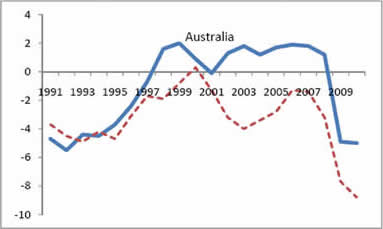

early 1990s recession. But unlike many other countries, Australia moved back

into surplus as the economy recovered and maintained a surplus for most years

until the current downturn (Chart 4.2).

4.8

This fiscal prudence meant that Australia entered the financial crisis

with a much smaller government debt than most other countries (Table 4.1).

Chart 4.2: General

Government Financial Balances: Australia vs OECD

(1991-2010; per

cent to GDP)

Source: Secretariat, based on

data in OECD Economic Outlook, June 2009.

4.9

Chart 4.2 shows that economic management over the last decade set

Australia apart with the capacity to afford a stimulus – leaving aside

the question of its efficacy or desirability – giving Australia the "ample

scope" for fiscal action referred to by the RBA Governor in his opening

statement to the committee.[4]

The chart also illustrates the magnitude of the impact of the Rudd government's

fiscal spending on Australia's financial position compared with the OECD

average.

Table 4.1: General

government financial liabilities

Per cent to GDP, 2008

|

|

gross |

net |

|

|

gross |

net |

|

Australia |

14 |

-7 |

|

Netherlands |

65 |

25 |

|

Austria |

66 |

33 |

|

New Zealand |

26 |

-16 |

|

Belgium |

93 |

74 |

|

Norway |

56 |

-125 |

|

Canada |

68 |

22 |

|

Sweden |

47 |

-14 |

|

France |

76 |

42 |

|

Switzerland |

46 |

10 |

|

Germany |

69 |

45 |

|

United Kingdom |

57 |

34 |

|

Japan |

172 |

84 |

|

United States |

71 |

48 |

Source: OECD Economic Outlook,

June 2009.

The impact of the fiscal stimulus in Australia

Overall impact

4.10

Treasury is the premier source of economic advice to the government of

the day and was the architect of the various spending initiatives outlined in

Table 2.2.

4.11

Treasury estimate that in the absence of the fiscal stimulus measures, rather

than recording modest growth, GDP would have instead fallen by 1.3 per cent through

the year to the June quarter 2009 (Chart 4.3).[5]

Chart 4.3: Australian

real GDP growth rate

Source: Dr Ken Henry,

Secretary, Treasury, speech to Australian Institute of Company Directors, 23 September

2009.

4.12

Elaborating to the Committee, the Treasury Secretary said:

Without this stimulus, we estimate that the economy would

have contracted not only in the December quarter of 2008 but also in the March

and June quarters of this year. Our estimates of these impacts are based on

internal modelling informed by studies of the effects of fiscal stimulus by the

International Monetary Fund, the OECD and a range of academic researchers. They

are corroborated by ABS data, by private sector surveys on how the stimulus was

spent and by an examination of the experience of countries that have not had

such a large stimulus in place.[6]

4.13

Asked about the relative contribution of fiscal and monetary policy,

Treasury opined:

...fiscal policy’s contribution to growth over that period has

been substantially larger than the contribution of monetary policy...[7]

4.14

The reasoning behind this conclusion was set out in Treasury's written

contribution:

The official (nominal) cash rate was reduced from 7.25 per

cent at the end of August 2008 to its current level of 3.00 per cent in April

2009,[8] a reduction of 4.25 percentage points...[as] underlying inflation fell by ¾ of a percentage point

between the September quarter 2008 and the June quarter 2009...[the] real

official cash rate has fallen by 3.50 percentage points...However, bank lending

rates have fallen by less than the reduction in the official cash rate...about 2½ percentage points. Using

the findings of Gruen, and Naveen[9],

a 2½ percentage

point reduction in the real interest rate would contribute 0.85 per cent to GDP

in the first year. However, the majority of the cash rate reductions occurred

less than a year ago.[10]

4.15

This analysis may, however, have underestimated the contribution of

monetary policy to GDP growth. It is not real rates which matter to households

but rather the change in their nominal household disposable income resulting from

changes in nominal interest rates. These effects were very large. For example,

a 3 per cent reduction in nominal interest rates on outstanding household debt

of $1.3 trn (including households and unincorporated enterprises) increases

household income by $39 bn each year, and that is about 3 per cent of GDP in a

year.

