Chapter 2

Managed investment schemes

2.1

The passage of the Managed Investment Act 1998 (MIA) created a

framework that allowed for the establishment of an investment

structure—a managed investment scheme. This structure replaced the prescribed

interest schemes that, up to that time, were widely used as a collective

investment mechanism to 'pool' investors' funds.[1]

2.2

The primary object of the MIA was to strengthen investor protection in

an era of unprecedented growth in collective investment schemes. The deregulation

of financial markets in the 1980s saw a proliferation of collective investment

vehicles, from the

largest commercial property and management trusts to small one-off schemes such

as pine forests, ostrich and yabby farms. The government's support for

self-funded retirement, following the introduction of compulsory superannuation

in 1992, further stimulated growth in this sector during the 1990s. According

to a review of the MIA undertaken in 2001:

A key driving principle behind the new framework was the

shortcoming evident under the dual trustee/fund manager structure of the former

[prescribed investment] regime, where it was difficult to determine who was

ultimately responsible for a scheme's operation.[2]

2.3

Under the MIA, the managed investment sector continued to expand

substantially with new companies forming to offer products to the retail

market. In particular, agribusiness MIS grew. In this chapter, the committee

examines the structure, responsibilities and operation of agribusiness MIS.

Structure

2.4

As a structure, MIS allows for collective investments that enable a

large number of investors (either retail or wholesale) to pool funds, or invest

in a common enterprise, for large scale projects.[3]

They have the following features:

-

people contribute money or money's worth as consideration to

acquire rights (interests) to benefits produced by the scheme (whether the

rights are actual, prospective or contingent, and whether they are enforceable

or not);

-

contributions are pooled, or used in a common enterprise, to

produce financial benefits, or benefits consisting of rights or interests in

property, for the people (the members) who hold interests in the scheme

(whether as contributors to the scheme or as people who have acquired interests

from holders); and

-

members do not have day-to-day control over the operation of the

scheme (whether or not they have the right to be consulted or to give

directions).[4]

2.5

The MIA removed the requirement for an independent trustee. Under this new

legislation, a single responsible entity (RE) replaced the dual trustee/fund

manager structure of the prescribed interest regime and was directly responsible

to scheme members for the scheme's operation. The intention was to avoid the

confusion over accountability engendered by the dual trustee/fund manager

structure of the previous regime.

Responsible entity

2.6

A registered MIS cannot operate without an RE, which must be a public company

that holds an Australian financial services licence (AFSL) authorising it to

operate a managed investment scheme.[5]

As noted above, investors do not have

day-to-day control of the enterprise, rather the RE carries full responsibility

for a scheme and any liability for losses. One of the duties of an RE is to

hold scheme property on trust for scheme members.[6]

As the operator of an agribusinesses MIS, the RE agrees to plant, manage and

harvest the product with the harvest proceeds net of outstanding costs and fees

returned to the investor.[7]

In exercising its powers and carrying out its duties, the RE of a registered

scheme must:

-

act honestly;

-

exercise the degree of care and diligence that a reasonable person

would exercise if they were in the responsible entity's position;

-

act in the best interests of the members and, if there is a conflict

between the members' interests and its own interests, give priority to the

members' interests;

-

treat the members who hold interests of the same class equally

and members who hold interests of different classes fairly;

-

not make use of information acquired through being the responsible

entity in order to:

-

gain an improper advantage for itself or another person; or

-

cause detriment to the members of the scheme;

-

ensure that the scheme's constitution meets the requirements of

sections 601GA and 601GB (provisions governing contents of the constitution and

legal enforceability of the constitution);

-

ensure that the scheme's compliance plan meets the requirements

of section 601HA (provisions governing the contents of the compliance plan);

-

comply with the scheme's compliance plan;

-

ensure that scheme property is:

-

clearly identified as scheme property; and

-

held separately from property of the responsible entity and

property of any other scheme;

-

ensure that the scheme property is valued at regular intervals appropriate

to the nature of the property;

-

ensure that all payments out of the scheme property are made in

accordance with the scheme's constitution and the Act;

-

report to ASIC any breach of the Act that:

-

relates to the scheme; and

-

has had, or is likely to have, a materially adverse effect on the

interests of members;

as soon as

practicable after it becomes aware of the breach; and

-

carry out or comply with any other duty, not inconsistent with the

Corporations Act, that is conferred on the responsible entity by the scheme's

constitution.[8]

2.7

It should be noted that these requirements were in force during the

period covered by this inquiry.

