Navigation: Previous Page | Contents | Next Page

Chapter 16 - The cultural environment

‘Money Dreaming’

16.1

The magnitude of the problem in delivering banking and financial

services to Indigenous people in remote Australia goes deeper then the lack of

formal education and has its roots in the cultural gulf between the people and

the mainstream business world.[1]

Mr Barry Smith, Assistant Secretary, Department of Family and Community

Services, quoted an elder from Daguragu who explained that their stories,

traditions and pattern of behaviour do not have a ‘money dreaming’. He said:

‘You white people actually do have a money dreaming. You have the whole history

of managing and using money.’

16.2

Mr Smith noted that understanding money matters is something that is

growing among Indigenous people but ‘we have to find ways to grow it both

culturally and substantially for those people’.[2]

As underlined by Ms McDonnell:

Indigenous consumers of banking services have specific needs

and they are simply not met by the basic banking model at the moment that

privileges a set of norms that Indigenous people just are not involved in.[3]

16.3

For example, there are cultural forces that must be recognised when

considering measures to assist Indigenous Australians manage their financial

affairs. Professor Altman drew attention to the tendency of social networks to

place ‘enormous demands’ on individuals to share cash.[4]

Mr Smith made a similar reference to the pressures on people to provide for

extended families which he called ‘demand sharing’. He told the Committee:

If you are trying to deal with somebody who is wanting

demand sharing and they want to use that money for alcohol or gambling or some

other use, then converting it into another product or another transactable note

or whatever can help you manage that demand sharing. You are quite happy for

demand sharing if it is around food but you do not have to give cash which then

could be used for other products. That has been useful. Not everybody has used

it but for some people it has been useful. The term is ‘humbugging’ but it is

tied up with the demand sharing. Older people find it much more difficult to

say no. Younger people probably find it easier to say no because they are

probably a little bit distanced from that cultural requirement.[5]

16.4

People working with the Tangentyere Council in Alice Springs also

commented on the broader obligations that Aboriginal people have toward a wider

range of people—‘they feel obligated to take all the money and share it’.[6]

Mr Acfield, Tangentyere Council, stated that their money, ‘in a sense, is a

resource that can be utilised communally’.[7]

16.5

The Cape York Community Financial Project Ltd informed the Committee

that the cultural rules of its communities include ‘an underpinning reciprocity

and demand sharing amongst the community members and the kinship, ties and

social alliances which extend beyond families and households’. It submitted:

The banks are seen as cash outlets not as saving facilities

and there is a low cultural emphasis on savings.[8]

16.6

Another example which highlights the special needs of some Indigenous

people living in remote areas revolves around the problem often referred to as

the ‘feast or famine’ or ‘boom and bust’ cycle. This cycle involves ‘people

spending their welfare payment soon after receiving it, and being left without

money until their next payment’.[9]

Delivering culturally appropriate services

16.7

Reconciliation Australia asserted that real improvements in Indigenous

access to banking and financial services in rural and remote areas ‘can only be

made by developing mutually beneficial cooperation between Indigenous

communities, the financial services sector and governments’.[10]

16.8

The following section looks at three groups that are currently helping

people meet the challenge of delivering banking and financial services to

Indigenous Australians—the Tangentyere Council, the Traditional Credit Union

(TCU) and the Cape York Community Financial Project. They have been described

as ‘best practice models in the delivery of banking and financial services to

Indigenous people in remote areas’.[11]

The Tangentyere Council

16.9

The Tangentyere Council is an Aboriginal run council which provides

services to Indigenous people living in town camps in Alice Springs. It has

been providing financial services to town campers for over 15 years through a

Westpac agency located on its premises.[12]

16.10

This bank agency delivers ‘culturally appropriate face-to-face banking

and financial services by Aboriginal staff in Aboriginal languages’.[13]

In addition to cashing cheques, it allows customers to pay off debts to the

Council for low-value items such as blankets and tucker boxes.[14]

The agency also offers literacy training and specialised Aboriginal banking

products, such as clan accounts and food vouchers.[15]

It assists Indigenous people combat the feast and famine cycle by offering a

food voucher system whereby people can place an amount of their welfare payment

into an account which is then used for food.[16]

Mr William Tilmouth, CEO of the Council, explained:

Clients electing to use the system can get a food voucher

every second day after pension day. The vouchers range in value from $40 to

$100 depending upon the number of people being fed in the family and the value

of the client’s Centelink payment.

