Key points

The Bills propose amendments to various foreign investment, taxation and superannuation law to:

- double the maximum financial penalties for contraventions of the relevant provisions relating to foreign ownership of residential land in Australia

- allow the Australian Taxation Office to share protected taxation information with an Australian government agency, for the purposes of administering major disaster support programs declared by the Minister

- extend, for a period of 12 months, a temporary mechanism for responsible Ministers to make alternative arrangements for meeting information and documentary requirements under Commonwealth legislation

- extend the current Seasonal Labour Mobility Program withholding tax regime to include the Pacific Australia Labour Mobility scheme, and any future similar temporary migration programs prescribed by the Government

- create a supplementary performance test for faith-based superannuation products.

Introductory Info

Date introduced: 8 September 2022

House: House of Representatives

Portfolio: Treasury

Commencement: Various dates as set out in the main body of the digest.

Purpose of

the Bills

The Treasury

Laws Amendment (2022 Measures No. 3) Bill 2022 (Main Bill) and the Income

Tax Amendment (Labour Mobility Program) Bill 2022 (Supporting Bill) amend

various foreign investment, taxation and superannuation laws for five separate

purposes.

- Schedule

1 (Main Bill) amends the Foreign

Acquisitions and Takeovers Act 1975 (FATA) to double the maximum

financial penalties for contraventions of the relevant provisions relating to foreign

ownership of residential land in Australia..

- Schedule

2 (Main Bill) amends the tax secrecy provisions in the Taxation

Administration Act 1953 (TAA) to allow a taxation officer to

disclose protected taxation information to an Australian government agency for

the purposes of administering a major disaster support program approved by the

Minister. The current law prohibits such a disclosure.

- Schedule

3 (Main Bill) amends the

- Coronavirus

Economic Response Package Omnibus (Measures No. 2) Act 2020 to extend, for

a period of 12 months, a temporary mechanism for responsible Ministers to make

alternative arrangements for meeting information and documentary requirements

under Commonwealth legislation. Schedule 3 is not covered in this Bills

Digest because it is adequately explained in the Explanatory

Memorandum to the Bills.

- Schedule

4 (Main Bill) and Schedule 1 (Supporting Bill) amend various tax

laws to:

- rename

the ‘Seasonal Labour Mobility Program withholding tax’ regime as the ‘labour

mobility program withholding tax’ regime

- extend

the current income tax treatment (including a 15% income tax rate) under the renamed

‘labour mobility program withholding tax’ to the new ‘Pacific Australia Labour

Mobility’ (PALM) scheme and any future temporary migration programs prescribed

by the Australian Government.

- Schedule

5 (Main Bill) amends the Superannuation

Industry (Supervision) Act 1993 to create a supplementary performance

test for faith-based superannuation products.

Committee

consideration

Senate

Standing Committee for the Selection of Bills

At the time of writing this Digest, the Senate Standing

Committee for the Selection of Bills deferred consideration of the Bills.[1]

Senate

Standing Committee for the Scrutiny of Bills

At the time of writing this Digest, the Senate Standing

Committee for the Scrutiny of Bills had not considered the Bills.

Statement

of Compatibility with Human Rights

As required under Part 3 of the Human Rights

(Parliamentary Scrutiny) Act 2011 (Cth), the Government has assessed the

Bill’s compatibility with the human rights and freedoms recognised or declared

in the international instruments listed in section 3 of that Act. The

Government considers that the Bill is ‘compatible with human rights because, to

the extent that it may limit human rights, those limitations are reasonable,

necessary and proportionate.’[2]

Parliamentary

Joint Committee on Human Rights

At the time of writing this Digest, the Parliamentary

Joint Committee on Human Rights had not considered the Bills.

Schedule 1

(Main Bill): Foreign acquisitions and takeovers penalties

Schedule 1 of the Main Bill seeks to double the financial

penalties for contraventions of provisions relating to foreign ownership of

residential land in Australia.[3]

Background:

rules relating to foreign ownership of residential land in Australia

The Foreign

Acquisitions and Takeovers Act 1975 (FATA) and other relevant

legislation regulate foreign investment in Australia in a manner consistent

with the Australian Government’s Foreign

Investment Policy.[4]

The FATA allows the Treasurer to review foreign investments proposed by

a foreign

person (which includes foreign corporations and governments) if the

investment meets certain thresholds based on the:

Whilst the Treasurer is ultimately responsible for all

decisions relating to foreign investment under the FATA, the Treasurer

is advised and assisted by the Foreign Investment Review Board (FIRB) which

administers the FATA in accordance with the Foreign Investment Policy.

The Australian Taxation Office (ATO) supports the FIRB by administering foreign

investment applications with respect to residential real estate.[6]

Under the FATA, a foreign person must seek foreign

investment approval before acquiring an interest in Australian residential land

and must comply with any relevant obligations imposed by the Treasurer.[7]

When considering an application for a foreign person to acquire an interest in

residential land, ‘the overarching principle is that the proposed acquisition

should add to Australia’s housing stock.’[8]

The FATA also contains specific penalties for contraventions of

residential land provisions.

In their 2020–21

annual report, the FIRB noted that 'as COVID-19 continued to cause economic

uncertainty and impact investor confidence, foreign direct investment inflows

declined across countries comparable with Australia’. The 2020–21 income year

saw a decline in the number of proposals, however, the total value of approved

investments increased from $195.5 billion in 2019–20 to $233.0 billion in

2020–21.[9]

What is the

problem?

In his second reading speech, the Assistant Treasurer, Mr

Stephen Jones, set out the Government’s rationale for the amendments contained

in Schedule 1 to the Bill:

Noncompliance with the residential land obligations by

foreign persons has flow-on implications for Australia's housing stock and

housing affordability.[10]

Research on the impact of the foreign investment in real

estate on housing prices in Australia between 2004 and 2014 suggests that:

… increases in foreign investment account for between 20% and

30% of the rise in housing prices between 2004 and 2014 in Sydney and

Melbourne. In other capital cities the effects appear to be negligible … foreign

investment only plays a moderate role in Australia’s property boom. This

implies that other factors such as CPI inflation, changes in domestic demand

and supply constraints are likely to account for much greater proportions of

the trends that we have observed, especially in cities outside of Sydney and

Melbourne…[11]

Further, research suggests that foreign investment in the

residential real estate sector is around 5–10% of the value of annual dwelling

turnover in Australia, and perhaps half that share of the total number of

dwellings turned over.[12]

The ATO is responsible for compliance and enforcement

activities for residential real estate, the vacancy fee and some commercial

land proposals.[13]

In 2020–21, the ATO reported that there were approximately 5,310 residential

real estate purchase transactions involving a level of foreign ownership.[14]

Out of the 5,310 purchases, there were 711 established dwellings, 3,644 new

dwellings and 955 vacant land.[15]

In the same period, there were 3,103 residential

real estate sale transactions by foreign persons, including the sales of

858 established dwellings, 1,415 new dwellings and 830 vacant land.[16]

The total number of residential real estate properties and land (including

purchases and sales) involving foreign persons was 8,413 in 2020–21.

The FIRB has reported the ATO’s investigations (and the

outcomes) into non-compliant residential land or property transactions by

foreign persons (see Tables 1 and 2 below). In 2020–21, the ATO identified

487 cases (including 126 cases carried forward from the previous year)

requiring investigation, completed 404 such investigations and found 100 properties

in breach of FATA, which is approximately 1.2% of the total number of

residential real estate involving foreign persons.[17]

Table 1:

Residential real estate compliance investigations by the ATO, 2018-19 to

2020-21

| |

2018‑19

|

2019‑20

|

2020‑21

|

| Investigations |

No. |

No. |

No. |

| Identified |

1,220 |

746 |

487 |

| Completed |

1,068 |

620 |

404 |

| Properties in breach |

600 |

259 |

100 |

The total number of identified cases includes new cases

identified in the prior financial year which remained open at the end of that

financial year. In 2020-21 there were 126 cases carried forward from 2019-20

year included in the identified count. At the close of the 2020-21 year there

were 83 cases that will be carried forward into 2021–22.

