Executive

summary

Derivatives are powerful financial instruments that play

an important role in the capital markets. If they are mispriced or

underregulated, they can amplify underlying systemic risks in the global

financial system.

In 2003 Warren Buffett described derivatives as ‘financial

weapons of mass destruction’. The 2008 Global Financial Crisis arguably proved

the truth of his words because mispriced derivatives contributed to the

systemic risks in the global financial system that eventually caused the

crisis.

The 2008 crisis prompted a comprehensive international

regulatory response, directed through the G20 forum (including

Australia).[1] Since 2009 Australian regulators have been implementing the G20 reforms to

improve transparency in the derivatives market.[2]

Notwithstanding the G20 reforms on derivatives trading, some

analysts fear that major international banks are becoming too exposed to

mispriced derivatives once again.[3] Furthermore, the strengthening of prudential regulations on banks (as outlined

by Basel III) meant that the banks might find it cheaper to shift risk using

derivative contracts.[4] This has sparked a public debate on whether there is sufficient government

regulation of derivatives trading in Australia and other countries.[5]

As an open economy Australia is vulnerable to global risks that

could trigger a ‘liquidity

crunch’ or a reduction in international trade. This has implications for

legislative changes implementing the G20 reforms, the resourcing and

effectiveness of Australian regulatory agencies supervising derivatives trading

and Australia’s engages with international partners in monitoring the progress

of G20 reforms on the derivatives market.

What is a financial derivative?

A derivative is a contract between two parties that derives

its value from the performance of an underlying asset. The underlying asset can

be almost anything of value (most commonly commodities, stocks and bonds).

There are many types of derivatives. Traditional forms of

derivatives such as options and forward contracts (illustrated in the example

below) have existed for hundreds of years. Newer and more complex derivatives

such as collateralised debt obligations or credit default swaps have grown

enormously in recent decades, and now constitute a multi-trillion dollar

worldwide market.[6]

Why do investors and firms use derivatives?

Derivatives are risk management tools. Investors and firms

use derivatives primarily for two reasons:

- to hedge against future price

movements, reducing uncertainty; or

- to speculate on future price

movements, accepting greater risk exposure in exchange for the chance of

greater profit. [7]

Using derivatives to hedge

Derivatives can make future cash flows more predictable, so

many investors and firms use them to hedge against potential risk. In this

regard, using derivatives is like buying an insurance policy that protects the

investor against price uncertainty.

Using derivatives to speculate

Investors who are prepared to accept additional risk often

use derivatives as a speculative tool. The purpose of speculation is to make a

profit from betting that the prices of assets will move in a favourable

direction. Complex derivatives allow investors to speculate on virtually

anything.

What role do derivatives play in the financial markets?

Derivatives serve an important ‘price discovery’ role in the

economy as they can be used for establishing the prices of goods and services.

When used as a hedge, derivatives provide investors with predictable cash flows

and limit their risk exposure. Trading derivatives as a speculative tool can

also provide liquidity and price signals in the financial markets.

Derivatives trading has opened up a wide array of financial

markets for investors. For example, an Australian investor can speculate on the

price of American soybeans or the value of the Canadian dollar by using

derivatives.

On the other hand, mispriced and unregulated derivatives can

pose a risk to the global financial system, as

happened in the 2008 Global Financial Crisis.

How did mispriced derivatives contribute to the Global

Financial Crisis?

The rise of collateralised debt obligations

Professor

Michael Greenberger of the University of Maryland, among many others,

believes that the extensive misuse of derivatives

amplified the 2008 Global Financial Crisis – in particular, through the use of

a type of derivative known as collateralised debt obligations (CDOs).[9]

CDOs

grew in popularity in the United States in the early 2000s, with CDO

sales increasing from US$30 billion in 2003 to US$225 billion in 2006.[10] According to the Reserve Bank of Australia, global CDO issuance increased

sixfold from 2002 to 2006 (see Figure 1 below).

Figure 1: Issuance of CDOs increased significantly in the early 2000s

Source:

Susan Black and Alan Rai, ‘Recent Developments in Collateralised Debt Obligations

in Australia’, Reserve Bank of

Australia Bulletin (November 2007): 5.