2.8

An officer of the RE of a registered scheme is under similar statutory

obligations to, among other things, act honestly; exercise the degree of care and

diligence that a reasonable person would exercise if they were in the officer's

position; and act in the best interests of the members. If there is a conflict

between the members' interests and the interests of the RE, the officer is to give

priority to the members' interests. Officers of an RE must not make improper

use of their position as officers to gain, directly or indirectly, an advantage

for themselves or for any other person or to cause detriment to the members of

the scheme. In addition, officers must take all steps that a reasonable person

would take to ensure that the responsible entity complies with the Corporations

Act, any conditions imposed on the responsible entity's Australian financial

services licence, the scheme's constitution and compliance plan.[9]

2.9

ASIC informed the committee that, although the legislative framework for

MIS has been 'the subject of a number of reviews and a significant amount of

work in developing potential refinements', the regime has remained largely unchanged.[10]

Agribusiness MIS

2.10

Agribusiness MIS are essentially a means to finance agricultural

operations on a large scale. They allow small investors to pool their funds and

to invest in a large agricultural operation that can achieve significant scale.

This pooling of investment funds is most beneficial in those agricultural

industries where scale is necessary to achieve low cost production.[11]

Individual investors then delegate their allotments to a single manager for the

efficient operation of the entire scheme. Investor fees provide the scheme

manager with the necessary funds to establish and operate the scheme.[12]

2.11

According to the Australian Forest Products Association, the MIS

structure proved effective in 'leveraging private sector investment in

plantation development' and became a high profile source of investment in rural

industries. It suggested that this success was due to schemes being able to:

-

provide investment scale through pooling of investments funds;

-

provide economies of scale through year-on-year investment in the

resource;

-

address information deficiencies and lower transaction costs; and

-

improve cash flow to help offset high up-front establishment

costs.[13]

2.12

During their early years, agribusiness MIS accounted for around $300

million per annum of investment in rural industries—mostly in forestry,

viticulture/wine, olives and almonds. Although, a minor source of investment

overall, agribusiness MIS have been important in the development of some

industries—notably blue gum forestry and olives.[14]