Source: FIRB, Annual Report, 2020-21, Table 4.5, 46.

Table 2: Outcomes

of residential real estate investigations that identified breaches, 2018-19 to

2020-21

|

2018‑19

|

2019‑20

|

2020‑21

|

| Compliance outcome |

No. |

Percentage |

No. |

Percentage |

No. |

Percentage |

| Divestment (a) |

83 |

13.8 |

70 |

27 |

57 |

57.0 |

| Retrospective approval (b) |

79 |

13.2 |

49 |

18.9 |

24 |

24.0 |

| Change of conditions (c) |

220 |

36.7 |

57 |

22 |

2 |

2.0 |

| Retrospective approval during FIRB consideration (d) |

213 |

35.5 |

62 |

23.9 |

17 |

17.0 |

| Vacancy fee raised* |

5 |

0.8 |

21 |

8.1 |

– |

– |

| Total outcomes |

600 |

100 |

259 |

100 |

100 |

100.0 |

* Refers to situations where a compliance review was undertaken

following the lodgement of a vacancy fee return and a vacancy fee liability was

raised for a dwelling that was found to be occupied for fewer than 183 days

during a vacancy year.

Source: FIRB, Annual Report, 2020-21, Table 4.6, 47.

Table 3: Infringement

notices issued in relation to residential real estate, 2018-19 to 2020-21

|

2018‑19

|

2019‑20

|

2020‑21

|

| Penalty type |

No. |

Total value $ |

No. |

Total value $ |

No. |

Total value $ |

| Tier 1 infringement |

346 |

1,288,000 |

140 |

499,360 |

37 |

375,336 |

| Tier 2 infringement |

169 |

2,267,320 |

36 |

804,600 |

20 |

1,217,040 |

| Total |

515 |

3,555,320 |

176 |

1,303,960 |

57 |

1,592,376 |

Tier 1 infringement notices are issued where the

breach is self–reported.

Tier 2 infringement notices are issued where the

breach is identified by the ATO’s compliance activity.

Source: FIRB, Annual Report, 2020-21, Table 4.9, 49.

Further statistics on foreign ownership of Australian

residential property or land are provided in Appendix A of this Digest.

The ATO has stated that its compliance approach:

- ‘recognises

that most foreign investors are willing to do the right thing and meet their

foreign investment obligations’

- ‘acknowledges

there is a small proportion that either don’t want to comply or have decided

not to.’[18]

Where breaches of the FATA are investigated, a

range of enforcement measures, including litigation, can be applied. In this

regard the ATO notes:

In 2022, we welcomed the decision handed down by the Federal

Court of Australia in relation to breaches of the FATA.

Using sophisticated compliance data-matching systems, our

investigations into tax evasion and fraud identified several concerning

activities by some investors.

In this instance, an individual investor purchased

4 properties without first applying for and receiving FIRB approval. The

investor also held 2 established residential properties. These actions are

considered serious breaches of the law and warranted a 'high touch' approach in

treatment.

The landmark decision handed down in the Federal Court

attracted penalties of $250,000. It sent a strong message to investors on the

importance of understanding and complying with their foreign investment

obligations. See Federal Court’s decision in Commissioner

of Taxation v Balasubramaniyan [2022] FCA 374 (8 April 2022).[19]

What is the

proposed solution?

The Government made an election commitment to ‘increase foreign investment fees and penalties’.[20]

The amendments to the

Foreign

Acquisitions and Takeovers Fees Imposition Regulations 2020 made by the

Government on 29 July 2022 doubled the fee amounts, implementing the fee

component of that commitment.[21]

The Foreign

Acquisitions and Takeovers Fees Imposition Amendment Bill 2022 (not

examined in this Digest) makes additional changes, in relation to the way the

relevant fees are indexed.[22]

Schedule 1 to the Main Bill implements the

penalty component of the Government’s 2022 election commitment for residential

land only. In his second reading speech on the Bill, the Assistant Treasurer

advised:

This increase to residential penalties will ensure that these

penalties effectively deter foreign persons from contravening the residential

land provisions in the Foreign Acquisitions and Takeovers Act 1975.[23]

Key provisions

As discussed earlier, the Government has expressed concern

about the effect of non-compliance with Australia’s foreign investment laws by

temporary or foreign residents on Australia’s housing stock and affordability,

despite available evidence suggesting high rates of compliance.

As such, the key issue that Schedule 1 to the Main

Bill attempts to address is ensuring that the applicable penalties ‘effectively

deter foreign persons from contravening the residential land provisions in the FATA’

and ‘will deter and punish illegal behaviour’.[24]

It is further noted that

‘Residential land is land in Australia where there is at

least one dwelling on the land (or the number of dwellings that could

reasonably be built on the land is less than 10) and does not include land that

is used wholly and exclusively for a primary production business or on which

the only dwellings are commercial residential premises.’[25]

Penalties (including infringement notices, civil and

criminal penalties) may apply for breaches of the FATA in relation to

residential land.[26]

For breaches occurring on or after 1 July 2020, the current value of a penalty

unit is $222 – meaning that 100 penalty units, for instance, equals $22,200.[27]

Schedule 1 to the Main Bill deals with three groups

of penalties:

- financial

penalties for criminal offences relating to developers selling a dwelling to a

foreign person without advertising the dwelling in Australia

- civil

penalties relating to residential land acquisitions by foreign persons in

particular circumstances

- civil

penalties relating to failures by a foreign person to lodge tax returns, keep

various records and provide various notices.

The proposed changes will increase the penalty units for

following three groups of penalties by 100%, as set out in Table 4

below.

Table 4: Increased

penalties for breaches of the FATA

| FATA section |

Prohibited conduct |

Current penalty |

Proposed penalty |

| Group 1: Penalties for criminal offence provision

relating to developers |

|

88

|

A person is a developer and sells a new dwelling to a

foreign investor without complying with a condition in an exemption

certificate to advertise the dwelling in Australia.

|

- imprisonment

for 10 years

- 15,000

penalty units (150,000 penalty units if the developer is a corporation)

or both[28]

|

- imprisonment

for 10 years

- 30,000

penalty units (300,000 penalty units if the developer is a

corporation)

or both[29]

|

| Group 2: Civil penalties

relating to real estate acquisitions by foreigners |

|

94

|

A foreign person fails to notify the Treasurer before

acquiring an interest in residential land or acquires the residential land

before the relevant time period specified in section 82.[30]

|

The greatest of:

- the

amount of the capital gain that was made or would be made on the disposal of

the relevant residential land or established dwelling

- 25% of

the consideration of the relevant residential land or established dwelling and

- 25% of

the market value of the relevant residential land or established dwelling[31]

|

The greatest of:

- double

the amount of the capital gain that was made or would be made on the

disposal of the relevant residential land or established dwelling

- 50%

of the consideration of the relevant residential land or established dwelling

and

- 50%

of the market value of the relevant residential land or established dwelling[32]

|

|

95

|

A temporary resident breaches the rules by holding an

interest in more than one established dwelling at the same time unless an

exception applies. A foreign person, who is not a temporary resident,

breaches the rules by acquiring an interest in an established dwelling,

unless an exception applies.

|

|

95A

|

A foreign person fails to comply with a national security

call-in notice from the Treasurer relating to residential land (for example,

prohibiting an acquisition of residential land while a national security

review is completed).[33]

|

|

96

|

A foreign person contravenes a condition in a no objection

notification, notice imposing conditions or exemption certificate relating to

a residential land acquisition (for example, requiring a purchaser of vacant

land to begin to build a dwelling before a particular time).[34]

|

| Group 3: Civil penalties relating to failures by a

foreign person to lodge tax returns, keep various records and provide various

notices |

| 97 |

A foreign person fails to notify of an approved

acquisition or sale, or fails to

advertise the sale in Australia.[35] |

A maximum civil penalty of 250 penalty units[36] |

A maximum civil penalty of 500 penalty units[37] |

| 115D |

A foreign person fails to lodge a vacancy fee return

on-time.[38] |

| 115DA |

A foreign person provides a false or misleading vacancy

fee return. |

| 115G |

A foreign person fails to keep records. |

Source: As per footnotes above.

