Chapter 2

Overview and recent developments

What is digital currency?

2.1

In its 2014 report on virtual currencies, the Financial Action Task

Force (FATF), an inter-governmental body established in 1989 by a Group of

Seven (G-7) Summit in Paris, defined digital currency as:

[A] digital representation of value that can be digitally

traded and functions as (1) a medium of exchange; and/or (2) a unit of account;

and/or (3) a store of value, but does not have legal tender status (i.e., when

tendered to a creditor, is a valid and legal offer of payment) in any

jurisdiction. It is not issued nor guaranteed by any jurisdiction, and fulfils

the above functions only by agreement within the community of users of the

virtual currency. Virtual currency is distinguished from fiat currency (a.k.a.

'real currency', 'real money', or 'national currency'), which is the coin and

paper money of a country that is designated as its legal tender; circulates;

and is customarily used and accepted as a medium of exchange in the issuing

country. It is distinct from e-money, which is a digital representation of fiat

currency used to electronically transfer value denominated in fiat currency.

E-money is a digital transfer mechanism for fiat currency—i.e., it

electronically transfers value that has legal tender status.[1]

2.2

The term 'digital currency' can sometimes have a broader meaning, which

also includes e-money.[2]

For the purposes of this report the terms 'digital currency' and 'virtual

currency' can be used interchangeably.[3]

Types of digital currency

2.3

Digital currency can be divided into two basic types: convertible and

non-convertible digital currency. Convertible digital currency has an

equivalent value in real (fiat) currency and can be exchanged back-and-forth

for real currency (Bitcoin is an example of convertible currency).

Non-convertible digital currency, on the other hand, cannot be exchanged for

fiat currency and is intended to be specific to a particular virtual domain or

world, such as a massively multiplayer online role-playing game, for example World

of Warcraft Gold is a non-convertible digital currency.[4]

2.4

Digital currency can be further categorised into two subtypes:

centralised and non-centralised. All non-convertible digital currencies are

centralised, as they are issued by a single administrating authority.

Convertible digital currencies can be either centralised or decentralised. Decentralised

digital currencies, also known as cryptocurrencies, are distributed,

open-source, math-based, peer-to-peer currencies that have no central

administrating authority and no central monitoring or oversight. Examples of

cryptocurrencies include: Bitcoin, Litecoin and Ripple.[5]

What is Bitcoin?

2.5

Launched in 2009, Bitcoin was the first decentralised convertible

digital currency and the first cryptocurrency. Bitcoin was created as an

electronic payment system that would allow two parties to transact directly

with each other over the internet without needing a trusted third party

intermediary.[6]

The 'distributed ledger' (also known as the 'block chain') is used to record

and verify transactions, allowing digital currency to be used as a

decentralised payment system.[7]

A simplified explanation of the process is as follows:

A user, wishing to make a payment, issues payment instructions

that are disseminated across the network of other users. Standard cryptographic

techniques make it possible for users to verify that the transaction is valid—that

the would-be payer owns the currency in question. Special users in the network,

known as 'miners', gather together blocks of transactions and compete to verify

them. In return for this service, miners that successfully verify a block of

transactions receive both an allocation of newly created currency and any transaction

fees offered by parties to the transactions under question.[8]

2.6

While Bitcoin is the most prominent digital currency, there are

currently more than five hundred different digital currencies, including Litecoin,

Ripple, Peercoin, Nxt, Dogecoin, Darkcoin, Namecoin, Mastercoin and BitcoinDark.[9]

Most of these alternative digital currencies were inspired by, or explicitly modelled

on, Bitcoin.[10]

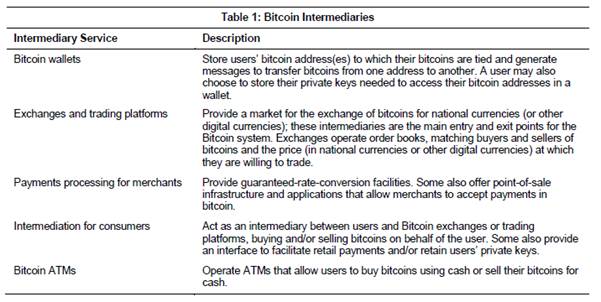

Digital currency intermediaries

2.7

Digital currency users may use intermediaries to manage their holdings

and facilitate transactions. For Bitcoin users, there is a range of

intermediaries which provide services to users.[11]