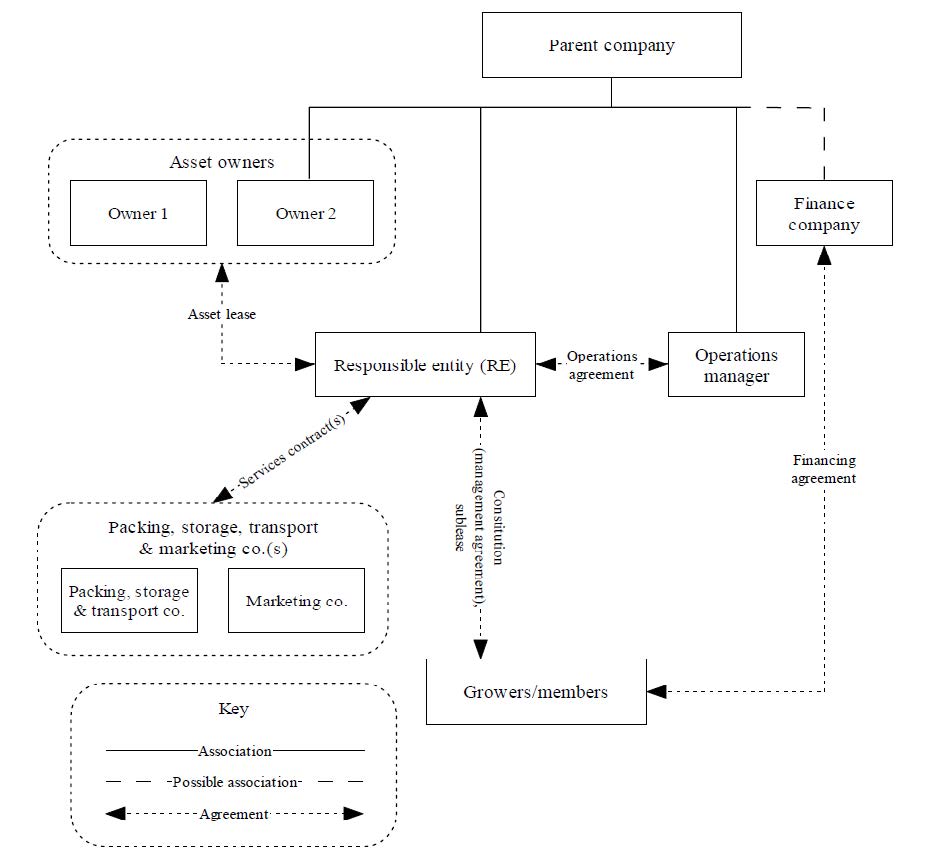

Figure 2.1: A typical MIS structure[15]

Growers' rights

2.13

By and large, investors in an agribusiness MIS (known as growers) do not

own any physical assets, such as the land or trees. The growers' contributions

secure them an interest in the scheme, which, in effect, is a bundle of rights

over an area of land or allotment. These rights include 'a right to have

particular services carried out in a given area of land (such as the

establishment and maintenance of trees for growing a crop), and a limited right

to the trees and the crop that is grown'.[16]

ASIC explained:

...investors acquire a right to derive profits from

agribusiness produce of the agribusiness enterprise (e.g. timber, wine, grapes,

olives, and almonds), net of management and lease fees paid to the

responsibility entity, and net of rent and other expenses incurred in operating

the agribusiness scheme.[17]

2.14

Generally, on entering the scheme, investors assign their rights to the

crop to the manager in return for a share of the harvest proceeds. Researchers

have noted that:

Even though the investor may have 'ownership rights' to the

trees or crop on a specific acreage, the MIS agreement provides that the harvest

proceeds from the whole scheme are shared pro rata among investors according to

their relative investments—thereby diversifying risk. [18]

2.15

The Great Southern Plantations 2007 Project was one such scheme. The

scheme was registered with ASIC on 8 March 2007, at which time Great Southern

Managers Australia Limited (GSMAL) became the RE. Approximately 4,000 growers

invested in the scheme which took in 43,989 woodlots of about one third of a

hectare each. By May 2009, growers had invested around $132 million in the

scheme. The relationship between GSMAL and the growers was defined by a Product

Disclosure Statement (PDS), a scheme constitution, the terms of the sub lease

and management agreement whereby each grower engaged GSMAL to prepare,

establish, maintain and ultimately harvest the trees.[19]

According to the Bendigo and Adelaide Bank:

A managed investment scheme was the logical investment

vehicle for Great Southern to offer pooled investments in plantation and

agricultural projects to investors.[20]

Tax benefits

2.16

For tax reasons, many agribusiness MIS were structured so that investors

were taken to operate their agribusiness investment in their own right. Thus,

an agribusiness MIS is a tax effective investment vehicle. With this type of

scheme, investors can claim a personal income tax deduction for the cost of

investing in timber plantation and agribusiness development activities—for the

up-front investment and any annual fees paid to the RE and its related parties.[21]

According to ASIC, agribusiness schemes were designed around this tax benefit,

which is 'received at point of initial investment and then subsequent revenue

commencing at a variable time later, such as 4–5 years later when the crops

reach maturity'.[22]

