Chapter 2

Strategic Review of the NBN

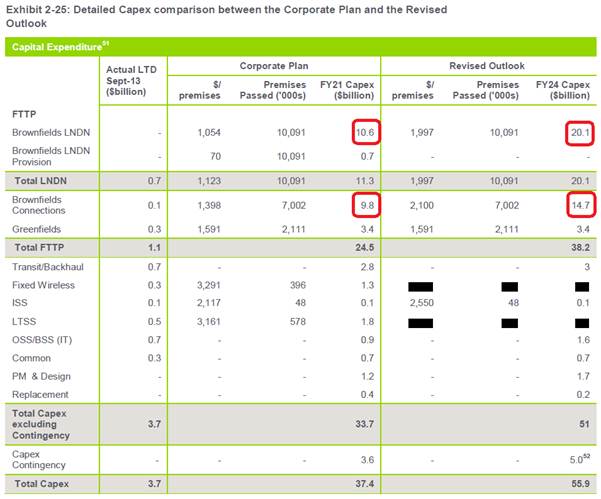

Background

Purpose of the Strategic Review

2.1

While in opposition, Mr Turnbull made frequent claims that the Coalition

broadband policy could be implemented for a third to a quarter the cost of the

NBN. For example:

FTTN in Europe and North America has been described to me by

those actually building new generation networks as costing between one third

and one quarter of FTTP. Given our relatively high labour costs and the fact

that FTTN’s main virtue is that it reduces the civil works which is mostly

labour, the difference in Australia is likely to be even higher.[1]

2.2

And:

Why can we do it cheaper? Fibre to the node, around the

world, costs between 1/4 and 1/3 of fibre to the premises. That is the

experience in North America and Europe. And in Australia with very high labour

costs the differential would likely be even more.[2]

2.3

Minister Turnbull also repeatedly asserted that the “real” cost of the

NBN would be different to the figures in NBN Co’s Corporate Plan. For example,

he told Tony Jones on Lateline in February 2013:[3]

We're going to do a couple of things. We will do a rigorous

cost/benefit and have a rigorous cost/benefit analysis done, but very quickly

we will ensure that we get a fully transparent and accurate assessment of what

it is really going to cost both in terms of dollars and time to complete the

project on the basis of the Government's strategy and then what it will cost in

terms of dollars and time to complete it on a variation along the lines we've

been proposing and we'll get that up very quickly.

2.4

Launching the Coalition policy on 9 April 2013, Mr Turnbull quantified

the expected saving, saying:[4]

We wouldn’t have gone about this this way and there will be

billions of dollars that Labor has wasted that we cannot recover but we will

save many billions of dollars, at least $60 billion, by taking the approach we

have described in this policy.

2.5

The Coalition’s Broadband Policy included a table labelled “The Choice

at a Glance”:[5]

2.6

The table asserted the likely required funding for the existing NBN was

$94 billion, while estimating required funding for the Coalition plan as $29.5

billion. This inflated estimate for the NBN was achieved by making four

assumptions: that real Average Revenue Per User (ARPU) would not grow as

forecast; that the number of “mobile only” households would be higher than

forecast; that costs would be higher than forecast; and that construction would

take longer than forecast.[6]

2.7

At a hearing of the Joint Committee on the National Broadband Network on

19 April 2013, executives from NBN Co demonstrated that the assumptions

underpinning the Coalition’s $94 billion claim were false.[7]

In particular, they demonstrated that actual costs for the fibre build were

falling and that all other costs were within budget. They also demonstrated

that the calculation of ARPU increase used by the Coalition was wrong. Finally

they noted that the effect of a delay in the rollout would result in a decrease

in peak funding, not an increase.

2.8

However, notwithstanding the falsehoods in the Coalition policy, the

Committee notes that the peak funding amount of the proposed Coalition

plan—$29.5 billion—is approximately “a third” of the inflated $94 billion cost

of the NBN, in accordance with previous statements made by Minister Turnbull.

This would not have been the case, of course, had the proposed Coalition peak

funding amount of $29.5 billion been compared to the $44 billion peak funding

figure in NBN Co’s 2012-15 Corporate Plan, which—as outlined below—was signed

off by the NBN Co Board and independently reviewed by KPMG.

2.9

As mentioned in Chapter 1, the Strategic Review was one of the

commitments made in the Coalition’s Broadband Policy taken to the 2013

election. In announcing the terms of reference of the review the Minister said:

Labor's made shocking mistakes. There are billions of dollars

that Labor has wasted that we will never be able to recover. This has been a

shockingly misconceived exercise...wasteful exercise in public policy. We are

endeavouring to recover value for it and get the job completed as quickly and

cost-effectively as we can. So we need to know, what is the state of the

project right now, accurately...[8]

2.10

A draft of the Strategic Review was provided to Government on 2 December

2013.[9]

Following board approval, a final report was provided to the Minister for

Communications and the Minister for Finance on 12 December 2013. This final

report was released in a heavily redacted form when it was tabled by the

Minister for Communications on the same day.[10]

2.11

Prior to its publication, two comments about the potential conclusions

of the Strategic Review were made publicly: the first by former NBN Co board

member Brad Orgill, and the second by former NBN Co CEO and Executive Director

Mike Quigley.

2.12

In a column in the Australian Financial Review on 4 October 2013, Mr

Orgill said:

Selective data, conservative assumptions and extrapolations

out to 2021 could be formulated to argue why the NBN might have comprehensively

blown out its costs and not achieved its objective. It would be a continuation

of the Coalition's attacks from opposition on NBN management and the board

including threatening a Royal Commission of Inquiry.

2.13

On 2 December 2013, in an address to TelSoc, Mr. Quigley said:

Rates to build the fibre network based on the existing design

and architecture were rising. But those rate increases would not have produced

a cost increase because we had identified and validated, network and design

changes that would have offset those increases. Which is why I find it

incomprehensible to hear the suggestion that the increases in LN/DN rates

should be built into the forward projections and cost reductions that have

already been identified, should not be. Unless, of course, your objective is to

try to confirm a pre-conceived position.

Key findings of the Strategic

Review – Revised Outlook

2.14

The Strategic Review provided a detailed review of the costs and

deployment timing of the existing deployment model for the NBN (called the

Revised Outlook). The Revised Outlook asserted that:

-

The fibre rollout project will take three years longer to

complete than indicated in the Corporate Plan, with a revised end date of June

2024;

-

The Revised Outlook for brownfields Premises Passed at June 2014

is 357,000 compared to 1,129,000 in the Corporate Plan;

-

Delays in deployment and take-up, lower ARPU and higher levels of

non-subscription result in ~$13-14 billion less Revenue to FY21;

-

The Capital Expenditure required will increase from $37.4 billion

to $55.9 billion;

-

The peak funding requirement will be $72.6 billion peaking in

FY24 which is $28.5 billion higher than the Corporate Plan ($44.1 billion); and

-

The Independent Assessment concluded that it is highly unlikely,

in the absence of a government guarantee, that debt funding will be available

from a third party financier in the near to mid-term.

2.15

As will be demonstrated below, these assertions were arrived at by the

use of variants of the same assumptions used by the Coalition in its April 2013

$94 billion claim: higher unit costs, rollout delays, lower growth in ARPU and

fewer premises connected.