Current regulatory framework

Taxation

2.8

On 20 August 2014, the Australian Taxation Office (ATO) released a suite

of draft public rulings on the tax treatment of digital currencies. The ATO's

rulings, which were finalised on 17 December 2014, determined that:

Transacting with bitcoins is akin to a barter arrangement,

with similar tax consequences.

The ATO's view is that Bitcoin is neither money nor a foreign

currency, and the supply of bitcoin is not a financial supply for goods and

services tax (GST) purposes. Bitcoin is, however, an asset for capital gains

tax (CGT) purposes.[12]

2.9

The ATO's finalised public rulings are as follows:

-

GSTR 2014/3—Goods and services tax: the GST implications of

transactions involving Bitcoin

-

TD 2014/25—Income tax: is Bitcoin a 'foreign currency' for the

purposes of Division 775 of the Income Tax Assessment Act 1997?

-

TD 2014/26—Income tax: is Bitcoin a CGT asset for the purposes of

subsection 108-5(1) of the Income Tax Assessment Act 1997?

-

TD 2014/27—Income tax: is Bitcoin trading stock for the purposes

of subsection 70-10(1) of the Income Tax Assessment Act 1997?

-

TD 2014/28—Fringe benefits tax: is the provision of Bitcoin by an

employer to an employee in respect of their employment a fringe benefit for the

purposes of subsection 136(1) of the Fringe Benefits Tax Assessment Act 1986?[13]

2.10

A summary of the taxation implication of the ATO's rulings on digital

currencies is as follows:

-

Capital gains tax (CGT)—Those using digital currency for

investment or business purposes may be subject to CGT when they dispose of digital

currency, in the same way they would be for the disposal of shares or similar

CGT assets; individuals who make personal use of digital currency (for example

using digital currency to purchase items to buy a coffee) and where the cost of

the Bitcoin was less than AUD$10,000, will have no CGT obligations.

-

Goods and Services Tax (GST)—Individuals will be charged GST when

they buy digital currency, as with any other property. Businesses will charge

GST when they supply digital currency and be charged GST when they buy digital

currency.

-

Income Tax—Businesses providing an exchange service, buying and

selling digital currency, or mining Bitcoin, will pay income tax on the profits.

Businesses paid in Bitcoin will include the amount, valued in Australian

currency, in assessable business income. Those trading digital currencies for

profit, will also be required to include the profits as part of their

assessable income.

-

Fringe Benefits Tax (FBT)—remuneration paid in digital currency

will be subject to FBT where the employee has a valid salary sacrifice

arrangement, otherwise the usual salary and wage PAYG rules will apply.[14]

Taxation white paper process

2.11

On 30 March 2015, the Hon Joe Hockey MP, Treasurer, released a tax

discussion paper to inform the government's tax options Green Paper, due to be

released in the second half of 2015, with the White Paper to be released in

2016 following further consultation.[15]

2.12

The tax discussion paper commented on challenges arising from the potential

for digital currencies to increase the ability of companies to relocate profits

to minimise their tax. The discussion paper noted:

...financial markets are increasingly globally integrated, and

the international flow of capital has become less restricted and more mobile.