Fuelled by a housing market boom

and an increase in mortgage uptake in the United States in the early 2000s,

banks made handsome profits by packaging various types of loans into CDOs and

selling them to investors.[11] This was usually done via a subsidiary company called a special purpose vehicle to shield the parental company from financial risk.[12]

There is a broad academic

consensus that CDOs were frequently overvalued prior to 2008.[13] Additionally, the extent of banks’ exposure was opaque due to the complexity of

these derivatives, so the extent of systemic risk went unnoticed.[14] Banks held CDOs on their ‘books’ before selling them to other investors (for

example, pension funds). Banks also invested in each other’s CDOs. As such, the

banking sector as a whole was financially exposed to a collapse in CDO value.

These problems were compounded by

credit rating agencies’ underestimation of CDOs’ real risk.

Misconduct of credit rating agencies

Many academics, such as Professor Lawrence White of the New

York University, argued that the misconduct of credit rating agencies contributed to the overvaluation of CDOs.[15]

Credit rating agencies are typically private companies paid

by banks or investors to assess the risk levels of

financial products. This includes determining the value and risk levels

of derivatives – for example, in the 2000s, whether CDOs were backed by

high-grade or subprime/riskier loans. However, for fear of losing their

customers (including banks that wanted to sell CDOs), credit rating agencies

often gave good credit ratings to CDOs backed by subprime/riskier loans.[16]

For example, some of the loans that were packaged into CDOs

were known as NINJA (no income, no job, no assets) loans that carried a high

risk of default.

These inflated credit ratings

meant that many CDOs were overvalued. Buyers of CDOs were unaware of the

default risk that these derivatives carried and assumed they were a good

investment. Put simply, CDOs were no longer an effective risk management tool

(which is the main purpose of derivative contracts) because investors were

unaware of the real risk CDOs carried.

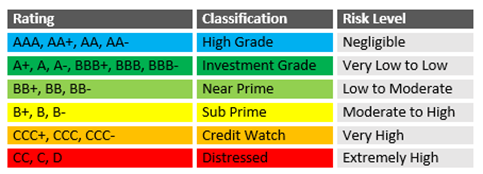

The table below shows examples of credit ratings and their

corresponding risk levels.

Table 1: examples of credit ratings and their supposed risk level

Source:

‘Equifax Credit Ratings’, Equifax Australasia

Credit Ratings Pty Ltd.

Regulation of derivatives trading prior to 2008

Despite sales of CDOs increasing exponentially in the early

2000s, CDO trading remained largely unregulated in the United States.

CDOs had traditionally been privately negotiated and traded

between 2 parties without going through a centralised

clearing exchange. Such privately negotiated derivatives are known as ‘over-the-counter’

(OTC) derivatives.[17] Many officials in the United States Government at the time believed that

because OTC derivatives were mostly negotiated between sophisticated investors

who knew what they were getting into, derivatives trading needed less

regulation compared to other financial products.[18]

In 1998, the former Federal Reserve Chairperson Alan

Greenspan told Congress that ‘regulation of derivatives transactions that are

privately negotiated by professionals is unnecessary’.[19] In 2000, Congress passed the Commodity

Futures Modernization Act that excluded derivatives trading from regulatory

oversight.[20]

Had CDO trading been conducted through centralised clearing

exchanges, United States regulators may have had an easier time overseeing the

derivatives market and stopping questionable trading practices.[21] Instead, the private, bilateral nature of OTC derivatives meant there was a

lack of transparency concerning the risk profile of market participants in the

derivatives markets.[22]

Building a ‘house of cards’

In 2005 Professor Raghuram Rajan, the former Chief Economist

at the International Monetary Fund, warned that perverse incentives (coupled

with the wrong monetary policy) could lead banks and investment firms to take

excessive risks.[23]