Although there have been changes to the tax regimes for forestry and non-forestry

MIS, the allowable tax deductions are a common characteristic of the schemes.[23]

Financing investment through

borrowing

2.17

The provision of finance is a marked feature of agribusiness MIS. While

some growers drew on their own funds to finance their investment, many chose to

access finance offered through their scheme, which provided finance for growers

to make their initial application fee. Repayments were to be made over the life

of the loan and fully discharged from the proceeds of the harvest. The scheme

allowed an upfront tax deduction of the loan application fee and of interest

payments on the loans.

Forestry MIS

2.18

Forestry schemes refer to plantation forestry projects which may be

ready to harvest in 8–25 years, necessitating a long period between investment

and return.[24]

The Australian Forest Products Association noted the significant challenges in

attracting private investment into plantation forestry created by the large

scale required to achieve a viable resource, the asset's relative illiquidity,

high initial costs and long waiting period for return on these long-term

ventures.[25]

Plantations 2020 Vision

2.19

In the 1990s, Australia faced a growing trade deficit in wood products.[26]

In 1992, the Commonwealth and state governments endorsed a plantation policy contained

in the National Forest Policy Statement (1992). Importantly, one of the policy

goals was to increase the total area of forest. In this regard, the governments

recognised that the long-term nature of plantation investments, often in excess

of twenty years, could cause difficulties attracting investment capital as the policy

statement explained:

When capital is committed for such a long time before a

return is received, companies, individuals and farmers may be reluctant to

invest in plantations.[27]

2.20

Notably, under this policy, the Commonwealth recognised 'pooled development

funds' as a useful mechanism for promoting long-term investments, including

plantation development, and announced it would encourage the establishment of such

funds. Also, taxation was identified as one of the areas that could help

minimise impediments to plantation development and assist governments achieve

their plantation objectives.[28]

2.21

In July 1996, the Ministerial Council on Forestry, Fisheries and

Aquaculture endorsed the plantation industry's target of trebling the

plantation estate by the year 2020. To achieve this target, the Ministerial Council

agreed, in consultation with relevant stakeholders, to develop a realistic and

achievable national strategy. Subsequently, in 1997, Plantation 2020 Vision was

released. This agreement was a three way partnership involving the Australian,

state and territory governments and industry.[29]

2.22

In addition to trebling Australia's plantation estate, one of the

strategic gaols of the 2020 Vision was to have a plantation

industry with a sound reputation as a credible investment destination and to

have 'well-informed investors' willingly participate in 'well-run and

profitable managed investment plantations projects'.[30]

The expectation was that private investment would take on a bigger role in

helping to boost the national plantation estate.

2.23

Following the release of the 2020 Vision, Australia's

plantation estate increased significantly to around 2 million hectares by 2008.[31]

Mr Alan Cummine, who has extensive experience in the forestry industry,

attributed the growth in private plantation after 1997–98 to companies that had

been managing 'prospectus-financed' forestry schemes for some years responding

positively to the launch of the 2020 Vision.[32]

Structure of forestry MIS

2.24

Although forestry investment schemes take on different forms, their core

activities involve establishing, managing, harvesting, processing and supplying

timber products from plantation grown on behalf of shareholders, unit holders

and scheme members.[33]

For example with the Willmott Group:

Each investor leased an area on which trees were to be grown.

Generally, each investor made a forestry management agreement with a company in

the Willmott group, by which that company agreed to plant, maintain and harvest

the trees. Most forestry management agreements provided for the investor to pay

the relevant company an initial fee, but for the investor to pay no further sum

until the trees were harvested.[34]

2.25

Each lease was for a term of years and some leases gave the tenant an

option for a further term.[35]

The National Association of Forest Industries noted the special characteristics

that distinguish forestry MIS, including the significant proportion of the

total costs that are incurred during the plantation establishment phase. In

this regard, it noted that growers are required to 'wait a long time before any

returns on their investments can be realised'. It stated:

There is no annual source of income and in the most simple

forestry investments, the trees are established in the first year of the

project and income is received when the trees are harvested a minimum of ten

years later.[36]

2.26

Also, a single forestry scheme could be conducted on multiple

plantations, which were distant from each other. Again using Willmott as an

example:

The growers' individual woodlots may be adjacent to woodlots

in other schemes, and land used in the schemes is intermingled, creating a

'chequerboard' effect.