Technology has also allowed new business models to evolve that have

substantially changed the way businesses and consumers interact. New ways of

transacting, including crypto-currencies such as bitcoin, were not contemplated

when the current tax system was designed.[16]

International approaches

2.13

The ATO's ruling, that digital currency is a commodity rather than a

currency, is similar to the tax guidance provided by relevant authorities in

other countries such as Canada and Singapore.[17]

Alternatively, other jurisdictions such as the United Kingdom and most recently

Spain, have released guidance advising that digital currency is exempt from

value added tax (VAT) under Article 135(1)(d) of the European Union (EU) VAT

Directive.[18]

The EU is waiting on a ruling from the EU Court of Justice on the correct

interpretation of the relevant EU VAT directive.[19] Sweden's tax authorities

have challenged a previous Swedish decision that digital currency should be VAT

exempt.[20]

Financial regulation and consumer

protection

Reserve Bank of Australia

2.14

The Reserve Bank of Australia (RBA) is the principal regulator of the

payments system, and administers the Payment Systems (Regulation) Act 1998

(PSRA). The RBA's general regulatory approach under the PSRA relies principally

on 'industry- or market-driven solutions', intervening only when necessary on

the grounds of its 'responsibility for efficiency and competition in the

payments system and controlling systemic risk'. The RBA considers digital

currencies are currently in limited use and do not yet raise any significant

concerns with respect to competition, efficiency or risk to the financial

system; and are not currently regulated by the RBA or subject to regulatory

oversight.[21]

2.15

In April 2015, the RBA informed the committee that it would be assessing

whether the current regulatory framework could accommodate alternative mediums

of exchange such as digital currencies.[22]

ASIC and ACCC

2.16

The Australian Securities and Investments Commission's (ASIC) view is

that digital currencies themselves do not fall within the legal definition of

'financial product' under the Corporations Act 2001 (Corporations Act)

or the Australian Securities and Investments Commission Act 2001

(ASIC Act). This means that 'a person is not providing financial services when they

operate a digital currency trading platform, provide advice on digital

currencies or arrange for others to buy and sell digital currencies'. However,

some facilitates associated with digital currencies may fit within the

definition as financial products.[23]

2.17

ASIC has issued advice to consumers on its MoneySmart webpage outlining

some of the of the risks of digital currencies:

Virtual currencies have less safeguards—The exchange

platforms on which you buy and sell virtual currencies are generally not

regulated, which means that if the platform fails or is hacked, you are not

protected and have no statutory recourse. Virtual currency failures in the past

have made investors lose significant amounts of real money. Some countries are

moving towards regulating virtual currencies, however virtual currencies are

not recognised as legal tender.

Values fluctuate—The value of a virtual currency can

fluctuate wildly. The value is largely based on its popularity at a given time

which will be influenced by factors such as the number of people using the

currency and the ease with which it can be traded or used.

Your money could be stolen—Just as your real wallet can be

stolen by a thief, the contents of your digital wallet can be stolen by a

computer hacker. Your digital wallet has a public key and a private key, like a

password or a PIN number. However, virtual currency systems allow users to

remain anonymous and there is no central data bank. If hackers steal your

digital currency you have little hope of getting it back. You also have no

protection against unauthorised or incorrect debits from your digital wallet.

Popular with criminals—The anonymous nature of virtual

currencies makes them attractive to criminals who use them for money laundering

and other illegal activities.[24]

2.18

In summary, ASIC advised that 'if you decide to trade or use virtual

currencies you are taking on a lot of risk with no recourse if things go wrong'.[25]

2.19

On 26 November 2014, the Parliamentary Joint Committee on Corporations

and Financial Services tabled a report on the oversight of ASIC. During the

course of the inquiry, ASIC informed the committee of its approach to digital

currency:

Virtual currencies such as Bitcoins are a developing area

globally. ASIC monitors new developments in the marketplace and, accordingly,

ASIC is considering whether and how the legislation it administers, such as the

Corporations Act, applies to virtual currencies.

ASIC's view is that Bitcoins themselves (and other virtual

currencies) are not financial products and are not regulated under the

legislation we administer. Unlike Australian dollars or other traditional

currencies, Bitcoins are not issued by a central bank and do not give the

Bitcoin holder any right to make payments in this form.