When do the

changes commence?

The amendments made by Schedule 1 to the Main Bill will

commence on 1 January 2023 and will generally apply to contraventions of the

relevant provisions that occur on or after 1 January 2023.

However, the increase to the civil penalty for

contraventions of subsection 95(1) (which prohibits a temporary resident from

holding an interest in one or more established dwelling at the same time) will also

apply to contraventions that started before 1 January 2023 and continue after 1

January 2023.[39]

The Explanatory Memorandum sets out the Government’s justification for these

amendments to apply retrospectively:

A higher penalty for a continuing contravention of subsection

95(1) reflects the seriousness of continuing to contravene the provision and

will better deter temporary residents from continuing to hold an interest in

multiple established dwellings, which has a direct impact on Australia’s

housing market.[40]

Policy

position of non-government parties/independents/major interest groups

At the time of writing, non-government parties,

independents and major interest groups had not commented publicly on the

measures contained in Schedule 1.

Financial

implications

The Government estimates that this

measure will increase receipts by $2.3 million over the four years

from 2022–23.

All figures in this table represent amounts in $m, rounded

to the nearest $0.1m each year.[41]

| 2022-23 |

2023-24 |

2024-25 |

2025-26 |

| 0.3 |

0.7 |

0.7 |

0.7 |

Source: Explanatory Memorandum, 1.

Schedule 2

(Main Bill): Data sharing to support government responses to major disasters

Schedule 2 to the Main Bill amends tax law secrecy

provisions to allow certain tax information about taxpayers to be disclosed to

Australian government agencies for the purposes of administering major disaster

support programs approved by the Minister.

Background

One of the barriers identified by the Royal

Commission into National Natural Disaster Arrangements for accessing

financial assistance for recovery from a disaster was ‘the inability, or

perceived inability, of different levels of government, organisations, and

non-government organisations to share information with each other’ (page 466).

What is the

problem?

The current tax secrecy provisions within Schedule 1 to

the Taxation

Administration Act 1953 (TAA) prohibit a taxation officer from disclosing

protected information acquired as a taxation officer to an Australian

government agency for the purpose of administering a major disaster support

program.[42]

Such disclosure is an offence and can attract a maximum penalty of 2 years imprisonment.[43]

This can slow down the administration of such programs by, for example, slowing

down the verification of an applicant’s eligibility to access a range of

support payments.

Protected information is information that

was disclosed, or obtained under, or for the purposes of a taxation law, and:

- relates

to the affairs of a taxpayer and

- identifies,

or is reasonably capable of being used to identify, the taxpayer.[44]

Examples of ‘protected information’ include details about

the income tax and related liabilities of a taxpayer and of assets and

liabilities disclosed to the ATO for the purposes of settlement negotiations.[45]

There are exceptions to the general offence.[46]

For example, a taxation officer can disclose protected information

to certain government organisations (such as ASIC, APRA, Industry Innovation

and Science Australia, the ACNC and Services Australia) for certain specified government

purposes.[47]

However, disclosure of protected information to an Australian

government agency for the purpose of administering a major disaster support

program is not currently a specified government purpose.

What is the

proposed solution?

Schedule 2 to the Main Bill proposes to amend the

tax secrecy provisions to allow the ATO to disclose or record protected information

with an Australian government agency, for the purposes of administering a major

disaster support program as declared by the Minister by legislative

instrument. The amendments in Schedule 2 to the Main Bill aim to reduce red

tape related to major disaster support programs to improve the

timeliness of major disaster recovery efforts.

In his

second reading speech on the Bill, the Assistant Treasurer advised:

The sharing of [protected] taxation information will only be

authorised if the Treasurer [or Minister] is satisfied that the [major disaster

support] program supports individuals and businesses affected by a major

disaster.[48]

The Explanatory Memorandum states that the amendments:

… will assist Australian government agencies to address the

needs of individuals and businesses significantly disrupted by a major disaster

event more efficiently and effectively and reduce the risk of those individuals

and businesses receiving inadequate or inappropriate support.[49]

The proposed amendments will allow for disclosures for the

purpose of any compliance action undertaken by the agency administering the

disaster support program.[50]

Key provisions

Schedule 2 to the Main Bill adds a new exception to

the tax secrecy provisions in Division 355 of Schedule 1 to the TAA. The

new exception will allow (but does not require) a taxation officer to disclose or

record protected information to an Australian Government agency for the purpose

of administering a major disaster support program declared by the Minister.[51]

Under proposed section 355-66 in Schedule 1 to the TAA,

the Minister can declare a program to be a major disaster support program

by making a legislative instrument.[52]

The Minister can make the declaration when a program administered by an Australian

government agency is in effect responding to the impacts of an event that:

- has

developed rapidly and resulted in the death, serious injury or other physical

suffering of large number of individuals or

- has

developed rapidly and resulted in widespread damage to property or the natural

environment or

- relates

to an emergency which has been declared, or no longer in force, under the National Emergency

Declaration Act 2020 (the NED Act 2020);[53]

and the program is directed at supporting individuals

significantly impacted by the event or ‘businesses’ the operations of which the

event has significantly disrupted.[54]

The Minister needs only be satisfied that the program

meets the eligibility criteria, and the program ‘does not need to explicitly

address the criteria’.[55]

In relation to this, the Explanatory Memorandum notes:

2.19 A program that is directed entirely at supporting

other entities or activities (such as not-for-profit organisations or employees

who would not otherwise be eligible for support as an individual) would not be

able to be the subject of a declaration. However, a program that applies to

different types of entities could still be characterised as being directed at

businesses if it substantially relates to supporting business entities. For

example, a program that is directed at supporting businesses but also supports

not-for profit organisations that are not also characterised as businesses

could be a program that is directed at supporting businesses.[56]

A declaration made by the Minister under proposed

subsection 355-66(1) must specify the period for which the declaration is

in force, which cannot be more than 2 years.[57]

To support the amendments, Schedule 2 makes a

consequential amendment to the definition of ‘national emergency law’ in the NED

Act 2020, so that proposed section 355-66 in Schedule 1 to TAA

is also a national emergency law.[58]

When do the

changes commence?

The amendments made by Schedule 2 to the Main Bill will

commence on the day after Royal Assent and apply in relation to records and

disclosures of information made on or after the commencement of the amendments,

whether the information was obtained before, on or after that commencement.[59]

Policy

position of non-government parties, independents and major interest groups

At the time of writing, non-government parties,

independents and major interest groups had not commented publicly on the

measures contained in Schedule 2.

Financial

implications

The Government has stated that the Bill will have no

financial impact.[60]

Schedule 4 (Main Bill): Tax treatment for certain new or

revised visa programs

A Bills

Digest was written for two lapsed Bills introduced by the previous

Government (the Treasury

Laws Amendment (Enhancing Tax Integrity and Supporting Business Investment)

Bill 2022 and the Income

Tax Amendment (Labour Mobility Program Bill) 2022) before the 46th

Parliament was dissolved for the May 2022 Federal Election and is complementary

to the current Digest.[61]

(See Appendix B to this Digest for further detail).