4.16

As can be appreciated this is a very significant impact of monetary

policy on potential consumer spending and thereby business confidence. Arguably

the reduction of interest rates (monetary policy) had a much greater impact

than the cash contributions provided by the government in the so-called

"$10bn cash splash".

4.17

The Committee would be interested in the outcome of Treasury analysis of

the relative contributions of monetary policy compared to fiscal policy in

stimulating consumer spending and business confidence,

4.18

The underlying strengths of the Australian economy particularly the level

of government debt and the strength of the banking system which as has been

stated elsewhere includes four of the 9 AA- or better rated banks in the world's

largest 100 banks.

4.19

Another undoubted factor in preventing the Australian economy going into

recession was the rebound in the Chinese economy leading to China substantially

increasing purchases of Australian iron ore and coal.

4.20

When asked by Senator Eggleston what would have been the consequences

for the Australian economy if the China factor had not been in play, Glenn

Stevens, Governor of the RBA, replied that other measures would have been

taken. The form of such other measures was not identified by the Governor.

The impact of the cash payments

4.21

There was debate over whether the cash payments were spent or saved and

this was relevant to the extent that they acted to stimulate demand. One

approach to assessing the efficacy of the cash payments was to examine retail

sales data to see whether there appears to have been an associated increase:

An analysis undertaken by Tony Meer of Deutsche Bank—and

reported at Peter Martin’s blog and then in The Age—tends to suggest

that retail sales were far in excess of what we might otherwise have thought.

But Ashton and I have undertaken an analysis of the retail sales, and our

argument is that, simply by extending the ABS trend data—which they stopped

doing in November last year—and putting in another very commonly used trend

figure, retail sales trends are not unusual at the moment and retail sales are

at about trend.[11]

...we undertook a forecasting exercise and we imagined that we

were back in May 2008...and tried to forecast retail sales... by and large, the

actual retail sales is within a 95 per cent confidence band of what we would

have expected in May last year—which again suggests to us that retail sales are

not that unusually different from what they might otherwise have been if we

could forecast this from almost over a year ago.[12]

4.22

The Reserve Bank regards the stimulus package as having supported

demand:

If the intention was to support demand in the economy... my

conclusion would be that those measures have supported demand quite materially

over the last... nine or 10 months.[13]

4.23

A similar view was expressed by the business community:

With the rationale that government spending be provided to

promote stimulus in the economy, we considered it should initially be provided

to households to promote private spending...Support to households has bolstered

retail spending, and this evidence has been recorded amongst our retail members

and those in the hospitality and restaurant-cafe sector.[14]

4.24

Clearly this is the case. Much of it was spent. The real question is

whether the level of support justified the cost and represented best value for

money.

Eligibility

4.25

Some argued that the cash payments could be more equitably and

efficiently targeted:

In terms of equity, I think that we could, should and still

can do more to help those who are most adversely affected by a slowdown in the

economy—that is, of course, the unemployed and those people who share a house

with the unemployed. It was an unfortunate irony that the unemployed did not

receive the $900 bonus payment. I think that providing money to unemployed

people directly is likely to have a very positive stimulatory effect not just

on the national economy but on the local economy in which those people live.

