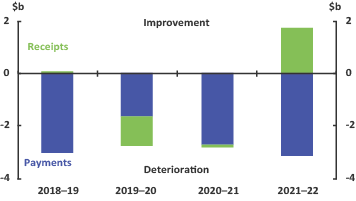

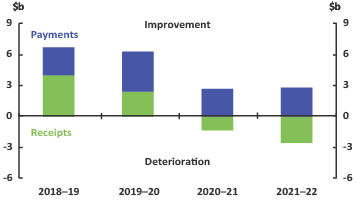

Figure 7: Policy decisions - payment and receipts2,4,8

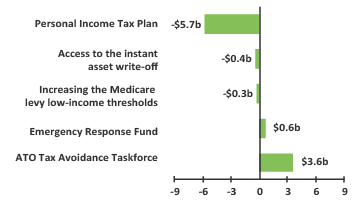

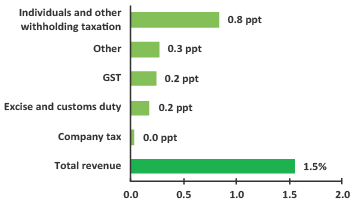

Figure 8: Top 5 revenue measures5,6,13,14

Total, 2018–19 to 2022–23

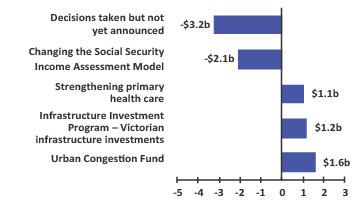

Figure 9: Top 5 expense measures5,6,14,15

Total, 2018–19 to 2022–23

Figure 10: Parameter and other variations - payments and receipts2,7,9

Figure 11: Contributions to annual real growth in revenue5,10

Average, 2018–19 to 2022–23

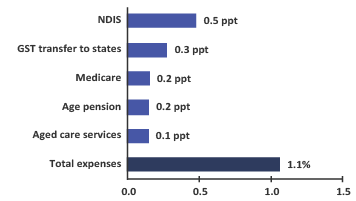

Figure 12: Contributions to annual real growth in expenses5,11

Average, 2018–19 to 2022–23