People can use their vouchers at a local supermarket that

they can travel to free of charge on one of two Tangentyere Council buses that

run throughout the day between the Town Camps, Tangentyere Council, the

supermarket and, when needed, the hospital.[17]

...

Because the supermarket enforces a ‘no-grog’ rule on the use

of food vouchers, the system also helps families cope with alcoholism. Holding

a food voucher instead of cash provides clients with some protection from

pestering from drunk family members and, in some instances, Tangentyere Council

has allowed the sober adult of the family to draw food vouchers on the

alcoholic’s account with their sober consent. This helps to keep children fed

and helps alcoholics fulfil their obligations to their family.[18]

16.11

The effectiveness of this scheme appeared to be under threat with the

transfer from cheque payments to electronic payment. According to Mr Tilmouth,

the problem was solved when the Department of Family and Community Services and

Centrelink helped Tangentyere Council develop a new food voucher system using

the Centrepay deduction facility.[19]

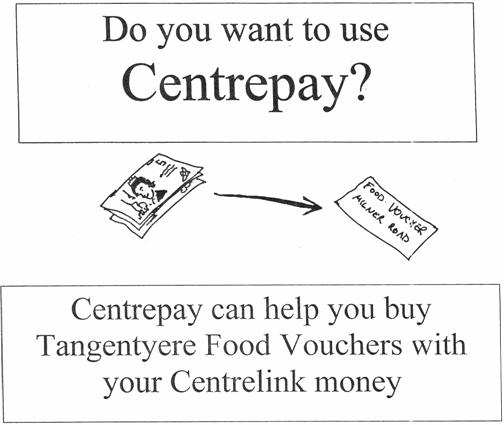

16.12 The accompanying illustrations produced by

the Tangentyere Council show the steps taken by the staff to assist their

members not only with basic banking services but with budgeting and managing

some of the cultural pressures such as ‘humbugging’.

16.13

As noted earlier one of the main problems with electronic banking was

people losing their key card. The bank agency has been able to rectify this

problem by holding their customers’ cards for them.

16.14

Again, education and training is central to the effective use of banking

services. The agency in collaboration with the Department of Family and

Community Services, Westpac and ATSIC undertook a bank pilot project which

addressed this matter. The bank liaison officers operated out of an air-conditioned

demountable building, called the Bank Training Room, in which clients could

watch a video in Aboriginal language explaining the benefits of keycards, and

receive training while their forms were being processed. According to Mr Tilmouth,

‘Initially, the flow of clients from the bank agency to the Bank Training

Room...was slow. However, this problem was overcome by giving clients a brightly

coloured “ticket” to the Bank Training Room’.[20]

16.15

Mr McDonald stressed that the education program did not go beyond providing

people with the skills and training to perform basic banking transactions. He

told the Committee that they did not reach a stage where they were ‘providing

people directly with budgeting skills, such as numeracy skills, so that they

could sit down with a calculator and rejig their own budget every fortnight.

That level of training has not been started’.[21]

16.16

The project with the help of Centrelink has also enabled recipients of

welfare benefits to better manage their welfare payments. Mr Tilmouth explained:

Having a Centrelink office on Tangentyere Council’s premises

has made opening bank accounts and signing up people for Centrepay deductions

relatively easy. Centrelink staff are able to provide our clients with letters

of introduction for the opening of bank accounts and payment details so that

the bank liaison officers can help them through a static budgeting process to

decide if and to what extent they want to sign up for food vouchers. The bank

liaison officers, however, do not provide clients with training in numerical

and budgeting skills.[22]

16.17

While the Tangentyere Council provides a valuable service, it is running

at a loss. Mr Westbury explained:

...because of the level of servicing and support that is

required for people coming in from the communities, and the whole issue of

cards and all those things you have heard from other evidence before you, the

actual costs for Tangentyere to maintain that service are well over what they

get back through fees from the bank or what they raise through their clients.[23]

16.18

The Tangentyere Council, however, is prepared to subsidise the

operation of the bank agency because of the vital need to provide Aboriginal

people in the region with ‘culturally appropriate services in a welcoming

environment’.[24]

The following illustrations produced by the Tangentyere Council show the

involvement of agency staff in helping local Indigenous Australians understand

how modern technology can be used to their advantage. It also highlights the

labour intensive component of their work.