2.16

The Strategic Review makes five key findings in relation to the

performance to date of NBN Co. These are:[11]

-

From a forensic perspective, the Independent Assessment found

that no material issues exist within the accounts of NBN Co;

-

The Independent Assessment concluded that, although the Corporate

Plan is based on detailed and quantitative analysis, it is “extremely

optimistic” and very unlikely to be achieved;

-

At 30 September 2013, the rollout of the brownfields FTTP network

was 48 percent behind the planned Premises Passed in the Corporate Plan, with

only 227,483 Premises Passed at that date. Of these premises only 153,977 are

serviceable by NBN Co. The greenfields and Fixed Wireless rollouts are also

behind Corporate Plan;

-

Total Expenditure to 30 June 2013 was 26 percent under the

Corporate Plan at that date. Whilst this is an under-spend relative to the

Corporate Plan, it is significantly ahead of the expenditure which would have

been required in the Corporate Plan to reach the levels of actual rollout

achieved; and

-

The Independent Assessment found that NBN Co has attracted a

committed, motivated, and generally capable group of people who want to do

important, meaningful work. It concluded that the culture and leadership of the

organisation are widely seen to be a major problem, and that the organisation

is currently carrying a level of overhead and headcount predicated on the

achievement of the Corporate Plan, which is in excess of current requirements.

2.17

As noted above, the Strategic Review found the Corporate Plan 2012-15

was based on detailed and quantitative analysis. At the hearing of 17 December,

Mr Korda provided an explanation for the difference between the Corporate Plan

2012-15 and the Revised Outlook:[12]

CHAIR: Can I confirm that the independent assessment

found that the revised outlook analysis is based on a revised and more

realistic review. Could you explain to me what that means.

Mr Korda: What we found in the corporate plan—I will

tie this together—was that, as BCG said, the revenue forecasts were optimistic.

I think deployment was optimistic. I think the level of overheads was

optimistic. The capex was optimistic. So what you get—I think we said—is a very

extremely optimistic corporate plan. We have reviewed each of those line items

based on the facts and have taken a realistic and more prudent view of where we

are at.

2.18

The Strategic Review also considered five alternative scenarios. These

are:

-

Scenario 2 – Radically Redesigned FTTP

-

Scenario 3 – FTTN short loop, FTTB large MDUs

-

Scenario 4 – HFC in HFC footprint

-

Scenario 5 – FTTN & HFC

-

Scenario 6 – Optimised Multi-Technology Mix

2.19

The Section 2.3 assesses the recommended option, the “Optimised Multi

Technology Mix.” However, as will be detailed below, scenarios utilising FTTN

and HFC depend on assumptions about possible outcomes of negotiations for

access to infrastructure and the state of that infrastructure. The assumptions

underpinning these scenarios are not as robust as the data available for the

all-FTTP scenarios (Scenarios 1 and 2).

Conduct and methodology

2.20

The terms of reference of the Strategic Review required NBN Co to report

on:

-

The progress and cost of the rollout and NBN Co’s financial and

operational status;

-

The estimated time and cost to complete the NBN under a

fibre-to-the-premises (FTTP) model (i.e. Government policy prior to 7 September

2013);

-

The estimated cost and time to complete the NBN if variations

were made to the current plan such as increased use of fibre-to-the-node (FTTN)

in established (brownfield) areas;

-

The economic viability of NBN Co under alternative strategies;

-

The implications of capital costs and principles of cost recovery

on wholesale and consumer prices under existing and alternative strategies;

-

Recommendations for organisation restructuring, any amendments to

the construction model and a revised NBN Co strategy to achieve Government

policy objectives; and

-

Any other matters the Chair deems relevant to the strategic

consideration of NBN Co’s present situation and future prospects.[13]

2.21

NBN Co tendered for advisory firms to contribute to the Strategic

Review. Three firms were appointed on 25 October: Deloitte, KordaMentha and the

Boston Consulting Group (BCG). Each performed a different function as part of

the review process.[14]

KordaMentha contributed to the analysis of the NBN operational and financial

performance; BCG reviewed the timing, financials and product offers under

alternative models; and Deloitte provided governance and program management

office services to ensure the Strategic Review met the parameters and deadline

for submission set by the Government.

2.22

At the committee's public hearing in Sydney on 17 December 2013, it was

revealed that the total cost of preparing the strategic review was in the order

of $8 million. This included the cost of the consultancies and NBN Co's

internal resources.[15]

It was also explained that BCG rather than KordaMentha was used for the revenue

estimates “given their international experience.” NBN Co could not provide any

specific expertise BCG had in relation to Australian revenue modelling.

2.23

The strategic review process was led by NBN Co's Head of Strategy and

Transformation, Mr JB Rousselot, and a 'cross-divisional team of internal

employees' working closely with the external consultants on the review.[16]

NBN Co executives told the committee that approximately 25 people were involved

in the review on a dedicated basis, led by Mr Tim Ebbeck, chief commercial

officer at NBN Co. During the course of the review, 280 workshops were held

involving different groups from within NBN Co.[17]

2.24

During the Supplementary Estimates hearing in November 2013, Dr

Switkowski summarised the approach to be used by the strategic review:

The way this review is structured is that there are two substantial

parts, one headed by KordaMentha, which is a forensic analysis of the costs of

NBN Co. to date and expectations of a business-as-usual scenario and associated

costs; then there is another analysis, which will be informed by BCG, as to the

costs and execution issues of an alternative technology path. BCG is

commissioned to do a complete analysis of the technical challenges of rollouts

around Australia, identifying options that extend from fibre to the premises,

fibre to the node, fixed wireless satellite, HFC and 4G wireless. That will all

come together and be integrated by the third of the advisory firms, Deloitte,

and will then constitute the report that the board will present to the

minister.[18]

2.25

For the Revised Outlook, KordaMentha undertook the review of costs and

rollout timeframes, while BCG undertook the review of revenue. At the Committee

hearing on 17 December, NBN Co explained that this decision was made because

the revenue assumptions would be common across all scenarios:

CHAIR: For the independent assessment, why was

KordaMentha used for the costs, but BCG for the revenue? There seems to be a

split in the way it was designed and I am interested in the thinking behind it.

Mr Rousselot: The revenue forecast we had to do was

going to be applied to all scenarios going forward—so, not only the revised

forecasts but also all the other scenarios we are going to have. That is why we

had to have one of the two companies produce the revenue forecast. We selected

BCG to do so, given their international experience. The costs of the revised

outlook were only relevant to the revised outlook, and that is why those were

done by KordaMentha.[19]

2.26

At a doorstop on the day the Strategic Review was announced, the

Minister made it very clear the review was to be “owned” by the board and

management:[20]

That is the most urgent priority, and the reason that we've

asked the board to do it, or the company to do it, and of course it will be

substantially a new board, and there will be a lot of new management there as

well no doubt, is that we want the company to own it. You see, in the past,

this project has been riddled with politics, and the company has been under

pressure to deliver numbers and answers and documents that met the political

priority of the previous government.

What I have said to the company is I just want the plain

unvarnished facts. We do not want spin. We do not want the company to tell us

what they think we might want to hear. We want to know what the real facts are.

And then armed with those facts, then we can make decisions about the future of

the project and Australians will see the actual factual context in which we're

making them. That is terrifically important.

And the reason the company should undertake this is because

we want them to own it. See, you can - there's any number of consulting firms

you can hire, and the NBN Co's hired most of them over the last four years, but

you can hire a consulting firm, they'll come in and write a report. But the

directors, the executives may have no sense of ownership of it. They may - it's

just something that descended from outside.

It's really important that the directors and the management

own this.

Committee analysis – Revised Outlook and Radical Redesign

Preliminary Observations

2.27

The committee notes the heavily redacted nature of the public version of

the Strategic Review. In-depth scrutiny of the Strategic Review's findings with

regards to delays in FTTP deployment (including construction delays), Fixed

Wireless deployment, and financial performance (particularly Direct Operating

Expenditure) is compromised by these redactions.[21]

Of particular concern to the committee is the redacted information on cost per

premises. Cost per premises is used in the Strategic Review as the key

benchmark for the comparative analysis of alternative scenarios.