Background

Starting from 4 April 2022, the Pacific Australia Labour Mobility

(PALM) visa scheme has become the primary temporary migration program to

address unskilled, low-skilled, and semi-skilled workforce shortages in rural

and regional Australia among all sectors of the economy.[62]

The PALM scheme is built on strong partnerships among

Australia, Pacific Island nations and Timor-Leste.[63]

The ten participating countries include Fiji, Kiribati, Nauru, Papua New

Guinea, Samoa, Solomon Islands, Timor-Leste, Tonga, Tuvalu and Vanuatu.[64]

The PALM scheme consolidated, reformed and replaced

the previous two Pacific worker visa

programs, namely the

While the SWP or PLS visa streams will no longer be

available from 4 April 2022, workers who have already been granted or submitted

these visas before 4 April will be able to arrive and remain in Australia on

those visas.[66]

That means the SWP, PLS and the new PALM schemes will exist concurrently for

some time.

Current taxation arrangements for non-residents workers

generally

Under Australia’s tax laws, only tax residents can

access the tax-free threshold.[67]

A tax ‘resident’ of Australia is defined by reference

to four tests:

- the

resident according to ordinary concepts test

- the

domicile and permanent abode test

- the

183-day test – unless the Commissioner is satisfied that the person’s usual

place of abode is outside Australia and that the person does not intend to take

up residence in Australia and

- the

Commonwealth superannuation fund test.[68]

A person only needs to satisfy one of the above tests in

order to be taxed as an Australian resident. Generally foreign residents on

short-term work visa are not considered tax residents and are subject to the

non-resident tax rates. For the 2022–23 and 2023–24 income years, a tax rate of

32.5% applies from the first dollar of income earned up to $120,000.[69]

From the 2024–25 income year onwards, a tax rate of 30% applies from the first

dollar of income earned up to $200,000.[70]

Table 5(a):

Non-resident tax rates for 2021-22 and 2022-23

Taxable

Income

|

Tax on

this income

|

| 0 – $120,000 |

32.5 cents for each $1 |

| $120,001 – $180,000 |

$39,000 plus 37 cents for each $1 over $120,000 |

| $180,001 and over |

$61,200 plus 45 cents for each $1 over $180,000 |

Source: Tax

rates – foreign resident, Australian Taxation Office website (updated on

1/07/2022).

Table 5(b):

Resident tax rates for 2021-22 and 2022-23

Taxable

Income

|

Tax on

this income

|

| 0 – $18,200 |

Nil |

| $18,201 – $45,000 |

19 cents for each $1 over $18,200 |

| $45,001 – $120,000 |

$5,092 plus 32.5 cents for each $1 over $45,000 |

| $120,001 – $180,000 |

$29,467 plus 37 cents for each $1 over $120,000 |

| $180,001 and over |

$51,667 plus 45 cents for each $1 over $180,000 |

The above rates do not include the Medicare

levy of 2%.

Source: Tax

rates – resident, Australian Taxation Office website (updated on

1/07/2022).

Current

taxation arrangements for workers on temporary migration visas

Different taxation arrangements currently apply to

visa-holders in the SWP, the PLS and the PALM scheme.

For workers in the SWP, a tax rate of 15% applies,[71]

and is substantially lower than the starting marginal tax rate of 32.5% that

applies to other non-resident workers but:

- higher

than the 0% tax rate which applies to the first $18,200 earned by tax residents

– the $18,200 is known as the tax-free threshold amount which is not available

for non-residents such as SWP workers[72]

and

- lower

than the 19% for each dollar over $18,200 and 32.5% for each dollar over

$45,000 up to $120,000, earned by tax residents.

Foreign workers in the PLS are taxed at resident rates, as

PLS workers are considered to be residents for tax purposes (because they can

work in Australia between a minimum of one year and up to three years or longer).[73]

This means they benefit from the tax-free threshold discussed above and can

claim deductions.

Example 2 –

Australian resident in the PLS

Joe comes to Australia for 4 years on

a 403 visa issued prior to 4 April 2022 under the PLS to pick fruit

and nuts in rural and regional locations. Joe is an Australian resident for tax

purposes in Australia.

Joe works at a cherry farm in Wangaratta,

Victoria. He is paid $21 per hour and guaranteed 10 hours for 6 days

each week. As Joe is an Australian resident, his employer will withhold tax

from his salary and wages based on the resident tax rates. Joe’s weekly salary

is calculated as:

$21 per hour × 10 hours × 6

days = $1,260 per week

His employer withholds tax and an amount

for the Medicare levy = $251 per week

Joe’s take home pay each week is $1,009

Joe is required to

lodge a tax return at the end of the tax year.

Source: Australian Taxation Office, Seasonal

Worker Programme and Pacific Labour Scheme

However, foreign workers in the PALM visa scheme are

currently generally taxed as non-residents, at a tax rate of 32.5% for the

first $120,000 earned, 37% for income earned between $120,001 and $180,000, 45%

for income earned over $180,000.[74]

What are the

problems that the Bills seek to address?

As noted above, the PALM visa scheme consolidated,

reformed and replaced the SWP and PLS visa schemes. This means the PALM scheme

will seek to attract similar Pacific and Timor-Leste workers to those under the

previous SWP and PLS visa streams to work in all sectors of Australia’s

economy.[75]

However, these groups of foreign workers, who perform similar work (with some

differences across the three programs), are taxed differently, depending on the

type of visa they hold.

The Government argues that the higher tax rates currently

applied to visa holders under the PALM scheme will discourage workers’

participation in the program and therefore mean the program would defeat its

dual purposes of addressing Australia’s workforce shortages and maintaining

good relations with participating nations by helping the Pacific and

Timor-Leste workers to send homes savings and remittance.[76]

In addition, the current legislation does not have the

flexibility to allow the Australian Government to, by regulations, provide

concessional taxation rates to future visa programs for foreign workers.

Instead, the Government needs to amend the legislation to apply concessional

tax rates each time a new visa program is introduced.

Who will

the Bills effect?

As at 31 July 2022, there are 26,500 workers in the PALM

visa scheme.[77]

The Government has stated that ‘there are currently more Pacific and

Timor-Leste PALM scheme workers in Australia than there have ever been before’.[78]

There are also 40,108 pre-screened workers awaiting job

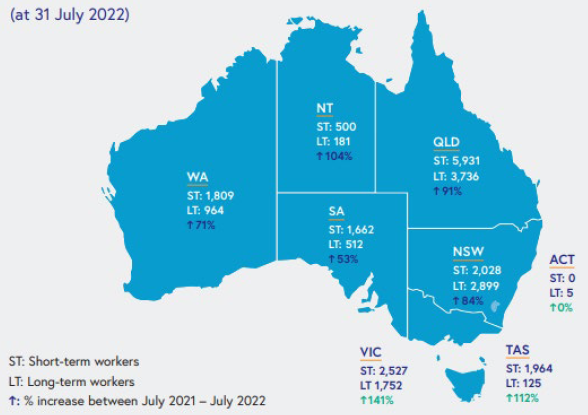

offers from approved PALM scheme employers as at 31 July 2022 (see Figure 1

below).[79]

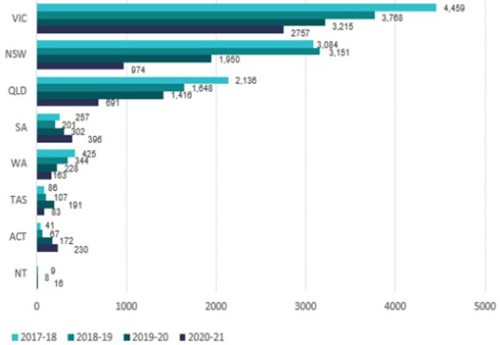

Figure

1: Distribution of workers

Source: PALM, Expanding, 2.