The Traditional Credit Union

16.19

The Traditional Credit Union (TCU) has developed another model that

addresses some of the problems associated with delivering financial services to

Indigenous people living in remote areas of Australia. It is an Aboriginal run

credit union operating in the Northern Territory. It was incorporated in

December 1994, has a head office in Darwin with eleven remote branches and two

agencies. According to the Assistant General Manager of the TCU, Ms Bev McMillan:

When TCU began operation it was seen to be a way for members

to put money away for later and to [provide] protection from family pressure.

Today TCU is far more than this, offering up to date services:

Savings,

budget and Christmas Club accounts;

Cuecards

that can be used in all EFT-POS and most ATM machines Australia wide and some

overseas machines;

Family or

Clan accounts to be used for joint saving;

Business

Accounts;

Cheque

accounts;

Internet

Banking;

Bpay;

Personal

loans up to $10,000, initial loan maximum is $5,000 with some members on their

second or third loan having paid off previous loans;

In partnership with ATSIC, TCU offer a Small Business Loans

Scheme with loans up to $15,000.[25]

16.20

It has been effective in assisting communities combat the feast and

famine cycle prevalent in some families. According to a report:

...anecdotal evidence indicates that since the TCU began

operating, people are more likely to spend their money over a full fortnight

and are more able to save...that many TCU members utilise budget accounts, saving

money over a period of time and purchasing white goods, furniture, small motor

vehicles and boats, or using it to go on holiday. Such evidence belies the myth

that Indigenous people, and particularly those on very low incomes, cannot

save.[26]

16.21

Mr David Shoobridge from the Daly River Community provided another

example of where the TCU encourages their customers to bank wisely. He stated:

You cannot walk in with a deposit and get a loan within the

next day or couple of days. You have got to take three months to build up your

credit and to deposit the amount of money you need as a deposit over the three

months. In many ways, that is like an education program. It teaches people to

save, and it teaches them that they have a responsibility to pay regularly.[27]

16.22

The TCU is committed to training local staff and provides the required

level of training that has enabled the credit union to use local staff to

operate its branches. It employs Indigenous people to work in and manage its

remote branches and offers them the opportunity for promotion. At the moment,

the TCU has two remote Indigenous branch supervisors who have served 5 years.[28]

Ms McMillan attributes the success of the TCU to:

- the initiative of Aboriginal elders who saw it as something they

needed and who were determined for it to become a reality;

- the commitment to providing real jobs to Aboriginal people in

their own community;

- the training of staff to perform their duties with pride and

self-confidence;

- the membership structure where members are equal shareholders and

own the institution;

- the directors and senior management who work together to create a

high standard and work ethic; and

- TCU’s understanding of Aboriginal culture and its ability to work

without compromising the regulatory obligations of a financial institution.[29]

16.23

Ms McMillan’s remarks are borne out by the comments of Mr Djerringal Gaykamanu,

a director and founding member of the TCU. He indicated that the TCU’s

importance to Indigenous communities went further than just providing

much-needed banking and financial services. He stated:

I started in the sixties to work with the people, bit by bit,

for community development and I am still working. I am the eldest at

Milingimbi. I look after the community and I look after the TCU. I know the

background story of the TCU—where it started, where it has come from and what

it is like now. The TCU is a very big name and it has become really good.

Everybody is happy that we started small and have grown big. That is very

important for our training, for business and for saving money. We can show our

kids down there why we started it up.[30]

16.24

In the view of the Northern Territory Government, the TCU has

demonstrated ‘a culturally effective strategy to deliver banking and financial

services to isolated indigenous communities.’[31]

It stated further:

The TCU’s approach lends itself to be adopted as a model for

other remote areas with a significant Indigenous and welfare dependent sector.[32]

16.25

The Department of Family and Community Services also acknowledged the

contribution that the TCU is making to provide banking services to remote

communities. Likewise, Reconciliation Australia praised the work of the TCU

maintaining that it provides a possible ‘best practice’ model for the delivery

of banking and financial services. [33]

Limitations on expanding services

16.26

The TCU, however, faces the same difficulties as those experienced by

smaller ADIs in country areas, including limited capital reserves and a

regulatory regime that places limits on their ability to expand services and

establish new sites. As with other smaller ADIs, the TCU’s low level of

reserves, its conservative risk management plan and its reluctance to charge

excessive fees to cover costs hamper its expansion. The TCU, while accepting

that regulation is necessary, highlighted the difficulties that such a regime

places on smaller ADIs. Ms Barbara Bradshaw, former General Manager of the TCU,

maintained that meeting the regulatory requirements is a major issue for the

TCU:

This not only increase[s] costs, but it can be a difficult

and time-consuming matter, particularly when a lot of the requirements were

devised for much larger organisations operating in an urban environment. A lot

of effort has gone into these compliance issues, but it somehow seems that

after one challenge had been dealt with, a greater one arrives.[34]

The regulatory regime and compliance costs

16.27

To comply with the regulations under the FSRA, the TCU had to change

from providing customers with basic information that was easy to read and

understand to producing a two-page product disclosure statement on every

product. According to the TCU, every time it signs on a new member it has to

give them ‘an inch thick of paperwork with all the regulatory requirements of

using its services and the products, their rights of reply, the Privacy Act,

code of conduct, and terms and conditions of use’. This is but one example of

the range of compliance costs the TCU incurs in satisfying the regulatory

requirements of the FSRA.

16.28

Furthermore, the experiences of the TCU highlight the importance of

having a regulatory regime that has the flexibility to take account of the

interests of all consumers. In this case, the Indigenous people living in

remote communities whose needs are not necessarily met by the current

disclosure requirements. The primary concern of the TCU is to deliver a service

in a culturally appropriate way that will equip their Indigenous customers with

the skills needed to conduct basic banking transactions and to manage a

fortnightly personal budget.

16.29

As detailed above the costs in delivering banking and financial services

to remote communities are significant and are ultimately borne by the customer.

The TCU acknowledged that despite its efforts to contain costs, it has a high

fee level and level of interest rates for loans. It told the Committee:

The fees charged represent our costs of operation in a

challenging environment. This point is made to our members and I believe that

whilst many do not like the higher fees they realise that they represent the

costs of operating in remote communities. They also appreciate having the

Traditional Credit Union there.[35]

16.30

The problems faced by credit unions in complying with regulations was

covered in chapter 8. The Committee found that the current regulatory regime

frustrates the attempts of smaller ADIs to establish a presence in remote Australia.

It recommended that APRA and ASIC consult with CUSCAL and with smaller ADIs

about the limitations placed on them by the regulatory regime in meeting the

banking needs of Australians living in rural, regional and remote communities.

The Committee recommended that particular focus be placed on ADIs working with

Indigenous communities in the remote areas of Australia.

16.31

The work of the Tangentyere Council and the TCU, underlines the

importance of the Committee’s recommendation particularly in having the review

look at the specific circumstances of ADIs providing services in remote

Indigenous communities. The Committee believes that consideration must be given

to find better and more effective ways to minimise compliance costs while

promoting the interests of Indigenous consumers. Clearly, Indigenous people

with poor literacy and numeracy skills are unlikely to benefit from information

presented in complex and lengthy documents. The illustrations prepared by the

Tangentyere Council show the need for flexibility and sensitivity in meeting

the needs of the Indigenous consumer.

Competition with the traditional banks

16.32

The TCU also shares the same problem as other non-bank ADIs in competing

with well known traditional banks with their long-established reputations and

their large client base. In this case rather than ‘cherry pick’ valued

customers there is a tendency for the banks to discourage less valued ones. The

TCU explained that:

The four major banks openly encourage their Indigenous clients

to transfer their accounts to the TCU, as they are costly clients and a

nuisance factor in their banks.[36]

16.33

The TCU suggested that the big banks could compensate it for ‘taking

over these high-overhead clients’. Not only does the TCU look after these

customers, but it takes responsibility for educating and training them in the

use of banking services even though they are not necessarily TCU customers.

The Cape York Community

16.34

Before leaving the discussion on the work of individual communities or

organisations, the Committee draws attention to the work being done on Cape

York. The Cape York Community Financial Project Ltd formed as part of the

Aurukun Shire Council intends to establish a credit union for Aboriginal people

in Cape York to be known as the Cape York Community Credit Union Ltd.

16.35

It is hoped that the ownership of and involvement in the local credit

union will encourage community members to save for the benefit of the whole

community. The Cape York Community Financial Project Ltd stated simply that

the whole concept behind the credit union is to facilitate the development of a

real Aboriginal community economy for the benefit of all the local communities.