2.28

The Minister for Communications has refused to release to the committee

(in camera) an unredacted copy of the Strategic Review, on the grounds

of public interest immunity. This was set out in a letter of 17 December 2013.[22]

However, the committee considers that the Strategic Review underpins a

potential Commonwealth investment of more than $40 billion—not including

flagged technology upgrades—and should be made available to the Parliament, in

accordance with the Minister’s many undertakings on transparency and

accountability. This will be discussed further in Chapter 4.

2.29

The Committee notes that the Strategic Review states in its Legal

Notice:

Given the required time frame for the Report’s completion,

NBN Co has relied on the Experts for the matters within their scope of work and

has not independently verified or audited the information presented in the

Report through the work of the Experts.

2.30

The committee asked NBN Co whether the Strategic Review had been subject

to the same independent scrutiny that had been applied to NBN Co’s Corporate

Plans:

CHAIR: Thanks for that, but what I was asking you was

to confirm what was in the legal notice stated in the strategic review—that it

has not been independently verified or audited. I am just asking you to confirm

that is what the strategic review says.

Dr Switkowski: You are asking about our review?

CHAIR: Yes, the legal notice.

Dr Switkowski: It has not had any further

verification.[23]

2.31

At the public hearing on 17 December 2013, the committee put to Dr

Switkowski that without the unredacted information, the committee and the

public will have to take NBN Co's word that the cost assumptions in the

Strategic Review are correct:

Senator LUDLAM: Apart from that, I have never seen so

many blacked-out rectangles on an NBN committee. It is almost as though the

whole operational security mantra has been imported into telecommunications

policy. I know I am being a bit tongue in cheek here, but it is a linchpin of

your entire project, those numbers: the remediation costs and any operational

expenses for keeping it maintained while it falls apart around you.

Dr Switkowski: I agree that those numbers matter. I

can only give you an assurance that they have been determined to the best of

our ability with considerable debate as to what the range of numbers should be

to characterise those costs. They have been incorporated in our models.

Senator LUDLAM: So you cannot tell us what they are,

but can you tell us how you arrived at them? We can ask this of Telstra in 20

minutes and they will tell us that those numbers are commercially sensitive as

well, but you must have landed on a particular number or a range of numbers.

How have you done that? Have you concluded negotiations with the companies

concerned?

Dr Switkowski: Clearly we have not. We have barely

started discussions.[24]

2.32

Despite the difficulties presented by the redactions, the committee

notes that a number of assumptions in the Strategic Review are transparent, or

can be derived from a close reading of the report. The committee has also

collected substantial evidence from committee hearings and relevant secondary

sources.

2.33

Section 2.2 reviews the Revised Outlook (“Scenario 1”) and the Radical

Redesign (“Scenario 2”). This is because these two scenarios are both based on

an FTTP rollout to the full fixed line footprint. It is also because cost

savings identified in Version 13 of the Corporate Plan 2013-16 were included in

the Radical Redesign scenario, and had that plan been used as the base case for

the Revised Outlook a different conclusion would have been reached. This will

be demonstrated below.

Base case used for the Strategic

Review

2.34

The Strategic Review notes that:[25]

For purposes of performance comparison, the Independent

Assessment used the August 2012 NBN Co Corporate Plan (referred to as the

Corporate Plan), which is the most recent Shareholder approved plan.

2.35

NBN Co released its Corporate Plan 2012-15 on 8 August 2012. This plan

noted:

-

Wholesale broadband prices are projected to fall over time in

both real and nominal terms;

-

The Internal Rate of Return (IRR) remains above 7% per annum;

-

Total forecast Capital Expenditure to end of the Fibre

Construction period increased by 3.9%;

-

Construction Commenced or Completed for approximately 758,000

Fibre premises by December 2012; and

-

Fibre Construction period extended by 6 months despite 9 month

delay in Commencement Date.

2.36

The 2012-15 Corporate Plan also noted that there had been changes to the

scope of work since the first Corporate Plan. This included changes to the

design reflecting the Telstra definitive agreements and the Optus HFC

Agreement, and decreases in construction and equipment costs referred to as

“Type 2 Architecture”. These efficiencies are the principal reason capital

expenditure only changed by 3.9 per cent between the 2012-15 Corporate Plan and

NBN Co’s 2011-13 Corporate Plan released in December 2010.

2.37

This issue was discussed during the 11 December hearing:

CHAIR: In developing the 2012-15 corporate plan, NBN

Co. moved to type 2 architecture. Would you explain the changes from type 1

architecture. I suspect Mr McLaren is the lucky respondent.

Mr McLaren: Yes, absolutely. The type 1 architecture

was an initial architecture for the fibre network—this is the passive network,

which we commonly also call the local and distribution network. It was an

architecture we developed for our initial trials that NBN ran in five cities

and commenced in 2011. It used an architecture that essentially relied on what

we call stranded fibre—strands of individual fibres that are deployed and

individually spliced, so quite a lot of fibre splicing has to go on. It is

essentially what the Australian market had been deploying for many years and

was an evolution through that. It also used quite a lot of the technology in some

of our initial learnings that we had seen overseas. So it was very much an

initial deployment, particularly informed by what Verizon were doing in the

United States, which was very much an aerial build. We took a lot of the

learnings from that company and applied it for those trials.

During that period, we had been looking at other options. We

were particularly concerned by the amount of fibre splicing that would be

involved with that architecture. As I said, each individual fibre had to be

sliced, which was not only time consuming; it was very much a cost and resource

issue in terms of getting the number of splices to be able to do it. So we were

looking for ways to reduce that burden in the build. The main change with the

type 2 architecture was to bring in what we call ribbon fibre. That is where we

have 12 fibres in a ribbon and they are all spliced, basically simultaneously,

with some new fibre-splicing machines.

CHAIR: There was a significant cost saving for you in

that process. You said one of the reasons you looked at this was cost savings.

Mr McLaren: Yes cost savings, as I just mentioned,

with the actual splicing itself. We have also been going—

CHAIR: Have you found a way to reduce the cost of the

build?

Mr McLaren: Obviously, we were looking at all options

to reduce the cost of the build through this time. The cost also came down to

how we went through our procurement process at the time. Type 1 was initial

work with our suppliers. We went through a more extensive procurement process

for type 2 and worked with the whole market, and were able to use the savings

that came to that procurement process as well.

2.38

NBN Co submitted its 2013-16 Corporate Plan to shareholder Ministers on

3 July 2013. This plan, known as “version 12,” confirmed the headline figures

for the NBN as set out below, compared to the previous Corporate Plan.[26]

Version 12 of the 2013-16 Corporate Plan was subsequently leaked to the

Australian Financial Review and is available on its website.[27]

Major Operational & Financial Metrics

2.39

Prior to its submission to the previous government, the Corporate Plan

2012-15 was independently reviewed by KPMG. The 2013-16 Corporate Plan was also

independently reviewed by KPMG. This was confirmed during a November hearing of

the Senate Environment and Communications estimates committee. The Secretary of

the Department of Communications, Mr Clarke, noted that:

The department as a matter of course commissioned analysis on

corporate plans on an annual basis.[28]

2.40

Mr Robinson, Deputy Secretary for the Department of Communications,

added that:

I think it is a matter of record that, at least for the last

couple of years, we commissioned KPMG to provide advice.[29]

2.41

The NBN Co board also commissioned Ernst & Young to review the

2013-16 Corporate Plan. This was confirmed during the same estimates hearing:[30]

Senator LUNDY: Did you engage any advisers for the

2012 to 2016 plan?

Mr Payne: For the June draft of the 2013 to 2016

corporate plan the board engaged Ernst & Young to review some of the key

assumptions...

Senator LUNDY: Did that review provide any advice that

the data did not appear to be aligned with the corporate plan assumptions?

Mr Payne: I think, overall, it said that the

experience to date supported the broad assumptions made in the corporate plan.

Senator LUNDY: So the Ernst & Young adviser

reviewing the corporate plan for the 2013 to 2016 plan found that all the

assumptions were correct.