As at 31 July 2022, there are 387 PALM approved employers.[80]

Employers will also be impacted by the measures proposed in the Bills as they

are required to withhold the correct tax rate using the PAYG withholding system

and claim the correct deduction amounts for salaries, et cetera.

Key

provisions

Schedule 4 to the Main Bill and Schedule 1 to

the Supporting Bill will rename the current ‘Seasonal Labour Mobility Program

withholding tax’ regime as the ‘labour mobility program withholding tax’

regime.[81]

Further, the Main Bill defines a labour mobility program as

including:

The effect of the other amendments in Schedule 4 to

the Main Bill and Schedule 1 to the Supporting Bill is that foreign

workers

- participating

in a labour mobility program

- will

pay an income tax rate of 15% on the salary, wages, commission, bonuses or allowances

received as an employee of an Approved Employer when they held a relevant

temporary work visa and was a foreign resident.[83]

This would mean that from 1 July 2022 foreign workers

under the new PALM scheme visa will receive similar taxation treatments as

those under the SWP visa scheme.

Ability to apply concessional tax rates to future new

labour mobility programs

The Main Bill also ensures that any future Government can

expand the concessional tax treatment by applying it to new types of visas via

regulations, rather than being required to amend the Income Tax Assessment

Act 1997.[84]

The Explanatory Memorandum argues:

This will increase flexibility to update the tax law in

response to future changes, such as changes to program names or the creation of

new programs for foreign residents for which this tax treatment is appropriate.

It will also allow flexibility to update the tax law in response to changes to

visa names by regulations.

This will provide the Government with the necessary

flexibility to make timely changes to tax arrangements to support the success

of Australia’s existing and future labour mobility programs. The regulations

would be subject to disallowance and therefore will be subject to appropriate

parliamentary scrutiny.[85]

These amendments were not included in the lapsed Treasury

Laws Amendment (Enhancing Tax Integrity and Supporting Business Investment)

Bill 2022 introduced by the previous Morrison Government.

Commencement

of changes to taxation of relevant visa holders

The Supporting Bill commences on 1 July 2022 and the

amendments in Schedule 4 to the Main Bill will either commence at the same

time, or do not commence at all, if the Supporting Bill does not commence.[86]

The amendments apply retrospectively in relation to salary,

wages, commission, bonuses and allowances paid on or after 1 July 2022. The Explanatory

Memorandum notes that the retrospective amendments are ‘wholly beneficial to or

do not disadvantage anyone affected by the amendments’ due to a lower income

tax rate applicable to the foreign worker employees and a lower withholding tax

rate applicable to the employers.[87]

Key issue 1: Horizontal equity

One of the criteria of good tax design is ‘horizontal

equity’. The notion of horizontal equity requires taxpayers in the same

position be taxed the same.[88]

In that regard, the Bill raises two horizontal equity

issues.

The first – which the Bill seeks to address – is ensuring

that workers in the PALM visa stream, the Seasonal Labour Mobility Program (or

SWP) and other future similar programs, pay the same rate of tax (15%). If

there are no changes to the current tax arrangements, workers in the PALM

scheme will pay more than twice the amount of the income tax (32.5% as a

starting rate) than workers in the SWP (15%), and such a difference in tax

treatment under the two visa schemes may appear to be unfair.

The second – which the Bill does not address – is that the

measures in the Bill, if passed, would result in non-resident workers without a

labour mobility program or Working Holiday Maker (WHM) visa being

taxed at a higher rate than non-resident workers that do hold those visas, even

if they are performing the same work for the same employer.

Whilst not explored in detail in this Digest, prior to the

introduction of the ‘backpacker tax’ for WHM visa holders, taxation-related

proposals reflected a view that it was appropriate to tax foreign workers on

short-term visas on the same basis, regardless of the sector they worked in or

the type of visa that they held.[89]

As such, a key issue raised by the Bill is whether it is appropriate

to tax foreign workers on short‑term visas working from specific

countries:

- in

the same manner as other non-residents foreign workers or

- on

a more concessional basis compared to other non-residents workers.

Readers are referred to the Bills

Digest that was written for two lapsed Bills for further details on this

issue.[90]

Key issue 2: Australia’s strategic objective with the

Pacific and Timor-Leste nations

The Australian Government has indicated its intention to

run the PALM scheme with the aim of producing a ‘win-win’ outcome for both

Australia and the partnering nations.

If the seasonal workers in the PALM scheme are taxed at a

higher starting rate of 32.5% as a foreign resident, there is a danger that the

PALM scheme would fail its dual purposes of

- addressing Australia’s workforce shortages,[91]

and

- maintaining good relationships with the Pacific and Timor-Leste nations.[92]

Committee consideration of the

related key issue

Joint Standing Committee on

Foreign Affairs, Defence and Trade

In its March 2022 report, the Joint Standing Committee on

Foreign Affairs, Defence and Trade recognised the growing importance of labour

mobility schemes in the enduring Australia-Pacific relationships. The Committee

recommends that such schemes be built on to support career development, build

relationships, and provide pathways to permanent residence. [93]

Recommendation 2 of the report states the

following.

The Committee notes the growing importance of the Pacific

Australia Labour Mobility scheme for skills transfer and training and as a

source of remittance income, and the support for such programs amongst the

Pacific. The Committee recommends the Australian Government:

• pursue steps to scale-up the

program, better support career development, and provide pathways for permanent

residency, akin to those being developed for the Agriculture Visa Scheme; and

• explicitly recognise the relationship building and

cultural exchange elements of the Pacific Australia Labour Mobility Scheme in

its design and promotion.[94

Policy

position of non-government parties, independents and major interest groups

The PALM scheme and its expansion have attracted some media

attention. For example, ABC News recently reported that farmers have

traditionally relied on backpacker labour for planting and harvest work but,

since the pandemic, working holiday-makers are yet to return in the same

numbers.[95]

Bree Grima, the chief executive of Bundaberg Fruit and

Vegetable Growers, said that made it even more critical the Pacific workers are

supported:

If it wasn't for [the Pacific workers], we simply would not

have been harvesting our crops or planting our crops either… We've had some

brilliant numbers come into Queensland and into regional areas, a lot more than

we've had before. So we need to make sure that the workers that are here, that

are keen to stay here, that they've got the support mechanisms to ensure that

they've got that work available for them.

There's a lot of work and time and effort that goes into

becoming an approved employer, and there should be... It is a difficult

process to go through but I do support that it does do a lot of background

checks and ticks a lot of boxes. These workers, they are highly skilled, they're

putting a lot into the community, and we need to make sure that we're looking

after them in every aspect.[96]

ABC News also reported that the unions and employers in

the aged care sector considered the extension of the PALM scheme to include

aged care as a positive move but warned that there would be minimal impact:

- CapeCare

chief executive Joanne Penman was reported to have said that the full-time

[Fijian] workers had made a huge difference, working with the non-for-profit

aged care provider for four months.

- Australian

Nursing and Midwifery Federation (ANMF) federal secretary Annie Butler was

reported to have said overseas-trained workers had long formed a significant

part of Australia's care and nursing workforce and the expansion of the scheme

could have a positive, yet limited impact.

- Aged

and Community Care Providers Association interim chief executive Paul Sadler was

reported to have said Pacific Island workers would fill a limited portion of the

empty roles.