ASIC is consulting with other Australian regulators that are

also giving consideration to the regulation of virtual currencies. This

includes both financial regulators and law enforcement agencies that are

examining the use of Bitcoin in criminal activities. Additionally, the

regulation of Bitcoins is being considered by regulators and policy makers

internationally.[26]

2.20

The Parliamentary Joint Committee on Corporations and Financial Services

noted that it will continue to monitor the development of digital currencies.[27]

2.21

While ASIC does not consider digital currencies to be currency or money

for the purposes of the Corporations Act or the ASIC Act, the general consumer

protection provisions of the Competition and Consumer Act 2010 apply to

digital currencies, rather than the equivalent provisions in the ASIC Act. The Competition

and Consumer Act 2010 is administered by the Australian Competition and

Consumer Commission (ACCC). The ACCC's SCAMwatch and consumer information

webpages do not include any specific warnings about digital currencies.[28]

Financial System Inquiry

2.22

On 20 December 2013, the Hon Joe Hockey MP, Treasurer, announced the

final terms of reference for the government's Financial System Inquiry (FSI)

and the appointment of four members of the inquiry panel to be chaired by Mr David Murray AO.

The purpose of the FSI was to examine how Australia's financial system could be

'positioned to best meet Australia's evolving needs and support Australia's

economic growth'.[29]

On 7 December 2014, the final report of the FSI was released and the Treasury

is currently conducting a consultation process on the FSI recommendations.[30]

2.23

The FSI report noted that national currencies are currently the only

instruments widely used to fulfil the economic functions of money—that is, as a

store of value, a medium of exchange and a unit of account. The FSI found that:

Digital currencies are not currently widely used as a unit of

account in Australia and as such may not be regarded as 'money'. However, their

use in payment systems could expand in the future. It will be important that

payments system regulation is able to accommodate them, as well as other

potential payment instruments that are not yet conceived. Current legislation

should be reviewed to ensure payment services using alternative mediums of

exchange can be regulated—from consumer, stability, competition, efficiency and

AML [anti-money laundering] perspectives—if a public interest case arises.[31]

International approaches

2.24

In August 2014, the UK government announced it was considering

regulation of digital currencies. In November 2014, it published a call for

information and the outcome of this consultation process was released in March

2015. In relation to consumer protection the UK government announced its

intention to work with the digital currency industry and the British Standards

Institution to develop voluntary standards for consumer protection. In its

view, this approach would address potential risks to consumers without imposing

a disproportionate regulatory burden on the digital currency industry.[32]

2.25

The Canadian Senate's Standing Committee on Banking Trade and Commerce conducted

an inquiry into digital currency and tabled its report on 19 June 2015. It investigated

how digital currency should be treated, including whether it should be

regulated. It recommended that the Canadian government should exercise a

regulatory 'light touch' in order to create an environment that fosters

innovation and minimises the risks of stifling new technologies.[33]

2.26

Both the Singapore and Canadian governments have published advice for

consumers, similar to ASIC's MoneySmart webpage, warning consumers of the risks

associated with digital currency.[34]

Law enforcement

2.27

Digital currencies, such as Bitcoin, are not currently covered under section

5 of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006

(AML/CTF Act). The Act, however, recognises e-currency, which is defined as

follows:

e-currency means an internet-based,

electronic means of exchange that is:

- known as any of the following:

-

e-currency;

-

e-money;

-

digital currency;

-

a name specified in the AML/CTF

Rules; and

-

backed either directly or

indirectly by:

-

precious metal; or

-

bullion; or

-

a thing of a kind prescribed by

the AML/CTF Rules; and

-

not issued by or under the

authority of a government body;

-

and includes anything that, under

the regulations, is taken to be

e-currency for the purposes of this Act.