Mr Payne: That was so for the key assumptions that

they looked at. They did not look at everything.

Senator LUNDY: What did they look at? Did they look at

the capital expenditure parameters?

Mr Payne: I do not have the report with me. They

certainly looked at some of the key capital expenditure areas, some of the

revenue assumptions and so on.

Senator LUNDY: Did that review provide any advice that

the actual data did not appear to tally with the corporate plan assumptions on

revenue or capital?

Mr Payne: No. As I said, overall it supported the

assumptions. There were a couple of areas that the report called out that it

was very early days and hard to draw too many conclusions from the data to

date, but overall—

Senator LUNDY: You had an external adviser—and

independent adviser—advise that the 2013 to 2016 corporate plan was consistent

with the performance of the company.

Mr Payne: Certainly on the assumptions, yes.

Senator LUNDY: That was before the report was

submitted to the government.

Mr Payne: Correct.

2.42

Version 12 of the 2013-16 Corporate Plan was received by Government

while Telstra remediation was suspended due to asbestos concerns. Subsequently,

NBN Co sent shareholder Ministers a letter noting that the duration of the

stoppage in remediation work was more prolonged than expected and had put at

risk the deployment targets in the 2013-16 Corporate Plan. Shareholder Ministers

asked NBN Co to resubmit the plan to take these developments into account. NBN

Co prepared a revised Corporate Plan—called ‘version 13’—which was submitted to

the NBN Co Board in September 2013, after Telstra pit work had recommenced in

mid-August 2013. As Mr Payne noted during the 19 November estimates hearing:

I think the board approved [version 12] for lodgement in

June, so it would have gone in at the end of June to the shareholder ministers.

At around that time, you may recall, there were some issues particularly around

remediation ceasing, and so, I think, the company wrote to the shareholder

ministers to say that the short-term targets may need to be revised because

there was expected to be a prolonged cessation in remediation. So the shareholder

ministers asked us to resubmit the plan with that taken into account; hence the

second version in September.[31]

2.43

The “second version” referred to by Mr. Payne—known as ‘Version 13’—is

the most recent version of the NBN Co Corporate Plan, incorporating the effects

of the Telstra stop-work on remediation. NBN Co was asked about this Corporate

Plan at the 11 December 2013 hearing:

CHAIR: Mr Brown, Mr McLaren, Mr Cooney or even Mr

Adcock, was a draft version 13 of NBN Co.'s 2013-16 corporate plan provided to

the board for its meeting on 19 and/or 20 September?

Mr Brown: Each year, as required under the GBE

guidelines, we submit a corporate plan.

CHAIR: Thanks. Now could you answer the question I

asked? Was a draft version 13—1 and 3, comes after 12 and before 14—of NBN

Co.'s 2013-16 corporate plan provided to the board for its meeting on 19 and/or

20 September 2013? Yes or no?

Mr Brown: Yes, there was a copy submitted.

CHAIR: Version 13?

Mr Brown: Can I take that on notice? I am not aware of

exactly what version it was.

2.44

To date, NBN Co has not answered this question on notice. However, the

committee notes that a Corporate Plan was scheduled for board consideration on

19 or 20 September 2013.

2.45

NBN Co and the Departments of Communications and Finance were asked

whether a copy of this plan was submitted to shareholder departments. NBN Co

gave the following evidence:[32]

CHAIR: What is the normal practice for NBN Co.

communications to shareholder departments when it comes to documents that must

be considered by the government?

Mr Brown: The normal practice is NBN would put

together whatever that document is. I assume in this case we are talking about

the corporate plan....normally it would go to the board and, with their

agreement, it would be submitted as a draft to our shareholder ministers,

consistent with the GBE guidelines.

CHAIR: Can you confirm that version 13 of the corporate

plan was submitted to the shareholder departments via the portal prior to the

considerations. That would tend to suggest that perhaps it was not, but if you

could take on notice whether or not version 13 was supplied to the departments

before that board meeting. Was this version of the corporate plan approved by

the board on 19 or 20 September?

Mr Brown: I would need to take that on notice to

review the minutes of that board meeting.

2.46

The committee has not received an answer to this question on notice.

2.47

The Department of Communications gave the following evidence:[33]

CHAIR: What is the normal practice for NBN Co.

communications to shareholder departments? You may have heard that we had a

discussion earlier today about this. When it comes to documents that have to be

considered by government, do these documents appear on a portal?

Mr Clarke: Yes. There is a secure portal arrangement

to facilitate the transfer of confidential documents.

CHAIR: Is it the case that drafts of these documents

are often provided to shareholder departments prior to board consideration to

enable shareholder departments to prepare timely advice for government?

Mr Clarke: I can—

CHAIR: We both know the answer, but you need to say it

on the record.

Mr Clarke: For board documents it is less common, but

for documents that are conveyed between the parties, yes, that is a common

practice.

CHAIR: So was the draft of version 13 of NBN Co.'s

2013-16 corporate plan submitted to shareholder departments via the portal

prior to its consideration by the NBN Co. board on 19 September? It is a

simple, factual question. You know it has already been asked. It should be very

easy to ascertain.

Mr Clarke: I am not going to answer it.... I am choosing

to uphold the principle that the communications that are intended between the

agency through the department to the government—the nature of them; what was on

the table when, which is implicit in your questioning—are a confidential

matter.

2.48

The committee notes that NBN Co has yet to answer questions on notice

about the status of version 13 of the Corporate Plan, and the Department of

Communications has flatly refused to answer questions on whether a copy was

provided to Government. The committee further notes that the Minister made

reference to the content of version 13 of the Corporate Plan during the NBN

Rebooted conference in November 2013:[34]

Shortly before the election, the NBN Co revised its June 30

2014 premises passed target down to 600,000 brownfield premises.

2.49

In his speech to TelSoc on 2 December 2013, Mr Quigley also made some

observations about the content of Version 13 of the Corporate Plan:[35]

We did have to advise the Government in September that, the

issues with the LN/DN construction combined with the remediation stoppage moved

the construction end date from June 2021 to December 2021. The effect on the

financials of that six month shift in the construction end date was that

revenue returned to $23Bn since there was 6 months more revenue, but Opex

increased by about half a billion dollars due to the extra six months of

operating costs. The Capex spend is spread across a 6 month greater period

which leaves the total funding and the IRR unchanged. The contingency was also

unchanged.

Just to re-emphasise a previous point – our December of 2010

Corporate Plan contained a capex contingency of 10% or about $3.6Bn, the last

plan which was submitted in September retained the same level of contingency.

If the Management team had any doubt about offsetting the increased LN/DN rates

by the cost reductions we had planned, we would have made use of some of that

contingency. We had no such doubts.

What is remarkable is how little the financials changed over

the 3 years.

2.50

The most recent version of the NBN Co Corporate Plan—the most accurate

“base case”—was the 2013-16 Corporate Plan (Version 13) referred to by Mr Payne

in his testimony, prepared by NBN Co management and submitted to the board on

20 September 2013. Dr Switkowski was asked why version 13 was not used as the

base case during the 17 December 2013 hearing:

CHAIR: He [Mr Robin Payne] said in evidence at

estimates that the government asked that the company further review the June

draft to incorporate the consequences of the delay due to remediation. Given

that version 13 of the corporate plan 2013-16 was the NBN Co.'s response, why

wasn't that used as the baseline?

Dr Switkowski: We certainly are of the view that the

baseline that had to be referred to was the one that was formally in the system

and approved, and that any update of the performance of NBN Co. was within the

mandate of the current review, and that is what we presented in the [Strategic

Review] last week.[36]

2.51

Subsequent to this exchange, Mr Rousselot confirmed for the committee

that Versions 12 and 13 of the Corporate Plan 2013-16, as well as other documents,

were made available to the Strategic Review team.[37]

Summary of findings—Base Case used

for the Strategic Review

-

In July 2013, the NBN Co board submitted to shareholder

Ministers the NBN Co Corporate Plan 2013-16 (“version 12”). Former shareholder

Ministers requested that “Version 12” be amended to incorporate the effects of

Telstra’s stop work on remediation. NBN Co prepared a revised Corporate

Plan—called ‘version 13’—which was submitted to the NBN Co Board on 19 or 20

September 2013.