- South

Sea Islander worker welfare advocate Geoffrey Smith was reported to have said a

lot more work to address Australia’s history of mistreatment of people from

South Pacific Islands was needed before expanding the program.[97]

The concerns reflected in the last point above are

consistent with the historical prevalence of underpayment or non-payment of

wages and other unlawful employment arrangements in the agricultural sector and

are examined in detail in the Bills

Digest to the lapsed Income

Tax Amendment (Labour Mobility Program) Bill 2022 and the Income

Tax Amendment (Labour Mobility Program) Bill 2022.[98]

Financial

implications

Schedule 4 (Main Bill) and Schedule 1 (Supporting

Bill) partially implements the Pacific Labour Mobility – reforms measure

from the previous Government’s 2021–22 Mid-Year Economic and Fiscal Outlook.[99]

The Government estimates that the measure will increase

receipts by $165.0 million over the then forward estimates period.[100]

All figures in this table represent amounts in $ million.

| 2021-22 |

2022-23 |

2023-24 |

2024-25 |

| 40.0 |

45.0 |

40.0 |

40.0 |

Source: Explanatory Memorandum, 4.

These estimates reflects the tax that was expected to be

paid at the proposed rates by workers participating in the new Pacific

Australia Labour Mobility scheme and the expansion of the Pacific Labour

Scheme. This estimate includes an increase in goods and services tax receipts of

$50.0 million over the then forward estimates period that will subsequently be

paid to the states and territories.

Compliance

cost impact

The Government has stated that this measure ‘is expected

to result in a negligible impact on compliance costs, as the proposed taxation

arrangements are consistent with existing taxation arrangements for other

labour mobility programs’.[101]

Schedule 5 (Main Bill):

Faith-based products

The Bill proposes amendments to the Superannuation

Industry (Supervision) Act 1993 (SIS Act) to establish a supplementary

performance test for faith-based superannuation products.

Performance test for MySuper

products

MySuper products were introduced in 2013. They were designed

to be a simplified superannuation accumulation product, into which

contributions are paid if the employee either nominates the product or does not

express a choice about which fund their superannuation contributions are paid

into.[102]

That is, they are intended to be simple, cost-effective and balanced investment

options eligible to receive default contributions.[103]

In 2018, the Productivity Commission conducted a review of

Australia’s superannuation system (the PC Review) which made a number of

findings relevant to the introduction of the performance test:

- many

Australians have low financial literacy and are disengaged from their

superannuation[104]

- holding

superannuation in one of the worst performing funds could mean a person retired

with a significantly lower superannuation balance

- high

fees also eroded final superannuation balances.[105]

The Treasury Laws

Amendment (Your Future, Your Super) Act 2021 introduced a performance

test for MySuper products to hold superannuation funds to account for

underperformance through greater transparency and increased consequences. The

Australian Prudential Regulation Authority (APRA) conducts the test each year.

There are two components to calculating the performance

measure:

- the

net investment return of a product over the past 8 years (actual return) is

compared to a benchmark return and

- the

product’s representative administration fees and expenses (actual RAFE)

for the most recent financial year is compared to the median RAFE (benchmark

RAFE).[106]

The benchmark return is a passive investment portfolio

of indices tailored to the product’s reported strategic asset allocation.

As noted in the PC Review, using a benchmark portfolio to assess investment

performance aims to account for the many influences on investment markets which

are beyond funds’ control, while providing insights into the value added by

funds.[107]

The issue of selecting an appropriate portfolio of indices is examined below in

the ‘key provisions and issues section’.

Recent test results

The performance text was applied to MySuper products from

1 July 2021, with 13 products failing the performance test in 2021.[108]

Of those, 2 belonged to funds with clear religious affiliations (Australian

Catholic Superannuation and Retirement Fund and Christian Super).[109]

The performance test looks at results over 8 years meaning some newer funds

committed to investing along ‘ethical’ or ‘socially responsible’ principles

were not tested. A values-based investment fund, Australian Ethical’s MySuper

passed the performance test by 132 basis points.[110]

The 2 Christian funds which offered products which did not

pass the performance test in 2021 have since merged with other funds.[111]

There have also been further mergers of other Christian funds.[112]

According to the Financial Standard, this only leaves 2 religious funds

– Anglican Super (managed by Mercer) and Crescent Wealth.[113]

Key issues and provisions

The ALP made an election promise to ‘allow APRA to take

into account the religious affiliation of a super fund when applying the

recently-introduced performance benchmark.’[114]

Schedule 5 of the Bill implements this commitment.

What is a faith-based product?

Proposed section 60K defines a faith-based

product as one specified in the determination made by APRA. In turn, proposed

section 60L prescribes the information an entity would need to provide to

APRA in order for its product to be classified as a faith-based product. As

part of this process the trustees of the entity must apply to APRA to make a

determination that a product is a faith-based product. In making such an

application, the trustees of the entity must:

- declare

that the investment strategy for the product accords with faith-based principles

- declare

that they have:

- disclosed

the investment strategy to beneficiaries of the product and

- disclosed

(and in the future disclose) the investment strategy in marketing materials and

- provide

to APRA one or more indices which APRA could use to assess the product’s

performance

- provide

any additional information as specified in the regulations.

The Explanatory Memorandum notes that regulations may

provide that an application must contain:

- the

trustee’s investment strategy, which includes the product’s faith-based

principles

- the

product’s Product Disclosure Statement

- a

copy of any advertising materials disclosing the product’s faith-based

investment strategy and

- the

time at which the product adopted its faith-based investment strategy.[115]

Treasury has released an Exposure

Draft of the Regulations which set out the information that will be

required to be disclosed.

As part of a consultation process undertaken by Treasury

on the Exposure

Draft of the Bill,[116]

some stakeholders expressed concerns about the proposed definition of a

faith-based product, based on the definition being ‘circular’, lacking detail

and not being clear.[117]

In relation to how the proposed definition of a

faith-based product could be improved, some stakeholders suggested:

- applying

‘quantifiable criteria’ such as considering on a look-through basis whether the

products invest in companies that earn above a certain percentage of their

revenue from activities not inconsistent with their faith-based filters[118]

- that

the Bill or regulations give ‘explicit guidance on expectations of a

faith-based product. Where this is limited to religious principles… this should

be made explicit’[119]

and

- drawing

on legal definitions of ‘religion’ and/or the Australian Bureau of Statistics’

Australian Standard Classification of Religious Groups.[120]

Key issue: creating a

supplementary performance test

Under the existing Part 6A SIS Act framework, if a MySuper

product fails the performance test, a number of consequences will apply:

- APRA

must publish the fail result on a website maintained by APRA (see subsection

60C(5) of the SIS Act)

- trustees

must notify beneficiaries of the fail result using a notification letter

prescribed by regulations (see section 60E of the SIS Act) and

- for

two consecutive fail results, trustees are prohibited from accepting new

beneficiaries into the relevant product (see section 60F of the SIS Act).

Schedule 5 of the Bill amends the SIS Act to

provide for a supplementary annual performance test for faith-based products.

If a faith-based product fails the original performance test, none of the above

consequences will apply.[121]

Instead, APRA must assess the product against the supplementary performance

test. The trustee of the faith-based product only experiences the consequences

of a failed performance test if it fails the supplementary performance test.[122]

For the current performance test, APRA is required to

calculate a benchmark return for a product using assumed indices set out at

regulation 9AB.17 of the Superannuation

Industry (Supervision) Regulations 1994. The appropriateness (or

inappropriateness) of those indices is examined below.

However, for the supplementary test, APRA may use

alternative indices for faith-based products.[123]

Proposed subsection 60P(5) provides that regulations may specify

requirements relating to the supplementary performance test. In turn, proposed

subsection 60Q(4) provides that such regulations may include requirements

relating to APRA determining appropriate indices for a faith-based product.