There were strong incentives for investment managers at

banks and investment firms to generate profits because their pay or bonuses

were largely performance based. As such, Professor Rajan was concerned that

managers were incentivised to use innovative financial instruments, like

derivatives, to take excessive risks with company money in the hope of

generating high returns, which could then lead to a ‘catastrophic meltdown’ of

the financial system.[24]

Professor Nouriel Roubini of New York University described

the perverse incentive culture of investment managers:

People were essentially being rewarded for taking massive

risks. In good times, they generate short-term revenues and profits and

therefore bonuses. But that’s going to lead to the firm to be bankrupt over

time. That’s a totally distorted system of compensation.[25]

In the early 2000s, major banks traded an increasing number

of mortgage-backed securities (MBSs) and derivative contracts that repackaged

MBSs. This increased their short-term profits but also significantly increased

their risk exposure, partially because they had incorrectly assessed the risk

levels of the derivatives.[26]

Put simply, derivatives were one of the financial tools

that allowed investment managers to take on excessive financial risks (for the

purpose of generating short-term revenues) without tipping off the regulatory

authorities.

In addition to CDOs, banks and investors used other complex

derivatives such as synthetic CDOs and credit default swaps (CDSs) to make ‘side

bets’ speculating on whether the value of CDOs would rise or fall.[27]

Banks and investors used CDSs to

hedge against the potential risk of loan default. While this decreased the risk

exposure of investors, it significantly increased the risk exposure of major

insurance companies.

American International Group (AIG),

one of the world’s largest insurance companies, was a prolific underwriter and

seller of CDSs. Many investors purchased AIG’s CDSs because they had lent out

money and wanted to be compensated if the loans went bad. Many speculators, who

were not themselves parties to the loans, also purchased CDSs to speculate that

the loans would go bad.

As OTC derivative markets were largely unregulated, in

theory AIG could underwrite and sell unlimited CDSs even if it did not have

enough collateral to pay out the CDSs when loans went bad.

In 2008, the New York Times featured an

article that reported AIG’s Financial Products Division had underwritten

and sold CDSs worth $500 billion (US dollars), and that the company was receiving

as much as $250 million a year in income from CDS ‘insurance premiums’.[30] Many of these CDSs were to provide insurance to financial institutions holding

CDOs, in case loan borrowers defaulted.

In other words, the investment managers at AIG took

excessive risks and miscalculated the chance of a mass loan default, and

therefore grossly mispriced the CDSs they had underwritten.[31]

It is unclear whether the senior executives of the AIG knew

the company had sold CDSs in excess of its ability to pay out in the event of a

mass loan default. Nevertheless, the investment managers’ focus on short-term

gains and a lack of regulatory oversight meant that very few people at AIG had

the incentives to speak out against excessive risk-taking.

Through holding a large volume of mispriced derivatives

on their balance sheets, major banks and insurance companies became extremely

exposed to the potential risk of a mass default on subprime mortgages and other

related loans.

Professor

Frank Partnoy of the University of California explained how derivatives

amplified risk exposure, spreading it throughout financial markets:

If you were a homeowner with a risky subprime mortgage loan,

CDO arrangers might put together a hundred side bets on whether you would

default. Through credit default swaps, a hundred investors around the world

could be exposed to the risk that you might not make your next monthly

payments.[32]

The collapse of a ‘house of cards’

It is worth repeating that a derivative contract derives its value from an underlying asset, with the asset underlying a CDO in the

cases above being an income stream from subprime mortgage repayments. If this

asset becomes worthless – for example because the borrower defaults on the loan

– then the derivative CDO also becomes worthless.

When the American housing market slowed down in 2007–08

after a two-decade housing boom, many mortgage holders started to default on

their loans, and the number of home foreclosures increased substantially.[33] It became increasingly evident that the value of CDOs reliant on subprime

mortgage repayments had been vastly overstated.