The Australian Government has recently allocated $90,000 to help the community

develop a business plan for the credit union.[37]

16.36

Westpac is involved in trials in three communities in Cape York with the

‘Family Income Management’ Project. The program is aimed at increasing the

purchasing power of families in Cape York by teaching and assisting them to

save for a special purpose by putting aside a proportion of their income on a

regular basis. A Cape York Project Manager with Westpac has no doubt that the

project can be a success:

When we came back in April of last year with a second group of

secondees, the FIM project was still quite not established but almost and

Hersey and Kenlock [keen local participants in the Project] were continually

shuttling in families. I think it was about 25 families in the first day and they

all engaged with Family Income Management. There are little things that you see

every day like the number of washing machines under houses and the

ramifications of a simple thing like a washing machine that we take for granted

like health implications are enormous.[38]

16.37

On 6 August 2003, the Prime Minister announced that the Australian

Government would commit a further $1.5 million to allow the expansion of the

trials.

16.38

The Cape York Community Financial Project maintained that the

introduction of a credit union to the communities of Cape York, along with the

Family Income Management Plan, ‘will go a long way towards assisting the

communities in building their own economy and assisting the indigenous people

to move beyond passive welfare and towards financial and economic

independence’.[39]

16.39

Westpac has also embarked on a three-year project to encourage local

business by committing 150 members of its workforce to come into the community

and work with local groups to start up various enterprises.[40]

Summary

16.40

A number of themes emerge from the work being undertaken by the

Tangentyere Council, the TCU, the Cape York Community Financial Project and

Westpac in remote communities. The first is the need for long term and genuine

commitment by partners to the project. Ms Tania Major from the Cape York region

stressed that continuity in assistance was most important in winning the

confidence of local people. The communities wanted more than just words and

one-off projects. She stated that there needs to be a commitment on behalf of

those coming into the communities to help:

Continuity—them coming back to the community and seeing they are

genuine about what they are saying and the fact that they are constantly in the

community and helping seeing something evolve from all this word.[41]

16.41

The second theme concerns community involvement. Mr Gaykamanu, one of

the founding members of the Traditional Credit Union, stressed the importance

for the local people to own and support the project. He told the Committee:

The little credit union is just like your home: you live there.

That is why I said the credit union needs a home at Milingimbi for these

people. This Traditional Credit Union is not going to be going somewhere else,

either. I went down to the Daly River and talked to their people. I said,

‘Where are we going to put the TCU, and who is going to own it?’ I looked

around—owned by somebody that was going to be living there. We are come-and-go

people; we move around a lot, and this is why I said it. If we leave it there,

who is going to look after it?[42]

16.42

The third theme is the need for funding and support from both

governments and the private sector to assist Indigenous communities gain their

economic independence.

Committee view

16.43

The Committee commends the work of the Tangentyere Council, the TCU, the

Cape York Community Financial Project and Westpac in assisting people in remote

Indigenous communities to better manage their financial affairs. Such

partnerships are fundamental to the success of education and training programs

and should have the strong support of the Australian Government.

16.44

While acknowledging the achievements of the various pilot programs and

trials taking place, the Committee takes particular note of the views of local

people that continuity and commitment are crucial if the effects are to be

lasting. The Committee strongly supports continued funding for such projects.

Recommendation 27

The Committee recommends that the Australian Government continue

funding projects such as the Family Income Management Plan. It, however,

recommends that the Australian Government, relevant State and local governments

and the banking industry work with Indigenous communities to map out a plan

that would use the successes already achieved in trials as a platform on which

to build a more coherent and integrated policy for the economic independence of

Indigenous people. The work done by the Tangentyere Council, the TCU and the

Cape York Community should be stepping stones leading to even greater and

lasting success in advancing the economic welfare and independence of

Indigenous Australians.

16.45

The Committee acknowledges the involvement of Westpac in the various

projects and encourages it to continue its work. At the same time, the

Committee notes the absence of the other major financial institutions from any

significant engagement in Indigenous communities and would like to see them

follow Westpac’s example.

16.46

In its supplementary submission, the ABA outlined a proposal that is in

keeping with the Committee’s recommendation for both the public and private

sector to become partners in assisting remote communities with their banking

and financial services needs. The ABA commissioned a study of access to banking

services which is discussed in chapter 6. The resultant survey identified 32

towns across Australia that did not have adequate face-to-face banking

services. They tend to be located in very remote regions of Australia and have

a higher proportion of Indigenous people living in the community.