The lots are divided and allocated to growers at random and

land in various schemes is intermingled. This is true of all regions. To access

its lot, an individual grower may have to cross other growers' land and to

identify a grower's land, GPS is necessary, but not always possible. Surveying

would be prohibitively expensive.[37]

2.27

The Great Southern Plantation 2003 Project was another such scheme.

Members of the group (growers) participated in a scheme to grow and harvest

timber in forestry plantations. Under the schemes, a grower would acquire an

interest in a woodlot where trees would be grown and harvested on the grower's

behalf.[38]

The grower would enter into a land management agreement with GSMAL.

Fee structure

2.28

The fee structures for forestry projects generally require an up-front

fee from investors, and deferred rental and management fee out of proceeds of

the harvest, which can be many years later. Some forestry MIS, however, may require

growers to make annual lease and management payments as well as the up-front

fee.[39]

2.29

ASIC observed that fee structures that rely on up-front payments and

payments out of proceeds from harvests have presented issues for the sector.

This structure requires the RE (or its ultimate parent) to absorb a sustained

period of negative cashflows until the project produces enough income to meet

its costs.[40]

Horticultural MIS

2.30

Horticultural MIS were also operating before the MIS regime commenced in

1998 but increased significantly after 2004. According to ASIC, the growth was due

largely to Timbercorp's expansion into this sector. Non-forestry agribusiness

MIS have focused on horticultural crops involving olives (for oil), almonds and

wine grapes. Other horticultural crops include; macadamia nuts, citrus fruit,

stone fruit, tomatoes, olives, table grapes, mangoes, avocados, truffles and

wheat.[41]

2.31

The wait for a return on investment in these projects differs between

crops but is less than forestry MIS. ASIC explained:

Horticultural schemes (almonds, wine grapes and olives) are

marketed in Australia as being fully income producing after 5 years. They then

generally [are] expected to have a revenue producing life of up to 22 years.[42]

2.32

Horticulture projects, however, are labour and capital intensive in

comparison to forestry MIS.[43]

2.33

While each horticultural MIS was structured differently, it is possible

to make generalisations on how they operated.[44]

In the main, agreements in an MIS comprised a constitution, a management

agreement, a head lease and sublease and a compliance plan.[45]

Normally, the schemes were structured around a contract between the grower and

RE.

-

The MIS operator leases land and water rights from land owners

which are often associated with the MIS operator. The land owner usually funds

all land preparation and infrastructure necessary for the project and acquires

all necessary water licences. Most MIS projects are either fully or partially

developed by the landowning entity at the time MIS participants are accepted

into the project.

-

After leasing the land and water rights, the MIS operator then

divides these into allotments or plots, which are then subleased to individual

MIS participants to conduct agribusinesses.

-

The MIS operator then enters into a management agreement to

operate and manage the agribusinesses of MIS participants. As a rule, the

management agreement will be the same for all the MIS participants—there is a

master agreement to which a list of MIS participants is attached.

-

MIS participants pay the MIS operator an up-front fee as well as

annual rent and management fees in return for managing the MIS project—in other

words the growers enter into a contract with the RE to cultivate, maintain and

harvest their agribusiness enterprise on their behalf.[46]

-

The MIS operator enters into an operations agreement with another

entity, the MIS manager, who is usually also associated with the MIS operator.

The MIS manager manages day-to-day operations, from preparing land to harvesting.