While some banks did not know the exact extent of the losses

they faced from holding these overvalued CDOs, other banks actually attempted

to sell overvalued CDOs to unsuspecting investors to mitigate their losses.[34] The resulting fear and uncertainty made banks and investors reluctant to lend

money, contributing to a global ‘liquidity

crunch’ that exacerbated the 2008 Global Financial Crisis.[35]

To ‘bail out’ AIG and some major banks, the United States

Government implemented the Troubled Asset Relief Program to purchase up to $700

billion in distressed assets from these companies to keep them solvent.[36]

In 2009, President Barack Obama said:

Under these circumstances, it's hard to understand how

derivative traders at AIG warranted any bonuses, much less $165 million in extra

pay. How do they justify this outrage to the taxpayers who are keeping the

company afloat?[37]

Regulation of

derivatives trading in Australia

Why is regulation of derivatives trading so challenging?

Regulation of derivatives trading is challenging because

governments may not always have adequate information on the derivatives market.

Economist Vania Stavrakeva argues:

Derivatives are much more complicated contracts than regular

loans, bond and equity purchases and have very different accounting standards.

In order to estimate the exposure of banks to systemic crises caused by

derivative positions, regulators will need both bank specific transaction level

data and fairly complex value at risk models …

Of course one should not forget that derivatives can also

improve welfare by allowing firms and financial institutions to hedge risk and

by improving risk sharing. Therefore, one needs to be careful not to

overregulate.[38]

Implementation of G20 reforms

The 2008 Global Financial Crisis prompted a comprehensive international

regulatory response, directed through the G20 forum (including Australia).[39] G20 leaders agreed in September 2009:

All standardised OTC derivative contracts should be traded on

exchanges or electronic trading platforms, where appropriate, and cleared

through central counterparties by the end of 2012 at the latest. OTC derivative

contracts should be reported to trade repositories. Non-centrally cleared

contracts should be subject to higher capital requirements.[40]

As noted, the lack of data on derivatives trading has made

it more difficult for regulatory agencies to adequately supervise the

derivatives market. Before the 2008 global financial crisis, regulators in

Australia generally only had access to highly aggregated data to understand the

OTC derivatives market, and the 2008 crisis highlighted that these aggregated

data are ‘insufficient to shed light on the vulnerabilities that can exist when

there is a web of derivative transactions between a large variety of firms’.[41]

Consequently, the Australian Government has introduced a

suite of legislative

changes designed to improve transparency and reduce systemic risk

associated with derivatives trading. The legislative changes also align with

Australia’s commitment to implement the Basel III agreement that prescribes banks’ capital and liquidity requirements for

derivatives transactions.

For examples, the Corporations

(Derivatives) Determination 2013 empowers the Australian Securities and

Investments Commission (ASIC) to make rules imposing reporting requirements on

a range of derivatives.[42] The ASIC

Derivative Transaction Rules (Reporting) 2013 set out the rules for reporting

derivative transactions to trade repositories. The ASIC

Derivative Transaction Rules (Clearing) 2015 impose a mandatory central

clearing regime for OTC interest rate derivatives denominated in major currencies.

These reforms have greatly increased the information

that regulators have about the Australian derivatives market.[43]

On the other hand, some stakeholders warn the risks of

overregulation, especially considering that the COVID-19 pandemic placed

significant operational burden for market participants. For example, the

brokerage firm Pepperstone has said:

… we are concerned that some of the requirements in CP

322 are overly stringent, and do not allow for investors who understand and

accept the risks associated with trading our products to trade the way they

require. We are concerned that this restriction on investors’ freedom of choice

will result in them seeking alternatives outside of Australia, even if it means

trading outside of a regulated jurisdiction. [44]

Multilateral cooperation

Although Australian regulators have been implementing G20

reforms to reduce systemic risks in the financial sector, as an open economy

Australia remains exposed to risks in the world economy. As such, Australia has

an interest in promoting multilateral efforts to strengthen the international

institutions and mechanisms needed to manage these risks.

Australia is a member of the Financial Stability Board (FSB), an international body that monitors the

stability of the global financial system and publishes an annual

progress report on the implementation of OTC derivatives reforms. Since

2009 Australian regulators have worked with other members of the FSB to resolve

cross-border issues that have arisen in the implementation of OTC derivatives

reforms.[45]

Derivatives trading in the 2020s

Bespoke CDOs

Today, derivatives trading is widespread and accessible. An

increasing number of equity and even cryptocurrency exchanges are offering a

wider range of derivatives.[46] According to a report

by the World Federation of Exchanges, more than 32 billion derivative

contracts were traded in 2019.[47]

Trading volumes in CDOs decreased significantly after 2008.[48] However, more recently, banks have once again been increasing their CDO sales.