There is no better way to target money towards the regions that are

experiencing the most unemployment than to provide increased payments to those

who are unemployed.[15]

The impact of the infrastructure

spending

4.26

Accepting for the sake of argument that stimulus spending is an

efficient and effective use of resources – and the committee notes there was credible

opinion contrary to this view – it makes sense at least to have a mix of types of

stimulus, and it needs to be noted that there have been several examples of

inflexibility and waste in the application of the fiscal stimulus packages:

Certainly the standard wisdom on fiscal stimuluses is that

you get a smaller multiplier from household handouts but you can do them

quickly. You want a mix of quick, less effective household handouts and slower

but possibly higher multipliers through infrastructure spending.[16]

In terms of the formulation, there may not have been a more

sensible package...There was the cash splash designed to support the household

sector ASAP. Then there was the idea of supporting economic activity more

generally...Then there are some of the longer term projects. To me that make

sense...I think most financial market economists...would think the package was

reasonably well structured given the economic circumstances.[17]

4.27

There has been differing views about the infrastructure spending:

Analysis of the efficiency of how the money is being spent

needs to be undertaken from the perspective that the primary objective was to

spend money quickly. The purpose of the stimulus package was to stimulate the

economy. That must be the primary criteria against which it is judged. Of

course, the more we can achieve along the way with the expenditure of that

money the better. But the objective was to spend a large amount of money

quickly, not to spend money perfectly in a drawn out fashion.[18]

4.28

Business is more supportive, at least in respect of some of the

infrastructure spend:

... But we have some confidence that there will be expansions

of capacity that will come from some of the investments in infrastructure...[19]

That would increase productivity, yes.[20]

The effects on business and consumer confidence

4.29

Both business and consumer confidence has picked up since late 2008, as

shown by the RBA compilation of consumer and business sentiment in Chart 4.4.

Chart 4.4:

Sentiment indicators

Source: Reserve Bank of Australia, Statement of

Monetary Policy, August 2009, p 35.

4.30

The Committee heard evidence that the business community would have

responded with even more vigour to alternative measures directed to the

business community:

Had they gone down the road of, say, finding ways to reduce

taxes—payroll taxes and other kinds of taxes related to business—which would

have a direct effect on business profitability and on cash flow then the

reaction within the business community would have been a lot stronger. Not only

would employment have been protected in the way that the stimulus was intended

but it would be much more general. In fact, a higher profitability for business

and higher cash flows would actually have led to, I believe, an actual

improvement in the level of economic activity relative to what we have seen

here.[21]

4.31

There was a compelling argument that the stimulus has led to a degree of

unproductive, even counterproductive, investment through the creation of

artificial supply chains:

On the second issue, of structural balance: what I mean here

is that, if we are going to have recovery, that recovery will come through

private-sector businesses again generating their own growth. The important

thing here is that the supply chains are related, so you not only will have

growth in final demand at some level but the actual supply chains within the

economy that are feedstock into those businesses will also be growing.

Having the kinds of structural imbalances that the stimulus

has—which mean that, ultimately, it will have to be wound back; you cannot

continue with these forms of expenditure—means that all the structural aspects

that go into these expenditures will also have to be wound back. Had we instead

opted for an approach that went towards raising the profitability of private‑sector

businesses, then the actual structures that we put in place, the supply chains,

would themselves have been productive because they would have been feeding into

the ability of firms to actually produce what other people are willing to buy.

In that way, rather than being a structure that has to be wound back as the

stimulus is withdrawn, this would have been a structure that would have become

a permanent feature of the Australian economy and contributed to growth.[22]

4.32

In the absence of fiscal stimulus, the Reserve Bank of Australia would

have responded by further lowering interest rates and would have had the

capacity to do so. As a result, the exchange rate would also have been lower.

Effects of higher national debt and implications for future taxation and

long bond yields

4.33

The fiscal stimulus packages will obviously add to government debt.

However, the bulk of evidence is that prudent fiscal policy in the decade

before the crisis means that government debt will remain manageable. The

Committee does note, however, that there are consequences attached to the

payment of this debt, such as the wiping out of the surplus, higher taxation and

higher interest rates. At best, it will take 10 years to pay the entire debt

off, and at worst, decades... was this really necessary? The Committee believes

that there are opportunities to minimise some of these consequences if the

fiscal stimulus packages were recalibrated.