The MIS manager usually conducts these activities through contracting third

parties to undertake the work. Generally the contractor makes the major

decisions on how the farming activities are conducted with the MIS manager

overseeing.

-

Once the crop is harvested, the MIS operator contracts one or

more companies to pack, store, transport and market the product.[47]

2.34

The MIS operator receives the proceeds from the sale of the harvested

product and once received, holds them on trust for the MIS participants. The

MIS operator keeps a proportion as a harvesting/marketing fee and distributes

the remainder to MIS participants in proportion to the funds contributed and

number of interests held. All produce grown on the project is pooled and the

amount that a MIS participant receives takes no account of the price received

for the variety grown on their individual allotment or of the yield from their

allotment.[48]

Fee structure

2.35

Generally horticultural projects require an upfront fee from growers and

either:

-

on-going annual rental and management fees to the manager to

carry on the business as per the prospectus; or

-

rental and annual fees paid out of net proceeds from harvests

(for typical horticultural MIS, returns are generated after 4–5 years).[49]

2.36

Most commonly the fee structure for agricultural and horticultural

public investment ventures was based on leasing an identifiable area of land to

an investor. In some prospectuses, ownership of an identifiable area of land

was offered to the investor.[50]

Agribusiness MIS collapses

2.37

After the introduction of the MIA, the number of agribusiness MIS grew steadily

until the high profile collapses in 2009 and subsequent years. During the

lead-up to these failures, there was a notable surge in investment in agribusiness

MIS. In the peak year of 2006–07, investors placed over $1.2 billion in MIS

projects.[51]

According to figures cited by the National Farmers' Federation, the MIS

industry managed to raise $1.079 billion in the 2007/08 financial year.

Non-forestry projects received 35 per cent ($378 million) of total MIS funds.[52]

2.38

Statistics indicate that contributions to non-forestry MIS grew rapidly

from $160 million in 2003–04 to $256 million for 2004–05, $445 million in

2005–06 and $467 million in 2006–07.[53]

With regard to forestry MIS, according to NewForests, the MIS sector established

almost 1 million hectares (2.5 million acres) of timber plantation in Australia

between 1998 and 2008.[54]

Overall, ASIC informed the committee that since the introduction of the MIS

regime in 1998 agribusiness schemes had raised approximately $8 billion.[55]

The following table provides detail on the funds invested in agribusiness and

shows the amounts invested during the peak years of 2006–2008 and the sudden

decline thereafter.

Table 2.1:

Estimates of amounts invested in Agribusiness MIS 2000–2012[56]

|

Year

|

Amount invested

Agribusiness MIS ($)

|

Timber ($)

|

Other($)

|

Projects

|

Participants

|

|

2012

|

40m

|

40m

|

0

|

4

|

165

|

|

2011

|

51m

|

48.6m

|

2.4m

|

10

|

491

|

|

2010

|

103m

|

74m

|

29m

|

14

|

2,474

|

|

2009

|

250m

|

227m

|

23m

|

26

|

7,560

|

|

2008

|

1.079b

|

701m

|

378m

|

56

|

24,300

|

|

2007

|

1,139b

|

672m

|

467m

|

67

|

24,500

|

|

2006

|

1,141b

|

698m

|

442m

|

57

|

25,800

|

|

2005

|

1,024b

|

767m

|

257m

|

47

|

~16,200

|

|

2004

|

665m

|

500m

|

165m

|

42

|

~15,800

|

|

2003

|

345m

|

247m

|

98m

|

45

|

|

|

2002

|

300m

|

189m

|

111m

|

68

|

|

|

2001

|

~500m

|

|

|

|

|

|

2000

|

~800m

|

|

|

|

|

Source—Australian

Agribusiness end of year reports for 2000 to 2010 income years, Data for 2011

and 2012 income years estimated from ATO data.