Due to CDOs’ negative connotations, banks have renamed these derivatives ‘bespoke tranche

opportunities’ or ‘bespoke CDOs’.[49] These new bespoke CDOs are predominantly purchased by hedge funds and other

institutional investors seeking higher returns.

In April 2019, Reuters reported that:

Trading volumes in synthetic

collateralised debt obligations linked to credit indexes are up 40% this year,

according to JP Morgan, after topping US$200bn in 2018 on the back of three

years of double-digit growth. Meanwhile, analysts predict more than US$100bn in

sales of bespoke synthetic CDOs in 2019 following an estimated US$80bn of

issuance last year.[50]

Banks have argued that the new bespoke CDOs are now backed

by safer loans rather than subprime mortgages.

Total return swaps

In March 2021, Bill Hwang, the founder of Archegos Capital

Management, used a type of OTC derivative known as a total return swap (TRS) to

indirectly invest in the US stock market. The TRS contracts significantly

increased Archegos Capital’s risk exposure, because TRSs are designed to allow

investors to trade on margin by using borrowed money (illustrated in the

example below).[51] Archegos Capital lost an estimated US$20 billion in 2 days and caused its

lenders to lose tens of billions.[52]

Because Archegos Capital was a

relatively low-profile family office, it was not subject to the same regulatory

scrutiny as major hedge funds. This allowed Archegos Capital to enter into TRS

contracts with 6 major investment banks simultaneously without disclosing to

any single bank or the regulatory authority that it had multiple TRS contracts

with other banks.[54] One commentator described Archegos Capital’s decisions as:

Imagine you go to four mates separately, borrow £1000 from

each without telling the other, and go to a casino and put it [sic] all that

money on red.[55]

In other words, the TRS allowed Archegos Capital to trade on

margin and take a highly leveraged position on selected stocks. When the stock

price fell and Archegos Capital could no longer afford to put up the collateral

to maintain its leveraged position, it caused a stock fire sale that further

depressed the stock price. This wiped billions of dollars off the stock market

and resulted in ‘one of the single greatest losses of personal wealth in

history’.[56]

The Financial Times featured an article that

commented on the potential destructive power of derivatives:

The Archegos Capital debacle has exposed the hidden risks

of the lucrative but opaque equity derivatives business through which banks

empower hedge funds to make outsize [sic] bets on stocks and related assets.

The soured wagers made by Bill Hwang’s family office have

triggered significant losses at Credit Suisse and Nomura, underscoring how

these tools can cause a chain reaction that cascades across financial markets.[57] [emphasis added]

The collapse of Archegos Capital has prompted financial

regulators around the world to investigate their risk control measures.[58] For example, the Financial Times reported that Hong Kong’s central bank

and financial regulator are planning to use centralised trade databases to

identify excessive risk-taking by banks and investment funds trading

derivatives on Hong Kong markets.[59]

Conclusion

Derivatives are powerful financial tools that can help

investors to manage risk and limit investment exposure. However, derivatives

can also lead to excessive speculative trading and significantly increase

investors’ risk exposure.

On a large enough scale, mispriced derivatives can endanger

the entire financial system. Like any other powerful tool, derivatives need to

be properly monitored and regulated. Consequently, it is important that

Australian regulatory agencies are effective in carrying out their supervision

of derivatives trading, complemented by continued promotion of multilateral cooperation

to implement derivatives market reforms.

Glossary

| Acronyms |

Definition |

| AIG |

American International Group |

| ASIC |

Australian Securities and Investments Commission |

| CDO |

Collateralised debt obligation |

| CDS |

Credit default swap |

| CLO |

Collateralised loan obligation |

| MBS |

Mortgage-backed security |

| OTC |

Over the counter |

| TRS |

Total return swap |