-

It is normal practice for NBN Co to provide shareholder

departments with the Corporate Plan prior to Board consideration so that timely

advice for government may be prepared.

-

“Version 13” of NBN Co’s Corporate Plan 2013-16 represents the

most recent and accurate “base case” for the NBN. Despite this, the Strategic

Review used the fifteen-month old NBN Co Corporate Plan 2012-15 as the “base

case.” The reason for this will be examined in the following section.

Treatment of architecture changes

2.52

In his speech to TelSoc on 2 December 2013, Mr Quigley said:

With our LN/DN rate increases, we had exactly the same

situation. Increases in the LN/DN rates would be offset by other cost

reductions. And I am not talking about speculative cost reductions, where you

say to yourself: “oh, we need to find $2Bn in savings, somehow”. I am talking

about things that had already been identified, like smaller diameter cables

that had already been designed by cable companies, reduced and more efficient

testing, smaller footprint multi-ports that had already been designed,

reductions in fibre counts and corrections in planning tools that allowed

smaller mandrels and greater fill ratios for ducts. We called these changes our

2.x architecture. At the end of September, NBN Co was on track to implement

these cost reductions, as any sensible company would.

So, let me be clear. Rates to build the fibre network based

on the existing design and architecture were rising. But those rate increases

would not have produced a cost increase because we had identified and

validated, network and design changes that would have offset those increases.

Which is why I find it incomprehensible to hear the suggestion that the

increases in LN/DN rates should be built into the forward projections and cost

reductions that have already been identified, should not be.

Unless, of course, your objective is to try to confirm a

pre-conceived position.

2.53

On 11 December 2013, an article in the Australian Financial Review

by Philip Coorey & James Hutchison cited an NBN Co Board paper dated 20

September 2013.[38]

The NBN Co Board paper states:

The COO and CTO teams have undertaken a review of the current

network architecture for the access fibre network with the aim of identifying

and implementing a set of cost saving design and construction initiatives. Cost

savings from these initiatives, together with other productivity initiatives

underpin the assumed reduction in the CPP to FY18. This review incorporates a

number of in-flight Project Fox initiatives and pragmatic cost saving solutions

into a combined revised architecture which will be incorporated into future

FSAM designs. The planned changes are as follows:

-

Reduced fibre allocation per premise

-

Mandrel sizing and FOND cable diameter correction

-

Introduction of small diameter fibre cables

-

Removal of PON protection in certain circumstances

-

Fibre testing optimisation

-

Introduction of the small footprint multiport for underground

build.

2.54

Further:

The proposed architecture savings and cost reduction

initiatives represent a combined value of greater than $4.5 billion, which

support the assumptions in the Corporate Plan of a reduction in CPP to

construct the access fibre network from $1500 in FY14 to $1054 by FY18. The

initiatives will continue to be progressed through the COO and CTO teams with a

target to finalise an implementation plan for both new and current in-flight

designs by the end of September.

2.55

The cost savings identified in Mr Quigley’s speech and the 20 September

NBN Co board paper—“smaller diameter cables that had already been designed by

cable companies, reduced and more efficient testing, smaller footprint

multi-ports that had already been designed, reductions in fibre counts and

corrections in planning tools that allowed smaller mandrels and greater fill

ratios for ducts”—were discussed at length during the 11 December public

hearing.[39]

2.56

In relation to the smaller diameter cables:

CHAIR: Has the NBN Co. looked at introducing smaller

diameter fibre cables?

Mr McLaren: Yes. We are working with our vendors in

the fibre supply to obviously look to see improvements with smaller fibre

cables.

2.57

In relation to reduced and more efficient testing:

CHAIR: Has NBN Co. ever looked at optimising its fibre

testing?

Mr McLaren: Yes. As with many of these items, we are

always looking to optimise our testing for anything that has a cost in the

build.

2.58

In relation to smaller footprint multiports, Mr McLaren noted:

We have been working with our suppliers to introduce a

smaller form. It is not so much that it is smaller, but it is more flexible and

able to fit into Telstra's pits more easily. It will allow the work to proceed

quickly and there will be not be so much work in remediating those pits. We

have introduced that and it is already rolling out, as I understand it, in our

fieldwork now, a smaller footprint multiport.

2.59

In relation to corrections in planning tools that allowed smaller

mandrels and greater fill ratios for ducts:

CHAIR: Has a mandrel size change been implemented?

Mr McLaren: Yes.

2.60

In relation to the reduced fibre counts in the second leg:

CHAIR: Has NBN Co. ever looked at reducing the fibre

counts in distribution cable from 576 fibres to 433 fibres?

Mr McLaren: Yes, we have been investigating that

opportunity. Again, it is an opportunity to have smaller diameter cables, as we

talked about.

2.61

In relation to removing the second leg of a distribution loop:

CHAIR: Has NBN Co. ever looked at removing the second

leg of a distribution loop in certain FSAMs where the effect can be managed

within the terms of the WBA?

Mr McLaren: Yes. In some instances in the current

build of our network where that second leg is very difficult and costly, we

have made the decision not to build it.

2.62

In relation to the implementation of “Architecture 2.X” more generally,

Mr McLaren observed:

Mr McLaren: 2.x is not a big bundle of change. There

are incremental changes in many different parts of the network. We mentioned

the small footprint multiport. We mentioned techniques, and I think you

mentioned the now more efficient [mandrel]. There is testing which we use in

our rodding and roping, giving us a more accurate gauge on the available duct

space, and we have introduced those changes. So a number of changes are

incrementally being introduced into the design process over time.

2.63

The committee notes that by end September 2013, NBN Co was in the

process of implementing, or had already implemented, network changes to reflect

the move to Architecture 2.x. This is confirmed by Mr McLaren’s testimony, the

20 September Board paper and Mr Quigley’s speech. These architecture changes

resulted in greater than $4.5 billion in capital expenditure savings.

2.64

However, the Strategic Review only identifies $1 billion in cost

savings, and reduces these savings by a further 50 per cent:[40]

The Independent Assessment notes that there are opportunities

for cost reductions in the future. Some potential savings have been identified

in network design and architecture, primarily in reduced equipment costs,

however a business case needs to be prepared. Business cases for ~$1 billion of

potential savings have been completed and implementation of some of these

improvements is underway. These could be achieved over time, but allowing for

the time to introduce these concepts and other risks, it is prudent to adjust

the amount by 50 percent.

2.65

This issue was raised in the 17 December 2013 public hearing:

CHAIR: So to reiterate again, the strategic review

ignored over $4 billion worth of savings because there was no business case

presented notwithstanding the board previously had actually had a submission

put up by the company to them and an assumption has been made—which you are not

able to assist us with other than saying, 'I agree with it,'—that $500 million

of the savings should be dumped—just dumped—because it is prudent.

Mr Rousselot: As I said, the analysis that we did of

the potential savings was one that looked at it, and talked with people within

the company, either in operations or in design, to understand the status of the

savings that had been identified.

CHAIR: But as for the billion dollars, business cases

had been provided for the billion dollars.

Mr Rousselot: I do acknowledge that that is the case,

yes.

CHAIR: And you just halved it?

Mr Rousselot: We took a consideration of risk that was

still attached to implementing those savings.