2.28

The AML/CTF Act currently only covers a very small proportion of the

digital currencies. It does not cover digital currencies, such as Bitcoin, that

are not backed by precious metal or bullion. While subsection 5(b)(iii) enables

the regulation of digital currencies backed either directly or indirectly by 'a

thing of a kind prescribed by the AML/CTF Rules', no such rules have been

issued to date.[35]

2.29

Australia's current AML/CTF regime allows for limited regulatory

oversight of convertible digital currencies. Because digital currencies such as

Bitcoin are not yet widely used and accepted, they are yet to form a 'closed loop'

economy, and whenever they are exchanged for fiat currencies, or vice versa

('on ramps' and 'off ramps'), the transactions will generally intersect with

banking or remittance services which are regulated under the AML/CTF regime.[36]

For example, Australian Transaction Reports and Analysis Centre (AUSTRAC),

Australia's AML/CTF regulator, is able to monitor and track reportable

transactions such as:

-

reports of international funds transfer instructions (IFTIs)

between Australian accounts and foreign accounts for the purchase/sale of

digital currencies;

-

threshold transaction reports (TTRs) for cash

deposits/withdrawals of AUD10,000 or more involving the bank accounts of

digital currency exchange providers; and

-

suspicious matter reports (SMRs) submitted where reporting

entities consider financial activity involving a digital currency exchange to

be suspicious.[37]

Statutory Review of the Anti-Money

Laundering and Counter-Terrorism Financing Act 2006

2.30

In December 2013, the Australian government commenced a statutory review

of the operation of the Anti-Money Laundering and Counter-Terrorism

Financing Act 2006 (AML/CTF Act)—the review is required under section 251

of the AML/CTF Act.[38]

The Attorney-General's Department stated:

The use and ongoing

expansion of digital currencies is an area of continuing policy interest to the

Attorney-General's Department. A number of options to address the money

laundering and terrorism financing issues created by the emergence of digital

currency systems are being considered in the context of the statutory review of

the AML/CTF Act.[39]

Parliamentary Joint Committee on

Law Enforcement

2.31

The Parliamentary Joint Committee on Law Enforcement is currently

conducting an inquiry into financial related crime and received evidence from

law enforcement agencies in relation to Bitcoin and financial crime. [40]

The inquiry was referred on 5 March 2014 and is expected to report late in

2015.

International approaches

2.32

In March 2015, the UK government flagged its intention to apply

anti-money laundering regulation to digital currency exchanges, and committed

to a full consultation on the proposed regulatory approach in the next

Parliament in response to the findings of its consultation process.[41]

2.33

On 19 June 2014, the Canadian AML/CTF legislation, the Proceeds of

Crime (Money Laundering) and Terrorist Financing Act, was amended to bring money

service businesses (MSB) dealing in digital currencies under Canada's AML/CTF

regime. Once new regulations are drafted and come into force, they will cover

digital currency exchanges, but not individuals or businesses that use digital

currencies for buying and selling goods and services.[42]

2.34

In its report on digital currency, the Canadian Senate's Standing Committee

on Banking Trade and Commerce recommended that the Canadian government should

require digital currency exchanges, excluding businesses that solely provide

wallet services, to meet the same requirements as money service businesses

under Canada's AML/CTF laws. The report recommended that digital currency

exchanges should be defined as 'any business that allows customers to convert

state-issued currency to digital currency and digital currencies to

state-issued currency or other digital currencies'.[43]

2.35

On 13 March 2014, the Money Authority of Singapore (MAS) announced that

it would regulate digital currency intermediaries that buy, sell or facilitate

the exchange of digital currencies for fiat currencies under its AML/CTF

regime.[44]

Financial Action Task Force

2.36

The Financial Action Task Force (FATF) is an independent

intergovernmental body that develops and promotes policies to protect the

global financial system against money laundering and terrorism financing. FATF

released a report on digital currencies in June 2014, establishing a common

definitional vocabulary and suggesting a conceptual framework for understanding

and addressing the AML/CTF risks associated with digital currencies.[45]

2.37

On 1 July 2014, Mr Roger Wilkins AO, former Secretary of the Attorney

General's Department, assumed the Presidency of the FATF. Mr Wilkins has

indicated that during his term he intends to examine the money laundering and

terrorism financing risks associated with digital currencies and, consider

whether further policy measures are necessary.[46]

Conclusion

2.38

Countries are considering the regulatory challenges presented by the

emergence of new forms of digital currencies. Australia is no exception and in

the following chapters the committee will explore some of these challenges and

how best to address them.

Navigation: Previous Page | Contents | Next Page