4.34

This tax burden that will be necessary to repay the debt incurred as a

result of the stimulus package was acknowledged by the Treasury Secretary and

other witnesses:

Of course the stimulus that is being provided at the moment,

to the extent that it is debt financed, will have to be repaid in the future.

That means that at some stage in the future either government spending will be

lower than it otherwise would have been or tax settings will be higher than

they otherwise would have been. But that future time will be a period of faster

growth in private sector activity and the judgement has been made that in those

circumstances where the private sector is growing much faster than it is at the

moment the government will have the ability to repay debt without doing damage

to gross domestic product growth.[23]

...it is inevitable that these payments have to be paid for in

some sense, but how the fiscal tightening is done is a matter entirely for

policy. You could do it through expenditure cuts or tax increases... An

inevitable impact of Keynesian fiscal policy is that if you inject money into

the economy in bad times then you are going to have to get it back in good

times.[24]

The raising of taxation to pay interest on and repay debt

will reduce to some extent the productive capacity of the economy. For moderate

amounts of debt this is likely to be small in comparison with the waste of

productive resources through unemployment.[25]

4.35

The actual cost of raising taxation to meet the debt will depend on the

quantitative effect of the 'dead weight loss' arising from taxation (which is a

reflection of the extent to which it discourages economic activity). There is debate

about the size of this effect:

People estimate between 20 and 80 per cent for a deadweight

cost...[26]

To those who are terrified of tax rates destroying incentive,

there are plenty of ways to increase tax revenue in a way that would minimise

that. The first would be to abolish the enormous range of tax concessions that

currently exist—the 50 per cent capital gains tax concession or the enormous

concessions on superannuation. If the actual income tax rate for high‑income

earners were increased, there is virtually no chance that rich people will

decide to be poor because the tax rate is just too high for them...If the

parliament wants to increase taxes, it should, and the economic effects of

doing it wisely would be low.[27]

...taxes do distort economic activity. Those tax driven

distortions either reduce the size of the economy below the size that it would

otherwise be or in other ways impose welfare losses on citizens. That is

generally the case. It is certainly not the case always, and as you would be

aware, Senator, it is not the case if the tax is being used, for example, to

correct for an environmental externality—and there are a large number of other

interesting cases in which taxes that raise revenue actually turn out to be

welfare enhancing rather than welfare detracting. But as a general point it is

true. What is also true—and this is the reason why people get interested in tax

policy—is that different taxes have different effects.[28]

4.36

There are varying views about the impact of higher (prospective)

government debt on the interest rate that needs to be paid on that debt. The

Reserve Bank does not see this impact as significant, but their words sound a

note of warning about the global impact of government debt on borrowing costs,

and hence the risks for Australia:

I do not think that, at the moment, it is easy to discern

much impact here. The long range in Australia is between five and 5½ per cent,

which is about normal. It has been around that, on average, for the last

decade. For a country like Australia, what we are talking about in government

long-run borrowing costs is that there is a global rate which, roughly

speaking, is the US Treasury rate, and we will be paying above or below a

little margin, depending on our individual soundness. If we find that

government borrowing rates are a lot higher in the years ahead, I do not think

it will be because of Australia’s outcomes. It will be because there is a lot

of government debt being issued around the world by countries that have really

serious fiscal problems, like the Americans and the British...[29]

4.37

The Australian Office of Financial Management put more emphasis on

domestic influences:

In particular, the relative strength of the economy and the

expectations about inflation and exchange rates can have an impact.[30]

4.38

It also described a countervailing influence on long bond yields,

referring to the:

...changed attitude to risk on the part of many investors which

has led to a flight to quality and safety. So there has been an increased

availability of funds for investment in government debt. While governments have

had a very much increased volume of borrowing, that has been able to be

satisfied by an increase flow of funds into the sector.[31]

Assessing the stimulus package with models

4.39

A perennial problem in macroeconomics is that there are no controlled

experiments. We cannot take two identical economies and subject just one of

them to a stimulus package. There is always room for debate about how the

economy would have evolved in the absence of a stimulus package. As the

Treasury Secretary remarked:

...we will never know the precise impacts of the fiscal

stimulus on the economy.[32]

4.40

It should be noted that there are no absolutes in any of this modelling,

and it will never be known the precise impact of each element of the fiscal

stimulus package, and therefore claims about jobs saved need to be considered

against that background.