The Explanatory Memorandum notes that in deciding on

alternative index or indices, APRA will consider whether an alternative index

or indices reflects the faith-based investment strategy, and it is anticipated

that APRA will consider the indices included in the application for faith-based

status.[124]

Exposure

Draft Regulations relating to the supplementary performance test for faith-based

products were released on 12 September 2022. In summary, the Exposure Draft

regulations would:

- allow

APRA to make a determination specifying alternative assumed indices

for the covered asset classes in the table in regulation 9AB.17 of the existing

regulations

- requires

APRA to consider the suitability of any of the indices provided in the

application for faith-based status when determining alternative assumed indices

for the product. In deciding on an alternative index or indices, APRA will

consider whether the provided alternative index or indices reflects the

product’s faith-based investment strategy.[125]

However, the draft explanatory statement notes ‘it is not

expected that APRA will investigate all available indices or propose

alternative indices in making a determination.’[126]

In addition, as currently drafted, the proposed regulations do not appear to

enable APRA to create customised indices by removing any investments that were

excluded from a faith-based product from otherwise appropriate indices.

As such, it does not appear that the proposed

supplementary performance test addresses the issue of the lack of appropriate

indices used as the basis for both the current performance test and the

proposed supplementary test, as discussed below.

Key issue: lack of appropriate

indices

Stakeholders raised a number of concerns about the

existing operation of the current law with regards to appropriate indices by

which to measure MySuper product performance, as well as in relation to the

proposed indices for faith-based products.

Current use of indices in the

performance test

As noted above, each MySuper fund is required to benchmark

each product it offers to a portfolio of listed market indexes that reflects

the asset allocation of the product.[127]

Whilst not explored in detail in this Digest, APRA

provides information and guidance on how it selects appropriate indices by which to

measure the performance of MySuper funds.[128]

For example, where a MySuper product invests in:

- Australian

equities, the S&P/ASX 300 is used as the index

- Australian

Listed Property, the S&P/ASX 300 A-REIT Index is used as the index and

- International

Fixed Interest, the Bloomberg Barclays Global Aggregate Index (hedged to AUD).[129]

In turn, where a MyProduct invests in more than one

category, relevant indices are combined with appropriate weighting to provide

an overall appropriate index.[130]

Several stakeholders have previously expressed concerns

about not only the indices used to measure MySuper product performance, but how

they are selected and how many are used, including:

- ‘Given

the seriousness of the consequences of the ‘underperformance’ test, the

proposed test will drive trustees to make investment decisions effectively to

‘hug the index’. This is in conflict with the objective of delivering good

member outcomes over the medium to long term’[131]

- ‘the

performance benchmark test will cost consumers because it will constrain super

funds from constructing portfolios which are in the members’ best interests’[132]

- ‘The

question has been raised as to whether the benchmarking approach potentially is

in conflict with members’ best interests and member outcomes, as it measures

the returns of assets in a particular class against the index for that class, a

measure of investment efficiency, but does not take into consideration the

strategic asset allocation or risk of the investment portfolio underlying the

product.’[133]

- ‘An

increased number of indices will better capture the intended implementation of

the trustees and therefore the fund’s ability to deliver against relevant

benchmarks. Fewer indices will result in an assessment that captures more than

a fund’s ability to deliver on their planned implementation. Such an outcome

could result in some good performing funds failing the test whereas some poorly

performing funds could pass the test.’[134]

Further, some stakeholders have previously expressed

support for a second test be developed for funds or products which fail the

initial performance test.[135]

These concerns are relevant to the measure proposed by the

Bill as a key area of concern for stakeholders is the use of indexes, how they

are selected and the non-availability of alternative mechanisms to measure

performance not only of faith-based MySuper products, but others as well.

Concerns about appropriate

indices for faith-based products

The Jefferson and Shea Group (JSG) noted that

superannuation funds and products which offer investment strategies reflecting

the religious faith and values of their member base have a distinct nature and

different principles from other products.

JSG noted such funds and products ‘have a clear mandate

from members to express these values in the way the fund invests’ and this

usually results in ‘specifically customised’ funds and products that generally

follow one or more of the following investment forms:

- portfolio

construction – diverging from a market-cap benchmark weighting of portfolio

assets to favour (upweight) assets neutral or more aligned with faith

principles and exclude (‘screen out’) or down-weight other assets less aligned

with faith principles

- active

ownership – holding assets in order to exercise voting rights and seek to

engage with a company to improve performance on issues relevant to faith values

and

- impact

investing – investing (sometimes in partnership) in organisations which have

specific social benefit or otherwise non-financial goals, along with financial

goals. Financial goals in this context may be given a longer timeframe to be

achieved and/or be held to a lower priority. Considerable due diligence is

performed by funds in order to support specific impact investment initiatives.[136]

JSG provided examples of how the above can influence the

performance of faith-based MySuper products:

• a large cap US equity portfolio applying a Catholic Values

screen had materially different weightings to the top 3 sectors relative to the

S&P 500 Index – Information Technology (44 bps overweight), Health Care (92

bps underweight) and Financials (62 bps overweight)

• a large cap Europe, Australasia and Far East (EAFE) equity

portfolio applying a Catholic Values screen had materially different weightings

to the top 3 sectors relative to the MSCI EAFE Index – Financials (51 bps

overweight), Industrials (65 bps underweight) and Health Care (190 bps

underweight)

• the MSCI World ESG Leaders Index had several materially

different sector weights to the MSCI World Index, including a 113 bps

overweight to Communications Services and a 130 bps underweight to Utilities.

Collectively, these intentional faith- and values-driven

portfolio biases create annual return differences to their respective agnostic

benchmarks of 84-104 bps over the short term and 11-45 bps over longer term

horizons, in one asset class alone.[137]

As a result, JSG and other stakeholders indicated that it

may be difficult or almost impossible to find suitable indices to benchmark

funds against, or that the current system used to compare the performance

faith-based products that apply faith-based screening to investment decisions

to other superannuation products that don’t isn’t ‘comparing apples with

apples’.[138]

For example, in their submission Haven Wealth described

systemic problems with the evaluation of values-based investments:

One of Haven Wealth Partners’ biggest frustrations is that

our high conviction ethical approach is classified ‘responsible’ just the same

as the investment product built on the bare minimum screening to achieve the

same ‘responsible’ classification. To date, ratings and certifications in this

area tend to be binary rather than depict the level of commitment toward

screening. That said, we are aware of developments in this space.[139]

As noted above, the Exposure Draft of the Superannuation Performance

Test Treatment of Faith‑based Products – Regulations 2022 does seem

to address this problem by giving APRA the power to determine an alternative

index for comparison (proposed regulation 9AB.18A(2)(d)).

However, whilst this would allow APRA to develop

alternative indexes, the draft regulations to not appear to able to address the

excluding of certain industries entirely from indices used in the performance

test, to better reflect faith-based investment decisions. Some stakeholder

argued that this would an objective performance comparison to be made, whilst

better reflecting the faith-based investment strategy of the relevant product.[140]

For example, RIAA argued:

for asset class where the product’s investment strategy

varies significantly because a faith-based approach excludes a number of

investments, ‘ex-screening’ indices could be determined. For example, for

Australian equities this could be the S&P/ASX 300 reweighted to remove any

investments that were excluded for that product.[141]

Financial implications

The Explanatory Memorandum to the Bill states that there

are no financial implications arising from the provisions in Schedule 5

of the Main Bill.[142]

However, if people retire with lower superannuation

balances, it can reasonably be expected that they will rely more heavily on the

Age Pension. The PC Review suggested that the difference between a low performing

fund and a high performing fund could be as much as $502,000 over a lifetime.[143]

This is equivalent to at least 8–10 years’ income in retirement.[144]

Position

of major interest groups

There were 15 submissions to Treasury’s Exposure Draft of

the Bill. Stakeholders uniformly supported choice in superannuation products,

however, none of the submissions supported the proposed changes unreservedly,

with some arguing strongly against the creation of a ‘two-tier’ system.

