20 july 2020

PDF version [384KB]

Ian Cronshaw

Visiting Fellow, Crawford School, Australian National University

Executive summary

- Nuclear electricity provides around a tenth of world electricity

needs, with only a few other applications in the energy sector. It is the

second largest source of low carbon electricity after hydro. However, recent

capacity additions in OECD countries have been few, and growth is now outside

OECD countries, dominated by China and India.

Australian electricity options are short briefings on the principal energy sources and storage options being debated in Australia, including: coal, natural gas, wind, nuclear, photovoltaics (PV) and pumped hydro energy storage (PHES).

The global COVID-19 pandemic and its economic consequences mean that statements and projections about future demand and pricing of energy options may no longer be reliable. Readers should note that some figures quoted in these briefings may pre-date the pandemic. |

Nuclear energy production

Nuclear

energy is deployed to produce electricity by harnessing the heat produced

in the fission, or splitting, of radioactive isotopes of uranium or plutonium

in a reactor. In the majority of cases, water is used to transfer heat to steam

turbines. Reliable supplies of cooling water are essential to the operation of

large-scale nuclear plants. Nuclear energy is also deployed in military

applications, notably submarines for power and propulsion, but also other

shipping, including aircraft carriers and icebreakers. Nuclear plants are

generally characterised by large capacity and output, high capital cost, and long

construction times, but relatively low operating costs and almost zero

emissions to air from their operation.

Nuclear

energy is used to produce electricity in 31 countries from some 450 nuclear

reactors, providing around 10 per cent of global electricity. Production

is concentrated in OECD countries, where nuclear provides almost one-fifth of

total electricity output. More recently, new construction has been dominated by

non-OECD countries, notably China, but also India and states of the former

Soviet Union, accounting for a large share of the 52 reactors currently under

construction.

Major nuclear power countries

The United

States accounts for around one-third of global nuclear electricity,

providing just under a fifth of US generation. The nation has almost 100

reactors, but most of these entered service more than 30 years ago. Only two

reactors are being built, supported by measures enacted in the Energy Policy

Act 2005.

Nuclear power peaked in Japan around a

decade ago, providing nearly a third of electricity generation. However, after

the devastating disaster at Fukushima in 2011, all plants were closed down.

This resulted in severe electricity shortages, managed largely by increased

imports of liquefied natural gas (LNG) and coal, demand management measures,

plus enhanced solar generation. Subsequently, reactors are slowly re-entering

service, but nuclear generation seems set to play a diminished, if still

important role in Japanese electricity supply.

France

produces around three-quarters of its electricity generation from 58 reactors,

but again, the majority of its reactor fleet entered service before 1990. This

generation enables France to be one of the world’s largest net exporters of

electricity. Only one new reactor is under construction at Flamanville,

Normandy. With construction having started in 2007, the plant is well behind

its projected schedule and well over budget. Construction of a similar plant

was started in 2005 in Finland,

and has yet to enter commercial service, and is also well over budget. In OECD

Europe, only these two reactors, plus two smaller ones in Slovakia,

and one in Turkey

are being built. Germany,

Europe’s largest economy, produces around a seventh of its electricity from

nuclear reactors, down from a quarter a decade ago, having closed a part of its

fleet after Fukushima. Further plant closures have been foreshadowed, with all

nuclear power plants to be shut down by the end of 2022. Solar and wind now

generate more electricity than nuclear in that country.

China has a

very active nuclear program as part of its rapid shift to diversify its

electricity sector away from coal. However, its 48 reactors currently account for

less than four per cent of electricity supply. Even with its current building

program, this share is only expected to increase to around eight per cent of generation

by 2030.

International Energy Agency (IEA) projections show that

nuclear generation will broadly maintain its current share of global power

markets, on the basis of non-OECD output growth—especially in China and India,

which will account for around 90 per cent of the net growth. The declining

contribution of nuclear power in advanced economies and its interaction with

carbon emissions is examined in the 2019 IEA report Nuclear Power in a Clean

Energy System.

Advantages and disadvantages

The key advantage of nuclear power is that its operation

produces no greenhouse gases and no significant emissions of other air

pollutants. However, power plant construction, transport of nuclear waste, and

decommissioning does result in emissions. Despite this, whole-of-life analysis

shows that nuclear power is much more ‘greenhouse-friendly’ than burning

hydrocarbons such as coal, peat, oil and natural gas. For this reason, there

have been calls to expand nuclear power to help mitigate climate change.

Disadvantages, apart from the high up-front cost mentioned

above, centre around the safe storage and disposal of high-level radioactive

waste, with only a few countries having built permanent repositories for this

waste. The United States identified a site in the 1980s for such a repository

in Nevada, but local opposition has slowed progress. Negative perceptions

towards nuclear power, especially around the safety of waste and the

possibility that an accident could release radiation into the environment, also

persist in Australia.

Other nuclear technologies

Other nuclear technologies include fast breeder reactors

(which produce more fuel than they use), thorium

reactors (under research and development, notably in India), and the

still-distant possibility of controlled, clean fusion power, which draws on the

energy of fusing hydrogen nuclei. Smaller scale fission reactors are also being

proposed.

In the case of breeder

reactors, a large scale prototype was built in southern France, but has

been closed for some years in the face of major technical and mechanical

problems. For fusion,

decades of research have yet to lead to a useful power reactor. Experimental

work continues in several locations, with the largest being a multinational

experimental fusion facility in France (ITER),

but this is at least ten years away from demonstrating commercial feasibility

of the technology. The ITER facility has not been designed to capture any

energy produced as electricity, but as an experimental unit to test and

demonstrate the technology. Smaller scale fission technologies are also under

active research, but have yet to be demonstrated. Advanced reactor designs are

the focus of the Generation IV

International Forum collaboration (which Australia joined

in 2016).