16.47

Having identified the areas most in need of assistance, the ABA proposes

to move onto the next stage by leading a tri-partite Round Table (‘Remote

Services Round Table’) including relevant government agencies together with

Reconciliation Australia ‘to draw action plans to improve access’. It stated:

Banks are committed to improving access, and we need cooperation

of the bureaucracy and indigenous leaders before resources can be allocated.[43]

16.48

The Committee endorses this initiative but would like to see any such

project move beyond the stage of talking to one of active and sustained

involvement by the banking industry in improving access to financial and

banking services. The banks can best demonstrate their commitment by

establishing, with the help of local communities, a presence in these

communities.

16.49

The Committee now turns to examine the operation of the RTC program in

remote Australia.

Rural Transaction Centres in remote Indigenous communities

16.50

RTCs also offer the opportunity to expand banking and financial services

in remote areas of Australia. To date, however, progress has been very slow

with only four operational RTCs in the Territory. They are at Oenpelli,

Mataranka, Numbulwar and Maningrida. There is one under development at Wadeye

(Port Keats). All except Mataranka are Indigenous RTCs and include the Traditional

Credit Union, Centrelink and a range of community services. Mataranka has a

Post Office with giroPost, Centrelink and other services.[44]

16.51

The main difficulties with establishing an RTC in remote Australia are

the same as those experienced in rural and regional Australia but the hurdles

tend to be higher. Many isolated communities are unable to generate the

required critical scale of business activity to be commercially viable. The

experiences of the TCU testify to the particular difficulties that remote

communities have in building a creditable business case which has to take

account of the heavy expenses involved in providing services to outlying areas.

16.52

Reconciliation Australia observed that for many small Indigenous

communities, economies of scale dictate that only if they collaborate through

joint ventures with other communities will they ‘be able to demonstrate the

self-sustainability required by the RTC Program guidelines’.

16.53

But the scope and ambition of the RTC program make it difficult to accommodate

the particular challenges posed by Indigenous communities. Mr Westbury

suggested that more thought ‘needs to be given to designing the program around

the realities associated with these communities’. He stated:

They may require different and more flexible approaches to

the ways in which applications are assessed and encouraged. By that I mean that

there may be ways by which the fund might encourage Aboriginal communities to

group together to make applications. Clearly, in terms of economies of scale,

in some cases it is just not practical or realistic to expect that a credit

union operation is going to be viable in each individual major community.[45]

16.54

The Tangentyere Council poses a different problem in meeting the funding

guidelines of the RTC program. It deals with groups of Indigenous people who

live within a large community but who are in effect ‘very isolated from that

community’. Mr Acfield, Tangentyere Council, explained:

The urban-remote divide becomes a bit blurred in Alice

Springs. That has been an issue for us and it is part of the reason we have

gone for the hub notion. We can effectively use remote communities’ access to

RTC funding to then pull together a hub in Alice Springs, rather than go for

funding which might go the other way—in other words, to set up a program which

could be funded from Alice Springs to provide services. We have had to be

fairly creative, if you like, about how we have used that fund.[46]

16.55

Apart from the difficulties facing a remote community in achieving a

critical level of business turnover, it must also have within it a group of

people capable of putting together a sound financial plan showing that there is

sufficient community backing and management skills to make the facility

commercially self-funding. The community, however, needs to draw on expertise

to build a sound business case in areas that are already commercially marginal.

Managing this critical stage is a significant obstacle. Ms Bev McMillan from

the TCU noted that compiling a business management plan to accompany the

funding application is:

...a mammoth task for a manager in a community who is already

overworked and overtaxed. Sometimes they do not have the time or have the

ability to get that one step further to take advantage of the funding.[47]

16.56

Indeed, the experiences of the Nyirranggulung Mardrulk Ngadberre

Regional Council underline the difficulties in bringing together a business

plan. It reported that progress to establish an RTC at Bulman had stalled

because its ‘remoteness makes it impossible to undertake the negotiation

necessary to develop the agreements and commitments required to complete a

business plan’. It informed the Committee:

Proposed service providers for the RTC included a credit union,

Centrelink, Batchelor College and others. Negotiating letters of intent and

lease agreements with these providers has proved an impossible hurdle from

Bulman.[48]