2.39

In 2008, the industry was highly concentrated with Timbercorp,

Great Southern and Gunns the major scheme operators. In the five years

leading up to 2009, ASIC estimated that 'approximately $5 billion had been

invested in agribusiness schemes by over 75,000 investors'. Forestry schemes

represented approximately $3.7 billion of the $5 billion.[57]

ASIC produced the following breakdown of the funds raised by major schemes:

-

Timbercorp, around $1 billion;

-

Great Southern, $1.8 billion;

-

FEA Plantations, $426 million;

-

Rewards Projects Limited, $291 million;

-

Willmott Forests, about $400 million; and

-

Gunns Plantations, about $1.8 billion.[58]

2.40

Timbercorp was the first major agribusiness MIS to fail followed by

Great Southern.[59]

Based on ASIC's analysis, the majority of investors in both the Great Southern

and Timbercorp schemes were retail investors.[60]

Since then, there have been only a small number of forestry MIS offered to

retail investors. In addition, as a result of the winding up and deregistration

of a number of these schemes, there has been a reduction in the number of

registered schemes.[61]

2.41

In this report, the committee refers mainly to four of the main agribusiness

MIS—Timbercorp, Great Southern, Willmott Forests and Gunns.

Timbercorp

2.42

Mr Robert Hance and Mr David Muir established the Timbercorp Group in

1992. They incorporated Timbercorp Eucalypts Ltd, an unlisted public company,

which became known as Timbercorp Ltd. At the same time, Timbercorp Finance Pty

Ltd was incorporated as a subsidiary to provide finance to investor growers. The

Timbercorp Group of companies carried on business promoting managed investment

schemes. Investors, known as growers, invested and participated in the growing

of trees, almonds, olives and other horticultural products.[62]

2.43

On 4 April 2000, Timbercorp Securities Ltd (TSL) was incorporated and

replaced Timbercorp as the operator of the existing schemes and became the RE

of each new scheme. TSL held an AFS licence and became the RE for 34 registered

forestry and horticultural MIS, including eucalypts, almonds, olives, citrus,

avocadoes, mangoes and grapes. According to ASIC, the majority of TSL's

agricultural assets were in forestry plantations in Albany, WA and the Green

Triangle region spanning the Victorian and South Australian border. TSL's substantial

horticultural operations (mainly almonds and olives) were located across the country.[63]

Financing arm

2.44

As mentioned above Timbercorp Finance Pty Ltd was a subsidiary of the

parent company and provided finance to investor growers.

Liquidation

2.45

On 23 April 2009, TSL, its ASX-listed parent Timbercorp Limited

(Timbercorp) and around 40 other associated entities appointed KordaMentha as

voluntary administrators.[64]

The creditors resolved to put each one of the group companies into voluntary

liquidation. At a meeting on 29 June 2009, the creditors resolved to wind up

the companies and the administrators became joint and several liquidators.

2.46

At the time of its collapse and liquidation, there were 33 registered

MIS and three unregistered private scheme offers. TSL schemes had approximately

18,400 investors who had invested $1.095 billion.[65]

As a result of the collapse, the majority of the Timbercorp schemes could not

be carried to completion, meaning the investments were of limited or no value.

Following the collapse, liquidators also commenced or threatened recovery

actions against investors who had borrowed money from Timbercorp Finance.

Timbercorp Finance had outstanding loans to over 14,500 investors, totalling

$477.8 million.[66]

Great Southern

2.47

The Great Southern group of companies grew to become the largest manager

of agricultural-based MIS in Australia and the largest owner of land for

commercially grown hardwood plantations.[67]

Great Southern Managers Australia Limited (GSMAL) was an Australian Financial Services

(AFS) licensee and RE of 43 registered forestry and horticultural MIS and raised

around $2 billion between and 2004 and 2009 from 43,000 investors.[68]

According to ASIC, the majority of GSMAL's agricultural assets were in forestry

plantations located in Western Australia and the Green Triangle region. GSMAL

also conducted substantial horticultural operations (olives, wine grapes and

almonds) which were spread across the country.[69]