Prospects for Australia

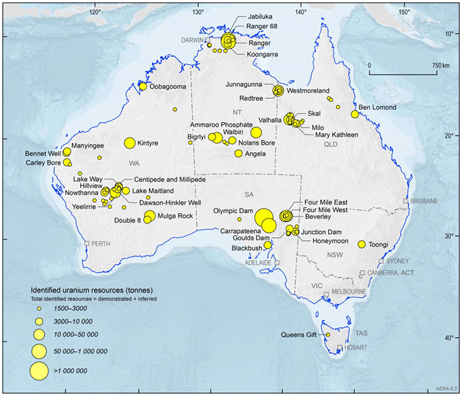

Australia holds almost one-third of the world’s proven

uranium reserves, which has underpinned

exports of around 7,000 tonnes per year. This represents about 10 per cent

of global supply and makes Australia the third-largest uranium producer.

Uranium ore is mined and processed into uranium oxide before being exported,

with no enrichment into nuclear fuel undertaken in Australia. There are three

operating uranium mines in Australia—Olympic Dam and Four Mile (South

Australia) and Ranger (Northern Territory).

Australia’s identified uranium resources

Source:

Geoscience Australia, Australian energy resources assessment, 2018

Nuclear power production is currently not permitted under

two main pieces of Commonwealth legislation—the Australian

Radiation Protection and Nuclear Safety Act 1998 (the ARPANS Act), and

the Environment

Protection and Biodiversity Conservation Act 1999 (the EPBC Act). These

Acts expressly prohibit the approval, licensing, construction, or operation of

a nuclear fuel fabrication plant; a nuclear power plant; an enrichment plant;

or a reprocessing facility. There is also a range of other legislation, including

state and territory legislation, which regulates nuclear and radiation-related activities.

In recent years, a number of inquiries have been undertaken

into nuclear issues in Australia. The Australian Parliament House of

Representatives Standing Committee on Environment and Energy held an inquiry

into the prerequisites for nuclear energy in Australia and reported

on 13 December 2019. The NSW

Parliament conducted an inquiry into uranium mining and the potential of

nuclear power in NSW (report

tabled in March 2020). The Victorian Parliament also has an inquiry into

nuclear prohibition (submissions closed in February 2020). South Australia held a Royal Commission

in 2015 and 2016 into expanding its nuclear industry.

Australia has one nuclear reactor at Lucas Heights (south of

Sydney). It is one of over 200

research reactors located around the world and is used chiefly for the

production of medical isotopes—it is not used to generate electricity. The

facility produces tens of cubic metres of low and intermediate level

radioactive waste each year. Despite efforts over some decades, a permanent

repository has yet to be developed for this waste, which is currently held at

Lucas Heights, Woomera, and other sites. Australia is currently working to

establish a National

Radioactive Waste Management Facility for the permanent storage of low-level

waste from nuclear medicine and research activities and the temporary storage

of intermediate-level waste. This is progressing under the National

Radioactive Waste Management Act 2012. The Government has identified a

site near Kimba in South Australia to host the facility and this selection has gone

before Parliament in the National

Radioactive Waste Management Amendment (Site Specification, Community Fund and

Other Measures) Bill 2020.

In almost all OECD markets, new nuclear reactors have

struggled to establish a business case in the last two decades (with the

exception probably being South Korea). The long lead times and high capital

costs, plus the technical and economic inflexibility of nuclear plants, have

mitigated strongly against new construction unless there has been sufficiently

strong policy support (such as for the proposed new reactor in the United

Kingdom). New power plants over the last two decades in OECD countries have

generally been gas fired (based on high-efficiency gas turbines) and more

recently based on new renewable technologies, such as wind and solar, where costs

have declined sharply and lead times are short and costs known more accurately.

Experience in other countries where nuclear reactors are

introduced indicates that initially costs and lead times may exceed

expectations. A skilled work force is required to construct, operate and

maintain the facilities. In addition, any reactor construction in Australia

would likely need to be in a coastal location to assure cooling water. In due

course, a permanent repository for high-level reactor waste would need to be

identified, constructed and operated, quite distinct from current efforts to

develop a repository for low and intermediate level waste. The example of the United

Arab Emirates, where a Korean consortium is building four reactors, may

prove instructive in how a modern nuclear industry could function.

Further reading

International Atomic Energy Agency, ‘Power Reactor Information System’

International Energy Agency, World Energy Outlook

For copyright reasons some linked items are only available to members of Parliament.

© Commonwealth of Australia

Creative Commons

With the exception of the Commonwealth Coat of Arms, and to the extent that copyright subsists in a third party, this publication, its logo and front page design are licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Australia licence.

In essence, you are free to copy and communicate this work in its current form for all non-commercial purposes, as long as you attribute the work to the author and abide by the other licence terms. The work cannot be adapted or modified in any way. Content from this publication should be attributed in the following way: Author(s), Title of publication, Series Name and No, Publisher, Date.

To the extent that copyright subsists in third party quotes it remains with the original owner and permission may be required to reuse the material.

Inquiries regarding the licence and any use of the publication are welcome to webmanager@aph.gov.au.

This work has been prepared to support the work of the Australian Parliament using information available at the time of production. The views expressed do not reflect an official position of the Parliamentary Library, nor do they constitute professional legal opinion.

Any concerns or complaints should be directed to the Parliamentary Librarian. Parliamentary Library staff are available to discuss the contents of publications with Senators and Members and their staff. To access this service, clients may contact the author or the Library‘s Central Entry Point for referral.