Notwithstanding its disappointment, the Council was ‘looking

again at financial and other services in a regional framework’. It was firm in

the view that:

The RTC scheme can and will make a significant contribution to

accessing financial and other services in remote areas.[49]

16.57

There is also the partnership aspect of an RTC and the importance of

attracting a financial institution willing not only to support the enterprise

but equipped and sufficiently ambitious to broaden the scope of the financial

services to be provided. Professor Altman noted that the RTC program was still

in its infancy and that most of the centres he was aware of are ‘building

shells that are a form of infrastructure for financial, banking and other

service delivery agencies to locate in’.[50]

He stated further:

It seems to me that an RTC will only be as effective in

terms of banking and financial services as the operator you get in there. Again,

I guess we are just going back to the fact that if you can get a bank branch

into an RTC it would probably be very positive, particularly if it can provide

some business advisory services and access to business credit. But if it is a

credit union or giroPost or an ATM, for instance, then it is not going to make

a huge difference to the economic development potential for that community.[51]

16.58

Four key issues emerge from the discussion on the establishment of RTCs

in remote Australia:

- the problem in generating sufficient business activity to make an

RTC a commercially viable enterprise;

-

the RTC guidelines which appear to lack flexibility and fail to

recognise and appreciate the unique structure and composition of Indigenous

communities;

- the difficulty in locating a core of committed people from the

community with the professional and business skills and foresight to design and

initiate plans for the establishment of a financial institution that would meet

the needs of their people; and

- the lack of involvement of Australia’s major financial

institutions to support RTCs in remote areas of Australia.

16.59

In chapter 8, the Committee made a number of recommendations that are

intended to improve the operation of the RTC program. They are relevant to the

RTC program as it applies to remote areas especially the need for the program

to be able to accommodate the unique circumstances of isolated communities.

This section of the report has underscored the importance of this

recommendation.

16.60

The Committee also notes that the RTC board does not have an Indigenous

representative. Reconciliation Australia pointed out that although Indigenous

people form a high percentage of the population in many areas that are eligible

for assistance under the program, there is no Indigenous representation on the

RTC Advisory Board.[52]

Recommendation 28

The Committee recommends that a member from the Indigenous

community, who is able to represent the interests of Indigenous people living

in remote areas of Australia, be appointed to the RTC Board.

In addition, the Committee recommends that the RTC Board’s Charter

be amended to recognise specifically the need for the provision of services to

remote Indigenous communities.

Investment capital in remote Indigenous communities

16.61

The Committee now turns to two key issues briefly touched on in its

consideration of the operation of the RTC program in remote communities—the

shortage of local business and entrepreneurial skills and the absence of

financial institutions.

16.62

The lack of both business activity and leaders to drive commercial

activity means that financial institutions are not attracted to remote

Indigenous communities. But the very absence of banking and financial services

in itself means that business is not drawn to these areas and so an environment

that lacks both financial services and business activity and where financial

literacy and business skills are not fostered becomes self-perpetuating.

Professor Altman told the Committee:

...a certain rudimentary level of business banking services is

needed before commercially viable businesses can operate, unless small

Indigenous businesses are expected to operate without access to deposit

facilities, credit facilities and other financial services—hardly a realistic

option at the start of the 21st century.[53]

16.63

Such an environment then suffers from a range of difficulties especially

its ability to attract capital and to produce skilled people with the

initiative and confidence to establish commercial enterprises. Three financial

commentators noted:

Access to development, equity or venture capital typically

requires the existence on the part of the persons seeking such capital,

ownership of valuable assets and the requisite skills to manage and develop

those assets.[54]

16.64

They maintained that in the main Indigenous people do not have the

access to equity capital that is available to non-Indigenous Australians

because:

- they lack the skills to identify potential business opportunities

and to package and structure those opportunities;

- they lack business and management skills to operate and develop

businesses;

- they are not part of and have no connections into the

professional business world of the equity and investment markets, making it

impossible for them to access the requisite capital, advice and skills;

- they have not until recently, had access to assets which could be

used to attract equity capital; and

-

the assets held or ‘controlled’ by, and the opportunities

available to, Indigenous people are typically in locations remote from each

other and from major commercial centres.[55]

16.65

The Northern Territory Government submitted that:

If remote communities are to build their capacity to move

beyond local welfare or government supported economies, small business and

private joint venturers need access to banking and financial planning

facilities. Private sources of finance and financial services need to be

locally available to encourage economic development and retain cash within the

communities.[56]

16.66

Coupled with these various problems is the perception by banks that

Indigenous people have limited credit records and no collateral, are high risk,

and add no value to the bank’s financial bottom line.[57]

Mr Joseph Elu, Director, Reconciliation Australia, suggested that fees are

higher in some Indigenous communities:

I come from the Torres Strait and have lived there

almost all of my life, and the lack of banking facilities up there borders on

being funny...It is a fact that in the Torres Strait the National Bank were

charging higher interest fees. The reason they gave for that was that, because

people could not get insurance for their dinghies, the bank were stacking on a

couple of interest points for personal loans.[58]

16.67

The Nauiyu Nambiyu Community Government Council noted the propensity of

the larger banks not to consider loan applications in amounts less than $5,000

which creates difficulties for Aboriginal people.[59]

16.68

In many remote areas of Australia, the land is often communally owned

and legally inalienable.[60]

The Northern Territory Government informed the Committee that:

In mainstream Australian society personal banking and

financial services centre around the home mortgage, the family home forms the

basic framework of financial management and planning. In remote communities in

the Territory, however, the majority of housing is on Aboriginal Land, preventing

any legal form of home ownership.[61]

16.69

Mr Stephen Oxley from the Department of Immigration and Multicultural

and Indigenous Affairs submitted:

We think banks should be encouraged to examine opportunities

to provide home and business loan products targeted at the needs of Indigenous

people and that, together with ATSIC and local communities, there are

opportunities to look at creative methods of providing home loans to people

living on community Aboriginal title land, where there have been historical

impediments to use of that land as security.[62]

16.70

The Committee is aware that Indigenous people share with other people in

regional, rural and remote Australia difficulties in gaining access to adequate

banking and financial services. It notes, however, that some difficulties faced

by Indigenous people are often compounded by remoteness, lack of financial

literacy, socio-economic disadvantages, cultural differences or a combination

of some or all of these factors. In some cases, their need for assistance is

greater.

16.71

The theme that dominates any consideration of Indigenous financial

matters is the extent and interrelatedness of the complex problems confronting

Indigenous people in gaining access to banking and financial services. It is

clear to the Committee that each identified problem cannot be treated in

isolation. To tackle the problems effectively, the Committee believes that

there must be a concerted and coordinated approach to address these issues. The

Committee is not convinced that this has yet been developed.

16.72

The recommendations made in this part of the report must be placed in an

overall policy framework that is intended to improve the economic and social

welfare of Indigenous Australians. The strategy must clearly articulate its

intention to advance the economic independence of Indigenous Australians by

promoting informed decision making; furthering education about rights and

obligations in respect of banking services; facilitating the wide and confident

use of electronic banking in remote areas; fostering Indigenous commercial

activity; and providing incentives for Indigenous people to take up the study

of economics and commerce and take on employment in the field of financial

services. It should acknowledge that for programs to be successful Indigenous

communities must embrace them as their own.

16.73

Any broad plan to improve access to banking and financial services must

also seek to encourage financial institutions to make a commitment toward and

to put in place practical measures to improve the delivery of banking and

financial services to people in regional, rural and remote Australia

particularly Indigenous Australians. This matter will be dealt with in the

following chapter.

Part IV - Financial Institutions in the Community

The report has clearly established that there are pockets in

rural, regional and remote Australia where people experience difficulty in

obtaining banking and financial services. Local councils in particular have

written to the Committee outlining the problems that their residents and local

businesses have in accessing banking and financial services. In expressing

their unhappiness with the delivery of such services, a number of submissions

raised the issue of banks and whether they have a community obligation to

provide adequate banking and financial services.

This final part of the report discusses this matter of

financial institutions and the obligations they have to their customers and to

the broader community.

Australia is not alone in this debate about the

responsibility of banks to the community they serve and how to encourage or

even compel banks to take a more constructive role in assisting disadvantaged

communities. As well as exploring community service obligations, the following

part of the report looks at developments in this area in the United Kingdom,

the United States of America and in Canada and determines whether Australia can

learn from their reforms.

Finally, the report summaries its views on the role of

governments and the private sector in ensuring that all Australians have access

to adequate banking and financial services.

Navigation: Previous Page | Contents | Next Page

Top

|