4.41

One approach is to use a macro-econometric model to address these 'what

if" questions. But confidence in the results will depend on confidence in

the model used. More usual is to use economy-wide models, a range of

single-equation studies and other sources such as surveys and business liaison

to form a view about the impact of alternative policies.

4.42

The Committee asked Treasury for more information about their

calculations on the impact on employment of the stimulus package. Treasury

explained that they first calculated the impact on real GDP:

Taking the dollar amount of spending in the fiscal stimulus

package, we then make adjustments for behavioural responses by households and

businesses. For one-off transfer payments to households, we assume the spending

propensity to be 0.7 in the forecast period. The remaining amount of the

transfer payments is assumed to be saved by households, at least over the

forecast horizon. In contrast, for direct government spending, the spending

propensity is assumed to be 1...the next step is to...apply an import share of

0.15...This gives us direct (or first round) fiscal multipliers to GDP of 0.6 for

transfer payments and 0.85 for direct government spending...To estimate the

effects on real GDP, we adjust the nominal spending numbers for inflation...[33]

4.43

The impact of the stimulus as calculated in this way is subtracted from

the real GDP forecasts to give alternative 'pre-stimulus forecasts', shown in

Table 4.2, and illustrated by Chart 4.3 above.

Table 4.2: Treasury

forecasts of real GDP with and without stimulus

(annual percentage

change)

|

|

2008-09

|

2009-10

|

2010-11

|

|

Pre-stimulus

|

-0.9

|

-2.0

|

3.4

|

|

Contribution of stimulus

|

1.0

|

1.6

|

-1.2

|

|

Post-stimulus

|

0.1

|

-0.4

|

2.1

|

Source: Treasury briefing

paper, p 4.

4.44

Treasury then calculated the employment impact:

The modelling work suggests...a 1 per cent increase in GDP

leads to a ¾ per

cent increase in employment over time...The peak impact of the stimulus packages

estimated at Budget was the addition of 210,000 jobs and the level of

employment remains higher through to the end of the forecast period...The peak

unemployment rate was estimated to be 1½ per cent lower as a result of the fiscal stimulus.[34]

4.45

Dr Kates is very sceptical about Treasury's modelling showing the

stimulus package having a significant impact:

...the Keynesian model cannot be used to demonstrate that a

Keynesian stimulus has a positive effect on the economy.[35]

4.46

Dr Kates states that in the absence of the stimulus package the

unemployment rate would have been 0.3 percentage points higher. This represents

34,000 people. On this basis he concludes that, given a $43 billion cost for

the stimulus package, it has cost over a million dollars per job saved.[36]

Other estimates of the employment impact of the package are much higher. As

noted above, Treasury puts it at over 200,000 jobs. This would imply the cost

per job saved is much less than this. (Furthermore, such calculations ignore

the additional taxation paid by those in work and the savings from lower

unemployment benefits. It also assumes the spending brings no other benefits

than creating jobs.)

4.47

Professor McKibbin, noted economist and member of the Reserve Bank Board,

submitted the results of his global modelling using the G-cubed model.

This suggested that the global fiscal stimulus would increase real GDP in all

countries in the first year, but higher real interest rates would then moderate

the impact.[37]

His modelling led him to argue for a fiscal stimulus in Australia about half as

large as that proposed by the Government.[38]

Navigation: Previous Page | Contents | Next Page