Stakeholders that would be directly impacted by the

reforms (that is, entities involved in faith‑based investment services)

appear to favour reforms to the existing performance test or changes to the

proposed supplementary performance test that would allow industries excluded

from faith-based or values-based products to be removed from indices used in

either test, to better reflect faith-based or value-based investment decisions.

Most stakeholders appear to favour including the proposed

changes in the wider Review

of Your Future, Your Super Measures, particularly as similar changes are

likely to be extended to other funds with a values-based investment philosophy

and with submissions from bodies supportive of proposed changes indicating that

further changes may be necessary.[145]

Separately, Margaret Cole of APRA said that the annual

performance test was ‘driving change and improvements for members.’ She also

stated that while APRA was supportive of review, it was for others to decide if

further parameters should be added to the performance test.[146]

‘Equity’ of the current

performance test and proposed supplementary test

Stakeholders raised different views about the equity of

introducing a supplementary performance test for a single category of MySuper

products (faith-based products).

The Industry Superannuation Australia submission argues:

The Government’s proposal to provide differential treatment

to faith-based products – by giving these products two attempts to pass the

performance test – potentially undermines the intention of the test. In

particular, it creates an uneven playing field between faith-based products

and other superannuation products, including products that are also

applying values-based investment principles (such as those that are marketed as

being ethical or socially responsible) … To the extent unintended and perverse

outcomes arise as a result of applying the current performance test benchmarks

to faith-based products, the same issue is likely to exist for other products,

including those that apply values-based investment principles.

Accordingly, ISA recommends that the treatment of faith-based

products be considered as part of the Government’s broader review of the Your

Future, Your Super reforms later this year. Committing to specific changes for

faith-based products ahead of that review is premature and appears to add an

additional layer of complexity to the review that could otherwise be avoided.[147]

[emphasis added]

In contrast, the Association of Superannuation Funds of

Australia argues:

If a product has made a ‘values-based’ or

‘principles-based’ decision not to invest in one or more assets then it is not

appropriate to assess that product against a benchmark that includes the performance

of those assets. Instead, the benchmark should be adjusted by removing

those assets and the product assessed against the adjusted benchmark… By way of

example, if a product has decided not to invest in tobacco products, or

armaments, or gambling, because of the deleterious effect on public and

individual health, the relevant benchmark(s) should be adjusted by removing the

performance of those products from that benchmark.

Further, establishing a paradigm in which a product ‘fails’

the original, unadjusted, performance test, and is then assessed against a

‘supplementary’, adjusted, performance test, creates the impression that the

product has ‘failed’ but has been granted special treatment, in the form of a

concession, to be assessed against another test. We submit that this should not

be the case – instead a product should be assessed against a single,

appropriate, benchmark in the first place to determine whether it has succeeded

in delivering appropriate outcomes to members.

Accordingly, we suggest that, in lieu of a ‘supplementary’

performance test, ‘values-based’ or ‘principles based’ products should be

assessed against a performance test that has been adjusted to take into account

the filters/screens that the trustee has put in place and whether that

product has passed or failed in delivering appropriate outcomes to its members

is determined on the basis of that assessment.[148]

[emphasis added].

JSG argued that ‘there is no compelling policy reason for

penalising a faith-based investment strategy for underperforming an agnostic

performance benchmark’.[149]

Haven Wealth Partners noted that the proposed reforms are in

part aimed at making sure faith-based investment products receive a ‘fair and

reasonable’ performance assessment given the additional complexity of their

product design and the customers which they serve.[150]

Likewise, in their submission Crescent Wealth said:

Whilst the proposed changes to the Act are welcome; we urge

and recommend that given the nature, processes and extra costs of faith based

funds, that further and expanded amendments to the Act be considered … We

believe such further changes … will assist in creating a more level playing

field for faith based funds.[151]

Other issues raised by

stakeholders

As noted above, other issues raised by stakeholders

included:

- whether

these changes should be considered as part of the wider Review of Your Super,

Your Future Measures currently being undertaken by Treasury

- that

similar conditions would be extended to other values-based products and

- the

effect that a separate test would have on the amount of superannuation people

retired with.

Table 6 below summarises stakeholder responses

around those issues.

Table 6: Summary of

stakeholder responses against three of the major themes

| Organisation name |

Should be part of the wider review |

Extension to other values-based funds |

Financial impact |

| Actuaries Institute |

Y |

Y |

|

| Association of Superannuation Funds of Australia |

Y |

|

|

| Australian Institute of Superannuation Trustees (AIST) |

Y |

|

Y |

| Chartered Accountants ANZ and CPA Australia |

Y |

Y |

|

| Council on the Ageing (COTA) |

|

Y |

Y |

| Crescent Wealth |

|

|

|

| Financial Services Council |

Y |

Y |

|

| Haven Wealth Partners |

|

Y |

|

| Industry Super Australia |

Y |

Y |

Y |

| Jefferson and Shea Group |

|

Y |

|

| Mercer |

Y |

Y |

|

| National Renewable Energy Network |

|

Y |

|

| Responsible Investment Association Australia |

|

Y |

|

| Super Consumers Australia |

Y |

|

Y |

Source: Treasury, Superannuation

Performance Test Treatment of Faith-based Products, Submissions.

Appendix A: Relevant statistical data for Schedule 1 (Main Bill) Foreign

acquisitions and takeovers penalties[152]

The Foreign Investment

Review Board (FIRB)has

been publishing annual reports on insights into foreign purchases and sales

of residential real estate since 2017–18 when the Register

of foreign ownership of residential land (the Register) was introduced.

FIRB also publishes data on the number of approvals and applications processes

each financial year in their annual reports.

The most recent version of the Register covers transactions

by financial year from 2017-18 to 2020-21. These figures only cover residential

property transactions over each period, there is no data on foreign

ownership levels in this report. It should also be noted that foreign

persons in this report do not include permanent residents, who do not require

FIRB approvals for residential property purchases. Figures for purchases and

sales are provided down to the state level.

Figure 2:

Four-year comparison of purchase transactions by state or territory

Source: FIRB, Register

of foreign ownership of residential land: Insights into foreign purchases and

sales of residential real estate 2020–21, 7.

Over the 4-year period covered by the Register, Victoria

has reported largest number of foreign purchases of residential property,

followed by NSW. The number of purchases has fallen steeply over the COVID-19

period, with all the states/territories except for the ACT, NT and SA showing

an overall reduction in purchase counts in 2020-21 when compared to 2019-20.

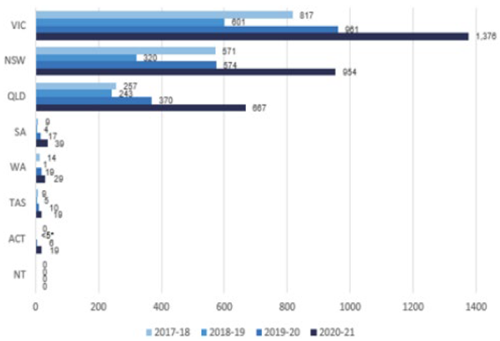

Figure 3:

Four-year comparison of sale transactions

There was an increase in

sales counts when compared to 2019-20 in all states and the ACT.

Source: FIRB, Register

of foreign ownership of residential land: Insights into foreign purchases and

sales of residential real estate 2020–21, 9.

For sales, there have been much smaller numbers of

transactions prior to 2020–21. In contrast to purchases, COVID-19 led to a