CHAIR: Mr Quigley, in his speech, seemed to predict

this would happen. He said he found it incomprehensible to hear the suggestion

that the increases in LNDN rates should be built into the forward projections and

that cost reductions that have been already identified should not be 'unless,

of course, your objective is to try and confirm a preconceived position'. It is

getting pretty hard to disagree with Mr Quigley, Mr Rousselot, if you are

ignoring savings deliberately and you are not applying any productivity

learnings and savings across the entire project except for two years in four

years time. It is getting pretty hard to disagree with Mr Quigley.

Mr Rousselot: The level of prudence that we have

applied to this particular scenario we have applied to the other scenarios.

2.66

A number of the cost savings identified above appear in the Strategic

Review in Scenario 2 (‘Radically Redesigned FTTP’). For example, the Strategic

Review provides that scenario 2 includes:[41]

Cost-efficient architecture and materials (a saving of

[redacted] per premises passed) including reducing from 3 to 1.2 fibres per

premises, increased use of aerial deployment, removal of PON protection, using

smaller diameter fibre cables, use of gel-free cables and eliminating the

battery back-up for the NTD.

2.67

The committee has put several questions in writing to NBN Co requesting

information about why these $4.5 billion in cost savings were excluded from the

Revised Outlook, and instead included in the ‘Radical Redesign’. In response to

a question in writing asking about the $4.5 billion in cost savings identified

in the 20 September NBN Co board paper, NBN Co replied:

As stated at the Senate Committee hearing on 17 December

2013, many working documents including these Board papers were made available

to the expert advisers. The advisers have formed the view that some elements of

the savings proposed may be realised in a scenario where current FTTP practices

are reviewed and optimised significantly – e.g. a “radically redesigned FTTP

rollout”.[42]

2.68

Similarly, the Strategic Review characterises the “radically redesigned”

scenario as follows:[43]

Based on overseas experience, it is possible to radically

redesign the NBN Co FTTP deployment to reduce the Cost Per Premises. The

changes to deployment include changes in the delivery model, which in turn

result in labour productivity improvements, different and more cost-efficient

architecture and materials, and cost-efficient construction techniques. This

radically redesigned FTTP deployment is estimated to cost [redacted] build

Capital Expenditure per brownfield premises passed, representing savings of

[redacted] per premises passed versus the Revised Outlook.

2.69

In an answer to another question on notice, NBN Co stated that:[44]

The Revised Outlook considered the operational and financial

position of the company based on the continuation of current rollout plans. As

highlighted in paragraph 3.2.8, these potential efficiencies may be realisable

through a step-change and transformation of the organisation.

2.70

And:

Scenario 2, Radically Redesigned FTTP contemplates NBN Co

making significant changes to its FTTP deployment approach to improve NBN Co’s

productivity and construction techniques. Within this scenario, it is expected

that these “radical” changes will increase rollout speed and decrease costs.[45]

2.71

The committee notes that the architecture changes (2.X) resulting in

these cost savings were characterised by NBN Co’s Chief Technology Officer, Mr

McLaren, as ‘incremental’ improvements that did not represent ‘a big bundle of

change.’ Mr Quigley similarly characterised these improvements as business as

usual: “at the end of September, NBN Co was on track to implement these cost

reductions, as any sensible company would.”

2.72

However, when asked about why these savings were not incorporated into

the Revised Outlook, NBN Co characterises them as ‘radical’ and ‘significant’

and requiring a ‘step-change and transformation of the organisation.’

2.73

The Committee considers that the Revised Outlook and the Radical

Redesign scenarios make different assumptions about the future trends for cost

per premise passed for FTTP. In fact, the so-called “radically redesigned” FTTP

scenario represents a better estimate of the costs that would be incurred by an

active and interested management than the Revised Outlook. This is supported by

the fact that many of the savings based on Architecture 2.x had already been

incorporated by previous NBN Co management into the September 2013 Corporate

Plan (Version 13).

2.74

The committee considers that the implementation of these architecture

changes was business as usual for NBN Co, and the exclusion of the associated

savings from capital expenditure assumptions distorts the outcome of the

Revised Outlook. The committee also notes that had the Strategic Review used

Version 13 of the NBN Co Corporate Plan as the ‘base case’ for the Revised

Outlook, the Revised Outlook would have arrived at a different outcome.

Summary—Treatment of architecture

changes

-

By end-September 2013, NBN Co had implemented, or was in the

process of implementing, a number of incremental changes to the fibre rollout

known as Architecture 2.x. Combined, these changes represented $4.5 billion in

capital expenditure savings.

-

Version 13 of NBN Co’s Corporate Plan 2013-16, prepared for

Board consideration on 20 September 2013, incorporated these architecture

changes and the associated savings to capital expenditure. It also incorporated

changes to the deployment schedule from Telstra’s stop-work on remediation.

Version 13 is the most recent and accurate NBN Co Corporate Plan.

-

Despite this, the Strategic Review used NBN Co’s fifteen-month

old 2012-15 Corporate Plan as the ‘base case’ for the Strategic Review. Only

$500 million of the architecture savings were included in the Revised

Outlook—the bulk of these savings were incorporated into Scenario 2 rather than

the Revised Outlook. This was justified by characterising the changes as

‘radical’ rather than incremental.

-

The committee considers that the implementation of these

architecture changes was business as usual for NBN Co, and the exclusion of the

associated savings from capital expenditure assumptions distorts the outcome of

the Revised Outlook by bolstering costs.

Assumption of brownfield delays

2.75

The Revised Outlook has factored in a delayed roll out schedule compared

to the 2012-15 Corporate Plan. This is set out in Exhibits 2-10 and 2-11:

Deployment Schedule—Corporate Plan

Deployment Schedule—Revised Outlook

2.76

Some general observations justifying this assumption are set out in the

Strategic Review, although many of these are redacted.[46]

These include: “[redacted]; the complexity of the interfaces between NBN Co and

the Delivery Partners, the uniqueness of an infrastructure build of this scale

and nature in Australia, and the lack of deep project management resources,

particularly as the volumes have increased; delays in dealing with Telstra

[redacted]; ineffective collaboration between NBN Co and its Delivery Partners

in resolving contract, design and construction issues; and disproportionate

focus on workforce size and Premises Passed as key drivers of behaviour rather

than Premises Activated driven by more effective design and collaboration.”

2.77

Version 12 of the 2013-16 Corporate Plan targeted 850,000 brownfields

premises passed by 30 June 2014.[47]

As set out above, this deployment profile was questioned by previous

shareholder Ministers, and the company was asked to develop a new Corporate

Plan taking into account the Telstra stop work on pit remediation. NBN Co did

so, but the September plan (“version 13”) has not been made public. However, as

noted above, the Minister made reference to the 30 June 2014 brownfields target

in version 13 of the Corporate Plan during the NBN Rebooted conference in

November 2013:

Shortly before the election, the NBN Co revised its June 30

2014 premises passed target down to 600,000 brownfield premises.

2.78

In his speech of 2 December 2013, Mr Quigley noted that the effect of

the revised 30 June 2014 target was to shift the construction end date by six

months:

We did have to advise the Government in September that, the

issues with the LN/DN construction combined with the remediation stoppage moved

the construction end date from June 2021 to December 2021.

2.79

As of 24 August 2013, build contract instructions had been issued for

512,818 brownfields premises.[48]

The issue of build contract instructions for the fibre network commences what

is referred to in the Strategic Review as the “construction phase.”[49]

The Strategic Review found that:

The construction phase is being completed in an average of

approximately 216 days (7.1. months), which is in line with the Corporate Plan.[50]

2.80

On this basis, by mid-March 2014 (216 days after 24 August 2013), NBN Co

was on track to pass approximately 512,000 premises. This is consistent with a

30 June 2014 target of 600,000 premises passed.

2.81

The interim Statement of Expectations was issued by shareholder

Ministers to NBN Co on 24 September 2013.[51]

Among other things, it states that:

In regard to rollout in brownfield areas, NBN Co should

continue existing construction where build instructions have been issued to

delivery partners. Any further build or remediation instructions should not

ordinarily be issued pending further analysis and discussion. Management of

existing design work should occur so as to optimise value in the context of the

Government’s policy for a flexible architecture.