Financing arm

2.48

Many investors in Great Southern took advantage of finance offered by

Great Southern Finance, which was facilitated through Great Southern's

arrangements with Bendigo and Adelaide Bank.[70]

Great Southern Finance Pty Ltd (GSF) was the financing arm of the Great

Southern Group.[71]

Liquidation

2.49

The Great Southern Group collapsed in May 2009 and joint and several

voluntary administrators were appointed.[72]

At that time, the Great Southern Group comprised the parent company, GSL, and

34 subsidiaries.[73]

On 19 November 2009, creditors resolved to appoint the liquidators as joint and

several liquidators of GSMAL. GSMAL and GSF were wholly owned subsidiaries of GSL.[74]

2.50

The Bendigo and Adelaide Bank made it clear that at the time

administrators, receivers and liquidators were appointed to the Great Southern

group of companies, no administrators were appointed to the Great Southern plantation

schemes. It explained:

Following a competitive process largely financed on behalf of

investors by Bendigo and Adelaide Bank...Gunns Plantations Ltd was appointed to

replace GSMAL as responsible entity for most of the Great Southern plantation

schemes in December 2009 and January 2010. Gunns, and other bidders for the role,

intended to manage the schemes through to completion on behalf of investors. [75]

2.51

Unfortunately for investors in Great Southern MIS, Gunns also struggled

to make the schemes profitable and ultimately administrators were appointed in

September 2012. Put simply, the plantation managed investment schemes did not

have the resources to manage the plantations to completion.[76]

Willmott Forests Limited (WFL)

2.52

Willmott Forests Limited (WFL), which was the RE for a number of managed

investment schemes, collapsed financially in September 2010 and receivers and

voluntary administrators were appointed.

2.53

On 26 October 2010, new voluntary administrators were appointed. They

determined that WFL was 'insolvent and without funds to meet its debts, comply

with its statutory obligations as owner/manager of the plantations and fulfil

its obligations to the growers and third parties under the constituent

documents'.[77]

Subsequently, in March 2011, the creditors of WFL resolved that the company be

wound up and liquidators appointed. The liquidators found that the Willmott

schemes could not continue to operate and that it was 'very unlikely' that 'a

party would be willing to take over as RE and manager of the schemes'. They set

in train a process to sell the assets.[78]

Gunns

2.54

Gunns Plantations Limited (GPL) was formed in 1999 and, as noted above,

also acted as the RE for the Great Southern Pulpwood Forestry Schemes

(1998–2006).[79]

2.55

In September 2012, an ANZ-led syndicate of banks that were owed about

$560 million appointed KordaMentha as receivers. They were to carry out a

detailed analysis of plantation timber managed-investment schemes run by the

company, 'into which thousands of investors had pumped about $600 million'.[80]

PPB Advisory, specialists in corporate recovery, restructure and insolvency,

were appointed as administrators of GPL on 25 September 2012 and liquidators on

5 March 2013.

2.56

Following, the collapse of the Gunns Group, the liquidators sought

expressions of interest for a RE, but, according to the court:

With the exception of the 2000 and 2001 schemes, no

satisfactory replacement could be found. GPL had no funds. The scheme

landowners were in receivership. The receivers had issued notices of default to

GPL under Forestry Right Deeds, adding further uncertainty to the growers'

position and their ability to recover any value from their investments.[81]

2.57

Without a properly funded entity to assume all the responsibilities and

obligations of an RE for the schemes, the court was satisfied that 'the only

course open to the liquidators was to sell the schemes'.[82]

Conclusion

2.58

Although the MIA was intended to strengthen investor protection, the collapse

of a number of high-profile agribusiness MIS has resulted in substantial financial

losses for investors in such schemes. Before looking more closely at the

failure and liquidation of agribusiness MIS, the committee seeks to highlight

the human dimension of the failure of these schemes and to bring to the fore

the lived experiences of the investors.

Navigation: Previous Page | Contents | Next Page