2.82

In other words, permission must be sought from the Minister before build

contract instructions can be issued to delivery partners. The practical reality

of this constraint was illustrated by Dr Switkowski at the 17 December

committee hearing:

In fact, we have spent time in recent weeks petitioning the

government, as we must, to continue to authorise us to go as fast as we

possibly can and not be required to keep checking in with the department or

whatever with numbers.[52]

2.83

The Strategic Review began its work in October/November 2013. In

November 2013, when visiting Blacktown with Dr Switkowski, the Minister said:

[NBN Co has] issued design instructions for more premises,

twice as many premises to be passed by June 30 next year, as the NBN Co has

passed to date.[53]

2.84

This statement was later clarified by Josh Taylor of ZDNet:

Turnbull's office clarified that the NBN will have passed

450,000 brownfields premise[s] by the end of June. The NBN has currently passed

237,324 brownfields premises, with 164,501 able to order a service.[54]

2.85

The Strategic Review assumes that only 357,000 premises will be passed

by June 2014. This delay, in tandem with workfront assumptions, is then

extrapolated across the entire build, pushing the rollout completion date to

2024. According to the Strategic Review, this reduces revenues by approximately

$11.6 billion, increases operating expenditure by $5.4 billion, increases

interest payments by $7.5 billion and, ultimately, increases the assumed peak

funding amount for the fibre rollout by approximately $13 billion. This issue

was discussed during the 17 December hearing:

Mr Rousselot: The slower rollout is indeed driving the

bulk of the reduction in revenue for the period FY 2011 to FY 2021, which is

the number you are referring to. The slower rollout, however, is not based on

my assumptions; it is based on the actual track record that we have and the

review that has been done since then by KordaMentha, supported by the newly

appointed operations team of NBN Co...

CHAIR: ...But this is an assessment that has been done,

based on assumptions about a whole range of things—and we are going to get to them.

I just want to make it so we are all going to be talking about the same thing.

You say 'the vast bulk', I say that it is more than $11.6 billion, but $11.6

billion is the figure characterised by you, or by the strategic review, as the

hit on the revenue base of NBN Co. by the decision—the assumption, the

forecast—that you will extend by three years. That is just a fact.

Mr Rousselot: If I may, because we look back to FY

2012 plan, there are in fact actuals that cover the period between FY 2012 and

now. So this is not an assumption; it is a fact. Yes, there are assumptions

being made in terms of from now onwards. So it is a mix of the fact and the

track record that we have achieved between when the plan was published and

today, and then a forecast made for the period going forward.

CHAIR: I note that the strategic review assumes that

government equity does not change in the revised outlook. Is that correct?

Mr Rousselot: Yes, that is the assumption we have

worked under.

CHAIR: So, under your decision to incorporate all of

these in the review, this decision to delay the completion date by three years

halves the revenues to 2021, and what that means is that NBN Co. has to get

more money from private debt markets. Is that right?

Mr Rousselot: Again, you have mentioned 'my

decisions'. It is not my decision. It is a forecast that we have made based on

the actuals and assumptions that have been made going forward. And, yes, you

are correct; this is the impact on the revenue.

CHAIR: Thank you. And more money is needed from the

private debt markets because of this assumption that you have made. I am not

trying to split hairs. You keep changing between 'decisions', 'assumptions',

'forecasts', 'advice'; I do not mind which of them you pick. This is your

document, Mr Rousselot—that has been extensively explained to us by Dr

Switkowski—so you cannot keep trying to blame other people. Your name is on it.

Mr Rousselot: I am not blaming other people. I am just

stating the fact that, to build the numbers that you are looking at, we have

actuals to date and we have forecasts going forward; and your point on the debt

is we have assumed, when we look at the revised outlook, that the

current funding arrangement with the government would apply, which is a maximum

equity contribution of $30.1 billion, $30.5 billion, and any fund that is

required in addition, given the re-forecast that is made based on actuals and a

revised forecast, we have assumed to be funded through debt.

CHAIR: Okay. So the extra interest that NBN Co. has to

pay up until 2024, from 2021 to 2024, in this situation is $7.5 billion,

according to your chart on page 38?

Mr Rousselot: I think that is correct.

CHAIR: So your costs are up by $7.5 billion because of

the decision. Your revenue is down by $11.5 billion because of your assumption,

decision, interpretation, whatever. So what happens to opex if the rollout is

slowed by three years?

Mr Rousselot: I believe that the opex vary little

during the period. I think the biggest changes—

CHAIR: On page 38 it suggests that it increases by

$5.4 billion—that is a lot by my standards; it might be a little by yours.

Mr Rousselot: I understand why you have that. Certain

payments that are made that are in fact more representative of the rollout are

treated as opex, and I think that is why you have a difference in that number.

I will have to check...

CHAIR: ...So where we are is that by slowing the rollout

by three years you have added a lazy $13 billion to peak funding—it is just

mathematics; it is just that that is what happens?

Mr Rousselot: That is the result of the forecast that

we have made, yes.

2.86

The 357,000 target was discussed at both the 17 December 2013 hearing of

the committee, and the 25 February hearing of the Senate Estimates committee.[55]

During the 17 December hearing, graphs were presented which demonstrated the

various rollout trajectories of NBN Co (see Appendix 4).[56]

Also during this hearing, it was demonstrated that NBN Co was tracking at

approximately 5,000 premises per week—considerably in excess of what was

required to reach the 357,000 target. In response, Dr Switkowski said:

This to me illustrates one of the big problems around the

commentary with respect to NBN. You, from the outside, have taken a bunch of

numbers and challenged our ability to make forecasts when we have all of the

data and we understand what is happening out in the field. How does that work?

For example, you cannot take 5,000 homes passed per month and not allow for the

fact that from the middle of December to the middle of January the industry

shuts down. There is 20,000 off your number to start off with. You have got to

get down to that level of analysis to form a forward view. What we will not do

is come up with numbers that are excessively optimistic, which I assert has

characterised previous forecasts. To have people from outside the organisation

attempt to reinterpret our forecasts is ludicrous.

2.87

During the 25 February hearing of the Senate Estimates committee, Dr

Switkowski confirmed that NBN Co’s weekly average was between 4,500 and 5,000

premises per week.[57]

He also confirmed Mr Adcock’s comment at NBN Co’s half yearly results briefing

that NBN Co expected this number to be 6,000 premises per week by 30 June

2014—once again, substantially in excess of what was required to reach a target

of 357,000:

Senator CONROY: Do you recall the graphs of the

various rollout trajectories for NBN Co. that I showed you at the December

hearing of the Senate select committee?

Dr Switkowski: Generally.

Senator CONROY: During that discussion I noted that

NBN Co. was passing, on average, about 5,000 premises per week. I also noted

that if NBN Co. plateaued at its current level of activity NBN Co. would easily

pass more than 400,000 premises by 30 June 2014. I do recall, Dr Switkowski,

you took a very dim view of this 5,000 average, given that it included downtime

over the Christmas break. What is NBN Co's current weekly average?

Dr Switkowski: Somewhere between 4,500 and 5,000

premises passed.

Senator CONROY: I also note that Mr Adcock said last

night that NBN Co. expects to be doing 6,000 premises by 30 June. Is that

correct?

Dr Switkowski: That was the statement that was made,

yes.

Senator CONROY: I have been doing some maths of my own. NBN

Co's weekly average for brownfield premises—and I think you are roughly

indicating this—passed over the past 17 weeks is about the 4,500. If you

exclude the two weeks Christmas shutdown where contractors appear to have

down[ed] tools, it comes to 5,078, between, as you said, 4,500 and 5,000. If

you extrapolate 5,000 premises, which is less than your own chief operating

officer is indicating, to 30 June, and there is no Christmas shut down between

now and 30 June—that is right, isn't it?

Dr Switkowski: Just Easter.

Senator CONROY: You are having an Easter shutdown as

well?

Dr Switkowski: I am just reflecting how the industry

operates.

Senator CONROY: Fantastic. NBN Co. gets to slightly

more than 400,000 premises. Even if you take the 4,500 weekly average and

assume a steady linear growth to Mr Adcock's 6,000 per week by 30 June, NBN Co.

will still pass more than 400,000 brownfield premises by 30 June. Without you

having done the maths and hoping that I am not seriously misleading you at the

desk, does that sound about right?

Dr Switkowski: Your algebra is certainly right.

2.88

The Strategic Review also makes assumptions about the daily run rate

(premises passed per day at the peak of the rollout). The medium term outlook

factored in the extension of the design to delivery schedule to 15 months.[58]

This was projected to be brought back into the original 12 month schedule in

two years.[59]

This revision includes an escalation of the daily roll out rate to a peak of

4,800 premises passed, compared to Corporate Plan peaks of more than 5,400 per day

for the brownfields deployment.[60]

The Revised Outlook’s only basis for the lower peak rate is a comment that:

Based on workforce modelling previously undertaken by NBN Co,

and the Independent Assessment, it is not anticipated that construction field

labour is a limiting factor in the FTTP deployment. The biggest constraint to

the network rollout is the availability of network designers, senior and

experienced project managers, in-field supervisors and project control staff to

provide leadership and oversee program delivery....

This constraint allows a maximum of 200-300 concurrent

workfronts (for example, an FSAM, a set of nodes or HFC in-fill areas) and

dictates the highest practical deployment speed achievable.

2.89

The Strategic Review did not address the question of what strategies

could be employed to lift this constraint (e.g. training, additional contract

resource from Telstra). Nor did the Strategic Review acknowledge that many

construction projects in other sectors are approaching completion, releasing additional

project management resources. Rather, productivity improvements were “assumed

out” of the Revised Outlook and “assumed in” to the Radically Redesigned FTTP.

As NBN Co noted in answer to a question in writing:

Scenario 2, Radically Redesigned FTTP contemplates NBN Co

making significant changes to its FTTP deployment approach to improve NBN Co’s

productivity and construction techniques. Within this scenario, it is expected

that these “radical” changes will increase rollout speed and decrease costs.[61]

2.90

The Committee also notes the testimony of NBN Co’s Chief Financial

Officer, at the JCNBN hearing on 19 April 2013. When asked the financial impact

of extending the rollout, Mr Payne replied:[62]

The biggest impact of a one- or two-year delay will not have

much impact on the internal rate of return. With a two-year delay we would

probably still expect to see an internal rate of return of around seven per

cent. Where it does have a big impact is on the peak funding requirement. Under

the existing plan, we have a peak funding requirement of just over $44 billion.

If we extended the rollout, it would reduce that peak funding requirement

because we are spending capex after a time when we have gone to cash flow

positive. That would come down by $2 billion or $3 billion.

2.91

This evidence demonstrates that, by itself, a deployment delay does not

necessarily produce an increase in peak funding. The delay must work in tandem

with an assumption that shifts the timing of when NBN Co becomes cash flow

positive. Put another way, if revenues are not assumed away (beyond 2021) from

the delayed deployment schedule, then according to Mr Payne’s testimony the

result of assumptions of delay in the brownfields deployment schedule would be

a decrease in peak funding.

2.92

NBN Co was asked in writing following the 17 December public hearing to

reconcile Mr Payne’s comment with the conclusion of the Strategic Review. At

the time of writing the question is unanswered.

2.93

The committee has serious concerns with the delayed deployment forecast

of the brownfields fibre build in the Revised Outlook. The June 2014 target of

357,000 premises passed by June 2014 is at odds with NBN Co’s weekly average,

statements made by the Minister before the Strategic Review concluded its work,

and NBN Co’s own statements at its half yearly results briefing. Furthermore,

the committee notes that NBN Co’s fibre deployment speed is conditional upon

the political control evident in the interim statement of expectations.

2.94

The revised deployment schedule—and the assumption that $11.6 billion in

revenues will be foregone as a result—has another consequence in the Strategic

Review. Revenues for the full fibre rollout are stripped out of scenario

comparisons, while the full assumed costs are included. This is visible in the

table comparing the financial outcomes of the scenarios (Exhibit 4-6,

reproduced below). This table includes revenues to FY2021 (when scenario 6 is

assumed to be complete) but capital expenditure to 2024 (when the Revised

Outlook assumes that the full fibre rollout will be complete). Incidentally,

this is true of delay assumptions for all network elements in the Revised

Outlook (more on this below). The committee also notes that the revenues

excluded from the Revised Outlook in Exhibit 4-6 are the three years when the

Revised Outlook assumes revenues will be the highest—$15 billion over FY2022,

FY2023 and FY2024.[63]

Exhibit 4-6 (Strategic Review)

2.95

The committee considers that the 30 June 2014 target—and the revised

deployment schedule—has been “lowballed” to achieve political objectives. This

includes setting a target so low that NBN Co could not fail to meet it—and in

fact would have to reduce its weekly run rate to avoid exceeding it. It also

provides support for the claimed three year rollout extension, which is assumed

to reduce revenues by approximately $11.6 billion, increase operating

expenditure by $5.4 billion, increase interest payments by $7.5 billion and,

ultimately, increase the assumed peak funding amount in the Revised Outlook by

approximately $13 billion. The committee also notes that a ‘lowball’ target

also provides a platform for NBN Co and Government to trumpet exceeding this

target in July 2014. As Dr Switkowski noted at the February estimates hearing:

I hope to be in front of the committee after June explaining

how we did better than the early forecasts.[64]

Summary—Assumption of brownfield

delays

-

The Revised Outlook assumes that NBN Co will pass 357,000

brownfields premises by 30 June 2014, compared to 600,000 in the Corporate Plan

(version 13). This assumption—in concert with conservative estimates of

premises passed at peak rollout—is reflected in the revised deployment

schedule, which assumes the fibre network will not be complete until 2024.

-

The 30 June 2014 target is at odds with NBN Co’s current run

rate, the number of build instructions issued by NBN Co by August 2013, and the

Strategic Review’s own finding that the construction phase is being completed

in line with Corporate Plan timing assumptions. The committee notes also that NBN

Co’s speed of fibre deployment has been brought under direct political control.

These factors cast doubt on the revised deployment schedule in the Revised

Outlook, and the assumed consequences of this assumption.

-

The committee considers that the 30 June 2014 target has been

“lowballed” to achieve political objectives. This includes setting a target so

low that NBN Co could not fail to meet it. It also provides support for the

claimed three year rollout extension, which delivers the following financial impacts:

- revenues are decreased by approximately $11.6 billion;

- operating expenditure is increased by $5.4 billion;

- interest payments are increased by $7.5 billion; and

- the assumed peak funding amount is increased by approximately

$13 billion.

Cost per premises assumptions –

brownfields[65]

2.96

NBN Co’s Chief Financial Officer gave the following evidence at the

November hearing of the Senate Environment and Communications Estimates

Committee in relation to the cost per premises passed of the NBN fibre build:[66]

Senator LUNDY: I understand that in April NBN Co.

advised the Joint Committee on the NBN that the current cost of building the

local network and distribution network falls between $1,100 and $1,400 per

premise. Is that correct?

Mr Payne: At the time we presented that to the joint

committee, that was our best estimate of the costs of completing the areas that

we were building in at that time. So that was our best estimate at that point

in time.

Senator LUNDY: Has it changed since that point in

time?

Mr Payne: Since that point in time we have done a

number of things. We have obviously started in more areas and have had some